Shares of cloud software pioneer Salesforce (NYSE: CRM) are falling hard after the company's second-quarter earnings update. Results were solid, but Salesforce is clearly hurting because of currency exchange rates. The outlook for full-year financial results were downgraded again as a result.

To offset this weakness, Salesforce announced its first-ever share repurchase program.

An $800 million drag on revenue

First, let's address the issues facing Salesforce (and all multinational organizations) right now. During the three months ended July 31, the company reported revenue of $7.72 billion, a 22% year-over-year increase. That was slightly higher than the outlook for $7.70 billion provided a few months ago.

But as co-CEO Marc Benioff said on theearnings call the U.S. dollar continues to strengthen against foreign currencies. Among other reasons, this is a side effect of the Federal Reserve's interest rate hikes this year as it tries to bring down inflation.

For a company like Salesforce that has significant sales overseas (about 32% international revenue in the second quarter), a stronger U.S. dollar lowers the value of a sale made in foreign currency when that money is converted back into dollars.

Specifically, Benioff said these exchange-rate headwinds lowered total revenue by about $250 million, $50 million more than forecast three months ago. And for the full year, foreign currency is now expected to be an $800 million drag, more than the $600 million previously anticipated.

Paired with other effects from a global economic slowdown, Salesforce decreased its expectation for full-year revenue to a range of $30.9 billion to $31.0 billion (down from $31.7 billion to $31.8 billion). This new outlook implies year-over-year growth of about 17%, or 20% when excluding exchange-rate effects.

Can stock buybacks save the day?

The good news is that, in spite of lower revenue coming through the pipes, Salesforce expects to maintain an adjusted operating margin of 20.4% for the current fiscal year. Management is guiding for $7.3 billion in operating cash flowing through to Salesforce this year, which it can use to invest in the business and return to shareholders.

On that latter note, Salesforce has always been focused on maximizing its expansion. Cash return to shareholders was always a topic for later discussion -- that is, until now. The company just announced its first-ever share repurchase program with total consideration of up to $10 billion.

One of the big complaints about Salesforce over the years is its issuance of new stock. Some of that was in the form of stock-based compensation to employees (just over $1.6 billion through the first half of this year) but also from the acquisition of smaller software peers.

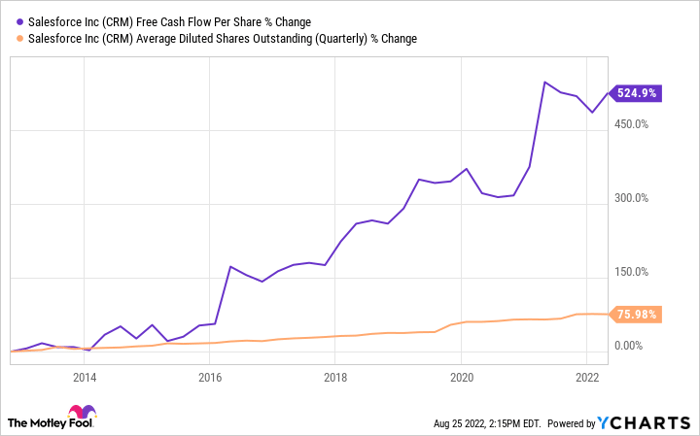

After years of growth, though, the top team at Salesforce is ready to start bringing the share count down to boost free-cash-flow per share. The company has already delivered massive returns on this metric via its acquisitions and organic growth efforts (in spite of issuing lots of new stock in the process), but a share repurchase program could help keep things headed in the right direction.

Data by YCharts.

A share repurchase program could also go a long way toward offsetting the current growth slowdown due to the U.S. dollar's epic run. Salesforce's free cash flow is also rebounding after the company made its largest-ever acquisition of Slack last year, so bringing the share count down will help get free cash flow per share back to setting new records sooner than rather than later.

After the earnings update, Salesforce trades for 31 times enterprise value to trailing-12-month free cash flow. The company's growth rate is decelerating, at least for the time being, but the new share repurchase program only bolsters the value for shareholders. This remains a solid stock to stay invested in for the long haul.

10 stocks we like better than Salesforce, Inc.

When our award-winning analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

They just revealed what they believe are the ten best stocks for investors to buy right now... and Salesforce, Inc. wasn't one of them! That's right -- they think these 10 stocks are even better buys.

*Stock Advisor returns as of August 17, 2022

Nicholas Rossolillo and his clients have positions in Salesforce, Inc. The Motley Fool has positions in and recommends Salesforce, Inc. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.