General Dynamics’ GD first quarter results were more or less in line with expectations. Revenue in particular was very close to what analysts projected, and represented a 1% increase from last March. Earnings grew 5.2% to beat the Zacks Consensus Estimate by 4.8%.

Segmental revenue beats/misses may not exactly reflect the result on the total revenue line because not every analyst providing total estimates also provides the line details. But they are still indicative of segmental performance in any given quarter:

Accordingly, Aerospace revenue of $1.903 billion beat estimates by 16.9%; Marine Systems revenue of $2.651 billion beat by 5.2%; Combat Systems revenue of 1.675 billion missed by 3.3% and Technologies revenue of $3.163 billion beat by 1.7%.

Analyst estimates are generally a good indication of the results a company is likely to report in any given quarter. That is because analysts study various aspects of the business including the major drivers of its growth, the internal strengths and weaknesses, the cost base on which it operates, pricing strength and so forth to arrive at projections of its future performance. Hence, these projections are studied opinions that can be depended upon.

And because they can be depended upon, investors develop a certain expectation about a company’s performance based on the estimates for the concerned period. And when a company significantly underperforms or outperforms estimates, there is usually a reaction from investors that is represented in the share prices. In this case, investors were largely unmoved, sending shares up 1.8%.

Drilling further down into the numbers reveals more about each segment’s quarterly performance.

Accordingly, we see that it is Combat Systems that missed analyst estimates on the bottom line as well. This segment missed estimates by 2.5% while Aerospace Systems, Marine Systems and Technologies beat by a respective 39.9%, 1.2% and 1.8%.

Conclusion

In the last quarter, the Aerospace business did significantly better than expected both in terms of revenue and profits. Analysts also expected lower revenue and better operating efficiency in the Marine business. Other segments were relatively close to analyst estimates.

Zacks Rank

General Dynamics has a Zacks #3 (Hold) Rank, based on its current risk/reward profile, but #2 (Buy) ranked Huntington Ingalls Industries HII is a better option for investors looking for exposure to the industry right now.

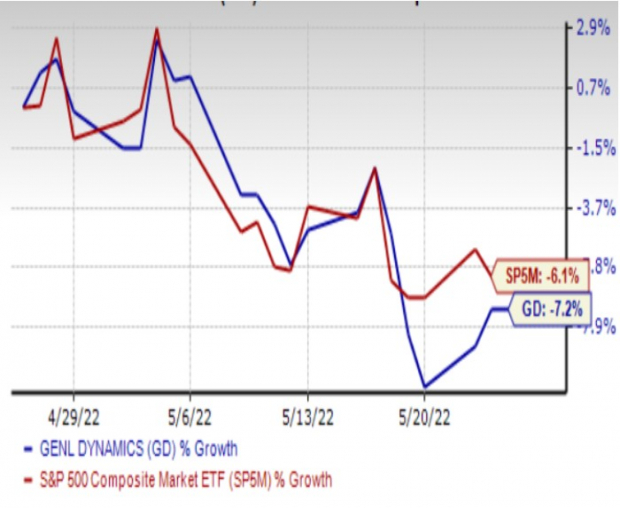

One Month Price Performance

Image Source: Zacks Investment Research

Zacks’ Top Picks to Cash in on Artificial Intelligence

This world-changing technology is projected to generate $100s of billions by 2025. From self-driving cars to consumer data analysis, people are relying on machines more than we ever have before. Now is the time to capitalize on the 4th Industrial Revolution. Zacks’ urgent special report reveals 6 AI picks investors need to know about today.

See 6 Artificial Intelligence Stocks With Extreme Upside Potential>>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

General Dynamics Corporation (GD): Free Stock Analysis Report

Huntington Ingalls Industries, Inc. (HII): Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.