Every investment decision you make on Wall Street requires the balancing of risk and reward. However, simply taking on big risks doesn't guarantee big rewards.

Shares of Bed Bath & Beyond (NASDAQ: BBBY) have plunged in 2022 as the company attempts to turn its struggling business around. If it succeeds, there could be material upside for investors, but the likelihood of failure seems elevated.

Here's what smart, risk-conscious investors need to consider before adding this troubled company to their portfolios.

1. The stock price

Bed Bath & Beyond's stock has fallen 80% so far in 2022. But it has seen wild price spikes thanks to the meme stock crowd. From its peak price, which was achieved late in the first quarter, the stock is down nearly 90%.

There's two ways to look at this.

Image source: Getty Images.

On the one hand, a low price means that investors are discounting a worst-case scenario. That effectively reduces risk for investors buying at the lows.

However, there is a financial metric known as the Merton Model, used by credit professionals and stock analysts, that suggests the exact opposite when considering price declines as severe as the one Bed Bath & Beyond has experienced.

To vastly simplify things, a deep stock price decline highlights increasing bankruptcy risk.

To be fair, taken alone, a share price decline could go either way. But the smartest investors don't look at a single variable when making a decision. The key is to consider a matrix of issues.

And that's where this home goods retailer's story starts to get really troubling.

2. Heaps of debt

Turning a company around is difficult, but not impossible. It is much easier to do when management isn't simultaneously trying to fix a weak balance sheet.

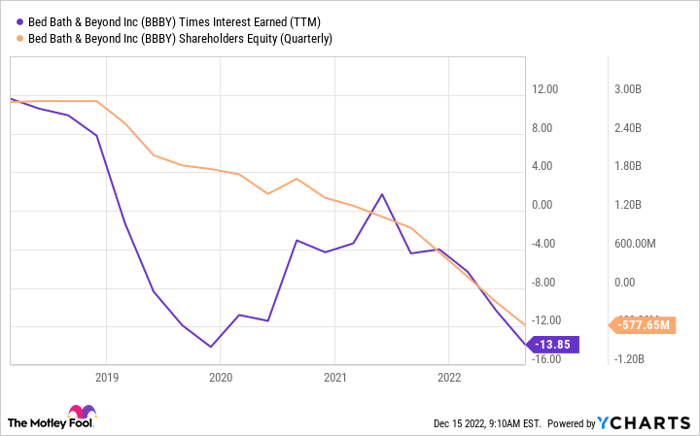

Bed Bath & Beyond's long-term debt stood at a hefty $1.7 billion at the end of the fiscal second quarter. That figure is around 45% higher than it was a year ago and the company isn't covering its trailing-12-month interest expenses.

To highlight the problem, Bed Bath & Beyond recently sold shares at the current deeply depressed levels. The proceeds were earmarked for debt reduction.

This decision suggests that diluting shareholders is less of a problem than the company's burdensome debt pile, which should worry investors.

BBBY Times Interest Earned (TTM) data by YCharts

3. Nothing left

In the debt-focused discussion above you, might have noticed that the debt-to-equity ratio wasn't mentioned. It's a common tool when assessing a company's financial strength, but there's one big problem in using it here.

Bed Bath & Beyond's shareholder equity, a key financial metric used in the debt-to-equity ratio, is negative.

That effectively makes the debt-to-equity ratio a virtually meaningless number. But there is a bigger takeaway here: Negative shareholder equity also means that in the worst-case scenario of bankruptcy, there will almost certainly be nothing left over for shareholders.

Simply put, if the turnaround doesn't work out, investors could lose everything.

4. Consistently poor results

Bed Bath & Beyond is attempting to close less desirable stores and make other changes that it hopes will get the business back on the right track. There's likely to be near-term pain before any positive results show up.

However, so far, the story has been almost all pain.

For example, revenue has been on the decline since peaking in 2018. Notably, that was before the coronavirus pandemic upended the retail sector in 2020. Trailing-12-month earnings, meanwhile, have been in a broad downtrend since roughly 2016.

The company's problems are not new, even though the pandemic did help to exacerbate their impact. And despite a brief earnings recovery after the initial hit from the pandemic, revenue and earnings trends have only gotten worse.

If Bed Bath & Beyond were financially strong, it could probably handle this business adversity in stride, but at this point, it isn't.

5. Missteps and new management

Even though the pandemic helped to make Bed Bath & Beyond's situation worse, there were a number of self-inflicted troubles as well.

For example, it shifted its merchandising strategy and ended up with private-label products that consumers didn't want. And now it is struggling with supply chain problems that may leave it light on products during the important holiday season.

A key issue now is the company's strained relationship with its suppliers because it stopped paying them in a timely manner. At this point, it looks like management is kind of lost.

Which brings up the huge management turnover that's taken place, including the CEO, CFO, and a key marketing position.

Turnover in the executive suite, in and of itself, isn't a big worry. However, when you combine it with a financially weak company struggling to turn itself around, it becomes yet another sign that risk may be too high.

Look at it in one of two ways: Either the board has decided that the company's previous leaders weren't moving in the right direction (leaving new leadership to fix their mistakes while simultaneously trying a different approach), or previous leaders decided to move on because they believed that, perhaps, things were too far gone.

Too many warts

Smart investors consider multiple facts as they look to make a final investment decision. With Bed Bath & Beyond, there are so many negatives that most folks are probably better off watching from the sidelines as this turnaround effort continues to unfold.

This is a stock that only the most aggressive investors should be considering today, and even intrepid types will probably have a hard time pulling the trigger.

10 stocks we like better than Bed Bath & Beyond

When our award-winning analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

They just revealed what they believe are the ten best stocks for investors to buy right now... and Bed Bath & Beyond wasn't one of them! That's right -- they think these 10 stocks are even better buys.

*Stock Advisor returns as of December 1, 2022

Reuben Gregg Brewer has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.