Co-authored by Katie Griffing, co-founder of Launchway Media, a digital marketing and PR agency that works with technology startups, and Tomás Güida, venture capital investor at All Iron Ventures and former BizOps at the Argentine startup Jampp, a growth platform for mobile apps.

The number of Spanish fintechs increased by 16% in 2019, according to the latest Fintech Radar report by Finnovista. The Spanish fintech ecosystem is gaining strength and there are nearly 400 fintech startups, a dramatic increase from 50 fintech startups reported just five years ago.

Several conditions have led to Spain’s recent fintech boom. For one, both traditional financial institutions and small businesses are undergoing digital transformations, investing heavily in new technologies that help cut costs and improve operational efficiency. The Spanish government also began drafting a law for a regulatory sandbox in 2018, giving fintechs the green light to test their innovations without risk of infringing on regulatory requirements.

Spain joins the United Kingdom and the Netherlands as one of the few European countries to introduce a regulatory sandbox. The Spanish Association of Fintech and Insurtech (AEFI), whose main objective is to create a favorable environment for the development of fintech and insurtech companies in Spain, played a key role in pushing for the approval of the regulatory sandbox. Although Spain was one of the last members of the European Union to transpose PSD2 into national law, the new banking directive is playing an active role as well. Open banking, which allows third parties to access consumer bank account data as a means to provide new products and services, is lowering the barriers for new fintech entrants and bolstering competition in the banking space overall.

In response to PSD2, traditional banks are feeling the pressure to become more agile. Meanwhile, the latest generation of fintech startups is launching and gaining traction far more quickly. All of these factors are shaping both the present and future of the fintech industry in Spain.

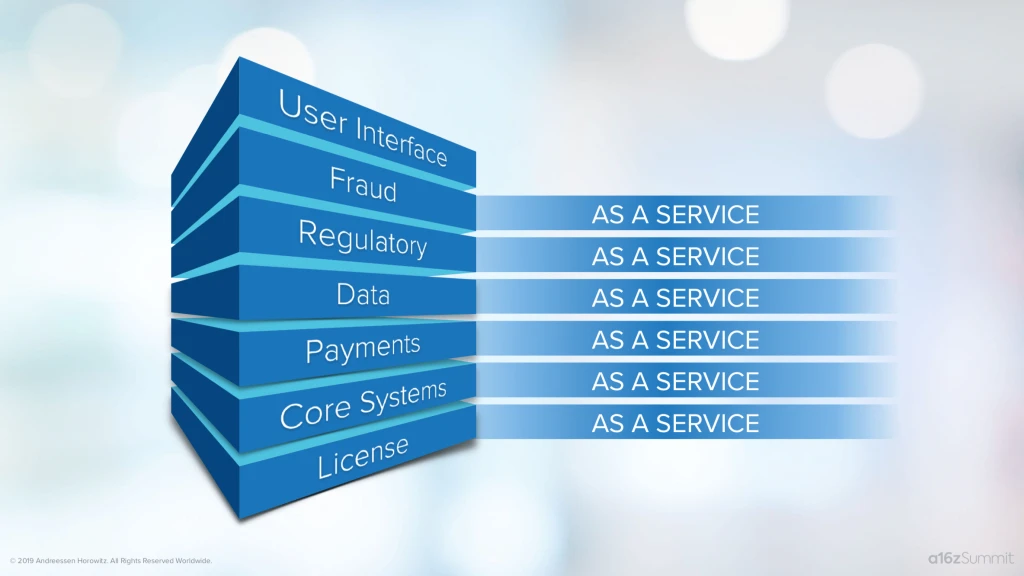

Enter: fintech-as-a-service

Just as Amazon Web Services eliminated so many of the barriers and costs involved to start a software company by providing ‘infrastructure-as-a-service,’ the same disruption is coming to the financial services market. Spanish startups already operating in this space include Flanks and Unnax, both of which provide businesses with open banking APIs and all of the tools necessary to offer new financial services based on consumer data.

Source: Every Company Will Be a Fintech Company by Angela Strange

It’s only a matter of time before ‘fintech-as-a-service’ takes off on a larger scale in Spain as startups turn to financial services as another avenue for growth. Soon we could see Spanish startups with large contract workforces – such as Cabify, Glovo, or Habitissimo – introduce a service like Lyft Direct, a no-fee bank account and debit card which allows Lyft drivers to access their earnings instantly after each ride. With Lyft Direct, drivers can also earn up to 4% cashback on everyday purchases, regardless of their credit. With thousands of contract workers across Spain (and Latin America), adding on financial services could provide a significant bump in revenue as these startups push to become profitable.

Then there are global companies like Shopify and Stripe which didn't start out as providers of credit, but recently introduced these services (Shopify Capital and Stripe Capital). The data they have on their customers allows them to evaluate risk more easily and offer better terms. Business management software companies operating in Spain, such as Cuentica and Nextail, could be well-positioned to offer lending services to SMEs in need of working capital as well.

B2B fintech edges over B2C

Spain is home to a heavily-banked population and plenty of consumer-focused banking products and services; however, PSD2 has fueled a significant rise in business-to-business (B2B) fintech as well. In fact, over half of Spanish fintechs (52%) are now operating in the B2B market.

Primarily tapping into the unmet needs of SMEs, a number of startups are developing more cost-efficient and convenient open platforms and APIs that address everything from B2B payments, SME lending, invoicing, and accounting, becoming a one-stop-shop for all of a business’ banking and administration needs.

Source: Finnovista Fintech Radar Spain 2019

Exaccta, for example, automatically extracts relevant data from invoices in real-time and generates quarterly taxes based on the user’s tax profile. It is designed for self-employed workers, accounting advisory firms, and SMEs. Holded, a robust business management platform, allows businesses to manage everything from human resources and project management to accounting and invoicing in one place, integrating with a number of other services such as Amazon, Paypal, and more.

Spain currently has more than 3.2 million self-employed workers, and 86% of Spanish SMEs have fewer than ten employees. Nomo is one of the first challenger banks targeting this market in Spain, securing more than 25,000 users as of September 2019. In July 2019, the Bank of Spain also approved one of the first B2B challenger banks, Neo, which will allow businesses to receive, store, and pay in 30 currencies. Neo is one of the first fintechs in Europe to offer both investment services (ruled by MIFID2) and payment services (ruled by PSD2) in one application.

Alternative financing sources are also growing at a faster pace than in the past. According to data from the Spanish Crowdlending Association (ACLE), crowdlending platforms provided 118 million euros in financing in 2018, with MytripleA leading the sector in volume. As Spain continues to do more to foster SME access to banking and alternative sources of finance by adapting regulations and introducing targeted policies that support fintech, more lending startups are tapping into this underserved market.

Tracxn counts 69 alternative lending startups operating in Spain as of September 2019, and these companies are breaking records constantly. In November 2019, online lender and credit scorer, ID Finance, raised £4.95 million, a record amount for an equity crowdfunding campaign in Spain. NoviCap, which provides short-term financing of working capital via factoring and confirming services, recently reached 100 million euros in financing to SMEs.

Many Spanish startups that started out in the B2C market are also evolving into B2B players, and this trend is likely to continue as barriers to entry lower and the need to connect new services into a single, comprehensive solution increases.

The fintech-proptech overlap

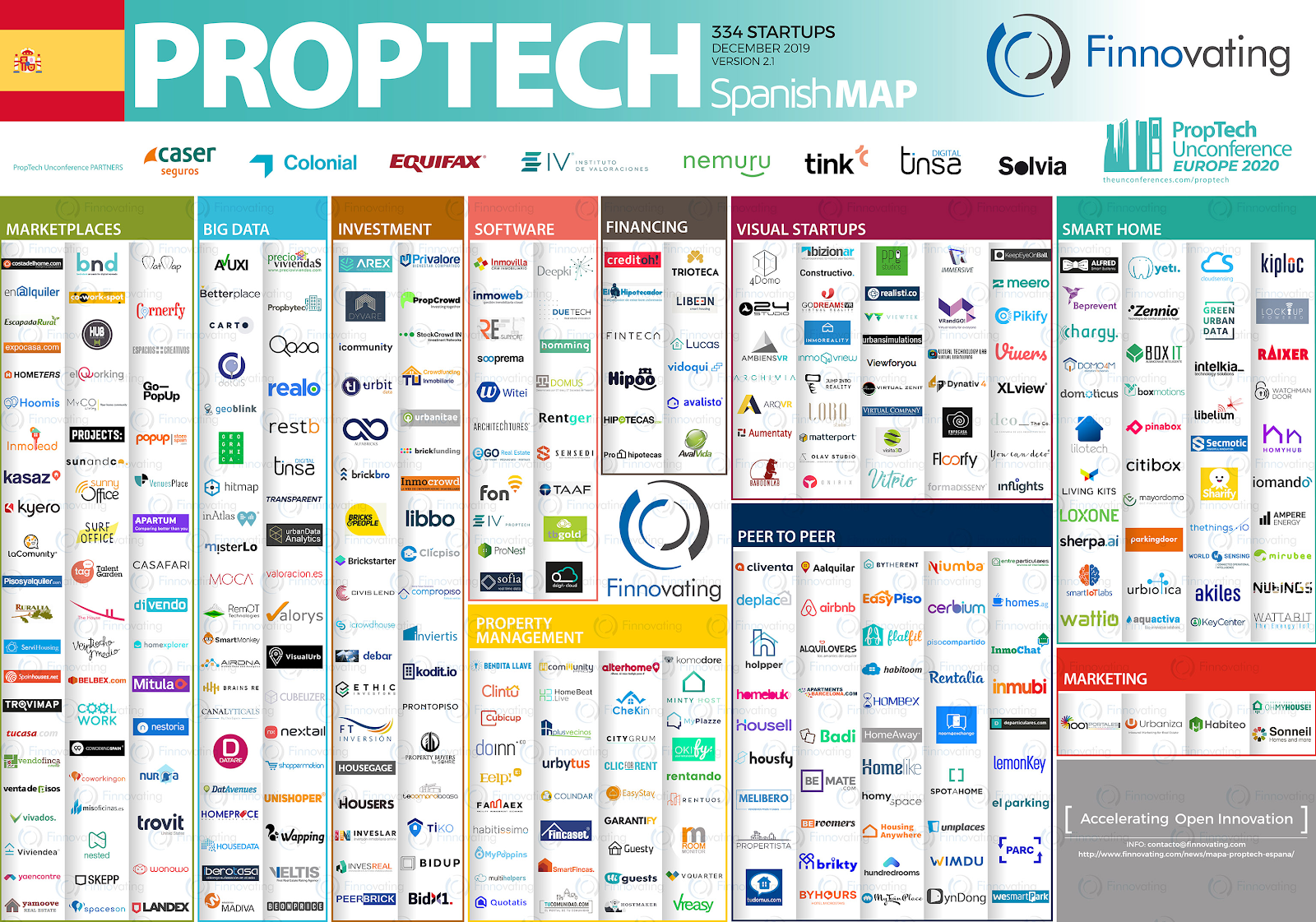

Another sector that is capturing growing venture capital interest in Spain is proptech. In 2017, Spain’s proptech sector attracted US$60 million, and these investments more than doubled in 2018, reaching US$150 million. According to Finnovating, there are now more than 330 proptech companies currently operating in Spain, a 37% increase over the year prior. Finnovating also shows that 87% of these proptech startups are focused on the B2B market.

Source: Spain December 2019 Proptech Map by Finnovating

As the proptech ecosystem in Spain consolidates and matures, so will its overlap with the fintech industry. Both proptech and fintech seek to eliminate the time-consuming and costly steps involved in real estate transactions. This is another area that remains underserved as there are still significant regulatory and market acceptance barriers to overcome. However, many startups, including lending and mortgage platforms, online payment systems, and real estate crowdfunding platforms, are starting to see traction.

Based on existing models in the US and the UK, a new generation of Spanish fintechs are tackling the mortgage technology segment, making it easier to plan, apply for, and manage mortgages. Many of these platforms have secured special agreements with banks, eliminating bureaucratic obstacles and providing mortgage approval decisions within a few days. Hipoo, Trioteca, Helloteca, Prohipotecas, and Finteca are just a few of the startups disrupting the mortgage sector.

Meanwhile, platforms focused on eliminating the intermediaries and commissions involved when selling property may soon move into the mortgage business as well, following the lead of global giants like Zillow. Founded in early 2016, home sales platform Housfy claims to be the fastest-growing real estate company in Spain, with operations in more than 80 cities. Housell, another home sales platform that recently raised €12 million, reports it’s sold more than 2,000 properties since it began operations in 2017. For platforms like these, adding financing services to provide a more seamless experience is a logical next step.

Pushing Spanish fintech forward

The rapid pace of change in such a dynamic market like Spain makes it difficult to anticipate what trends will actually evolve and dominate in the new year. However, there is proof that fintech is working its way into nearly every business sector, and a growing number of startups are introducing innovative solutions to address the financial needs of those that have underserved for so long by traditional institutions.

New fintech regulations will also open the doors for more banking services through existing online platforms. Spain is currently home to one of the most active fintech ecosystems in Europe, but there are still many milestones to achieve in order to solidify this achievement and ensure that the sector continues to grow.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.