Please find Running Oak's most recent performance and letter below.

Why Invest in Efficient Growth:

- Top 5 percentile: Running Oak’s Efficient Growth separate account has performed in the top 5% of all Mid Cap Core funds - despite being historically out of favor - in Morningstar's database over the last 10 years, net of fees.1

- Opportune: A little known - yet very large - hole exists in the typical equity portfolio, precisely where the most attractive risk/reward asymmetry currently lies. Efficient Growth fills that hole - and opportunity - like few portfolios do.

- 5 Stars: Efficient Growth has a 5-Star Morningstar rating.

- Since inception, Efficient Growth has provided 23% more return than the S&P 500 Equal Weight Index, given the same level of downside risk, gross of fees. (Ulcer Performance Index)*

Differentiated Approach and Construction

- Mid Cap stocks are at their cheapest in 25 years relative to Large. Efficient Growth provides significant Mid Cap exposure.

- Efficient Growth is built upon 3 longstanding, common sense principles: maximize earnings growth, strictly avoid inflated valuations, protect to the downside.

- Running Oak utilizes a highly disciplined, rules-based process, resulting in a portfolio that is reliable, repeatable, and unemotional.

How to Invest

- Efficient Growth is currently available as an SMA and ETF. (ETF specifics and SMA historical performance can't be shared in the same letter - sorry, it's annoying, I know. Please inquire for the ticker or more information.)

- In just 2 years, The ETF Which Shall Not Be Named has grown over 18,800% since launch - from 2 to 377mm.

Performance Update

- Running Oak’s Efficient Growth portfolio was up 2.17%, gross of fees (2.13%, net), in June.*

"Thinking without awareness is the main dilemma of human existence.” Eckhart Tolle, The New Earth

Data by itself and without context is worthless. Data that doesn’t make sense is likely to be just plain harmful. Efficient Growth makes sense. It's obvious: Maximize earnings growth while avoiding overvalued companies (companies that should go down) and other characteristics that clearly lead to greater downside risk (debt, etc.). Efficient Growth makes sense AND has performed especially well, despite a historically unfavorable environment for a disciplined, risk-focused strategy.

"Look, man, you can listen to Jimi, but you can’t hear him." — Sidney Dean to Billy Hoyle, White Men Can’t Jump

Thinking

“The S&P 500 outperforms 85 to 90% of funds over the long run.” – Standard & Poor's (you know, the people who make money – a LOT of money - selling the S&P 500)

Awareness

Cap-weighted indexes, by construction, will ALWAYS be overweight overvalued companies and underweight undervalued companies. NO ONE would EVER say “I want to invest more in overvalued companies and less in undervalued companies”…, because that would be dumb. Yet, over 50% of equity investment is now invested in that manner.

When the nonsensical is dominating like never before, beware.

After discussing Running Oak’s approach, a gentleman who once worked directly with John Bogle said, “Jack would have loved this.” Our strategy is technically active (because it’s thoughtfully constructed). It’s everything the passive devotees claim John Bogle would hate. They never met him. Meanwhile, a gentleman who worked directly with him said he would have loved it. I think John Bogle would have been deeply unsettled by the blind dogmatic religion that has grown out of his ideas – thinking without awareness | Data without common sense | Listening without hearing | Thoughtlessly investing more in overvalued companies and less in undervalued companies.

"I'm in the zone, man. I'm in the… zone." – Billy Hoyle, just before he chokes to lose the game

There’s a time and place for everything or, at least, most things. The S&P 500 is a play on Momentum. Because the S&P consistently invests more in overvalued companies and less in undervalued companies, it performs best when the stocks that have gone up most go up more. Last year, Momentum hit the 99.8% in history. It’s been a great run, which is awesome. However, because we humans are susceptible to recency bias, we believe that which happened recently will happen forever. 99.8% equates to 1 in 500. 1 in 500 isn’t the norm; it's a very rare exception. Instead of betting on reversal to the 499 in 500, investors are betting more and more on the 1 in 500. Most strategies will experience their day in the sun, and the S&P 500 has done so to a historic degree... but the investment philosophy is still nonsensical.

"Sometimes when you win, you really lose. And sometimes when you lose, you really win." — Gloria Clemente

As people, we tend to swing from one emotional extreme to the other. 99.8% is extreme. People have come to – like in 2000 - believe that investing is easy and that 99.8% is normal. “Investors” sit in their underwear… in their mom’s basement… on Robinhood… day trading PLTR (740% from its lows), OPEN (up 1000% in days), CRCL (priced at $31 and shot up to just under $300), KSS ($9 to $21 in a few days for no reason), TSLA (up 80% despite crumbling sales), GPRO ( up almost 400% in a few days), ARKK (100% in 3 months), Bitcoin, Fartcoin, etc. This behavior and sentiment is precisely what culminated in the drawdown of 2022. When the manager that has destroyed more value in history, ARK, is up 100% in 3 months, it's time to stop listening and start hearing.

An advisor shared the other day that a client recently told him “Bitcoin will NEVER go below $115,000.” Uh oh.

Complacency - a feeling of quiet pleasure or security, often while unaware of some potential danger or defect. (Note: Bitcoin can go below $115,000. In fact, it can go to $0. It likely won’t…, but it can.)

As has happened many times in the past, the more investors make, the easier they think it is. The longer that goes on, the more complacent they get. The more complacent they get, the less aware they are of a potential danger or defect, such as investing is REALLY hard. And then they all too often lost more than they made. “Sometimes when you win, you really lose.”

"We going Sizzler!" — Sidney Deane and Billy Hoyle

The forward PE of the 10 largest companies in the S&P 500 is now roughly 15% HIGHER than the forward PE of the 10 largest at the peak of the Tech Bubble.

Only 7 months into the year, "buy-the-dip" has delivered a higher return than any full year since 1985, aside from 2020.

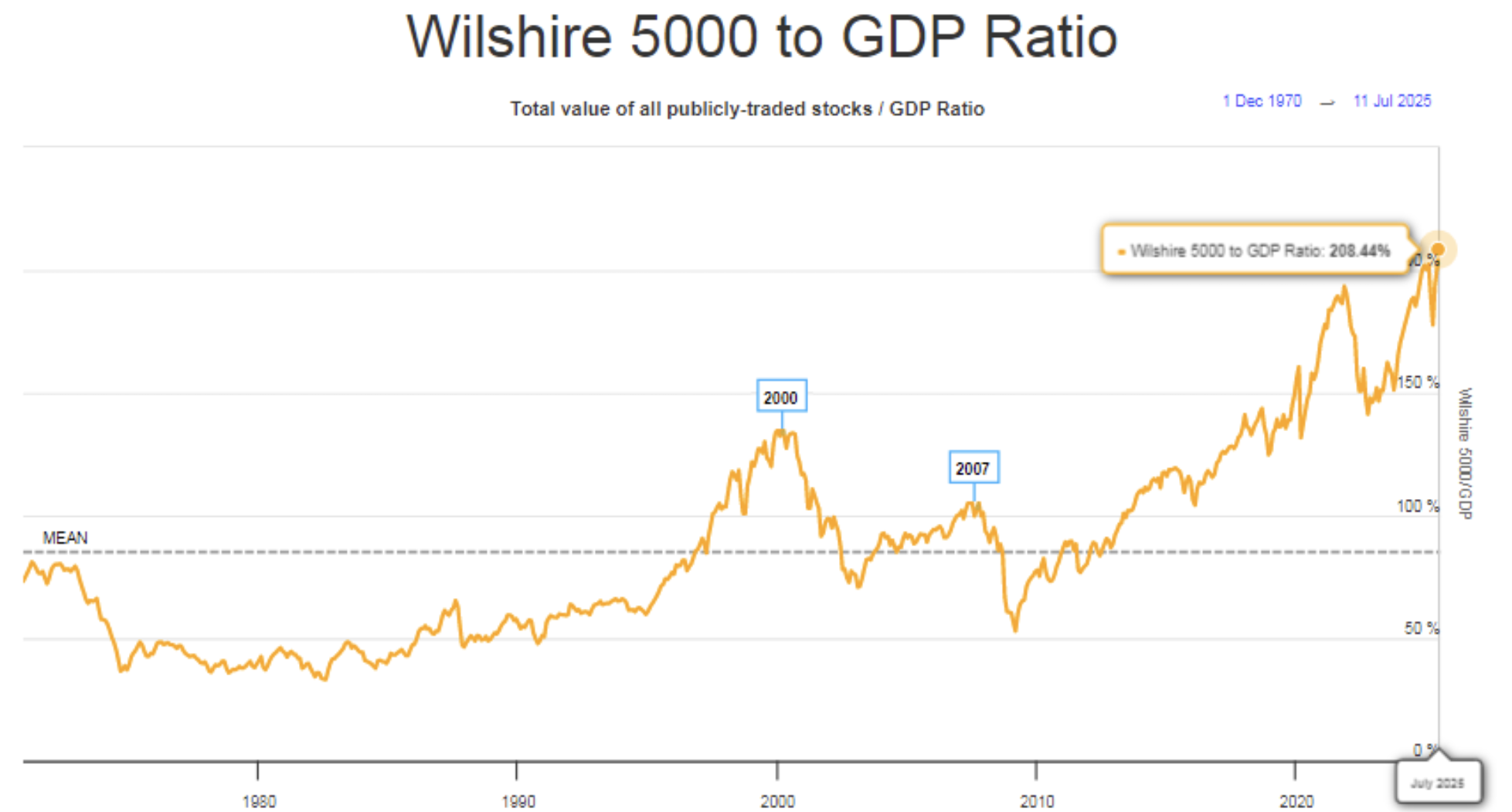

The Buffett Indicator, described by Warren Buffett as “the best single measure” of valuations. is now 50% HIGHER than the peak of the Tech Bubble.

Fund managers are now all-in on US stocks.

The average household currently has 20% MORE of their net worth invested in stocks than at the peak of the Tech Bubble. Households are doing so at a time when the top 10 holdings of the S&P are trading at a higher forward PE than the peak of the Tech Bubble, the stock market is more untethered from the economy than any time in history, and fund managers are all-in.

"You still throwing up bricks? What is this, a mason's convention?" - Sidney Deane

BRICK - Insiders, the people who know the most about their own companies, are selling. According to The Kobeissi Letter, only 11.1% of companies with insider activity are seeing more buying than selling by corporate officers and directors, the LOWEST share on record.

BRICK - Housing defaults look like they're about to eclipse Financial Crisis levels.

BRICK - The University of Michigan unemployment expectations have NEVER hit this level outside of a recession.

BRICK - The Conference Board’s Leading Economic Index (LEI) has experienced the steepest decline since the 2008 financial crisis, eclipsing the Tech Bubble.

BRICK - Population growth has completely stalled. Population growth is one of the biggest drivers of economic growth.

"You building a house with those bricks?" - Sidney Deane

Sequence of Returns - Why all of the above REALLY matters, particularly to anyone looking to use invested capital over the next decade

"I don’t lose. I just run out of time." - Billy Hoyle

Every investment discussion focuses on two main themes: risk and return, EXCEPT the passive/index fund narrative. Those who push passive conveniently neglect to mention risk. If they do, they say "just hold on", "the market goes up eventually", "don't sell"... That isn't addressing risk; that is avoiding the topic, and retirees don't have the option to just hide or pretend the market will magically be where they need it. There has rarely been a more critical time to protect clients - especially older clients - to the downside. Efficient Growth has provided roughly 50% less downside than the S&P 500 over the last 36 years, per average drawdown.*

Running Oak addresses downside proactively by:

- Avoiding overvalued companies that SHOULD go down

- Avoiding companies with too much debt that have a high likelihood of insolvency or dilution

- Diversifying across companies - Efficient Growth invests in 50 to 75 stocks.

- Equal-Weighting and not taking outsized risk in one company

- Diversifying across industries

Billy: "You are like a woman possessed."

Gloria: "Possessed by the spirit of intelligence, you moron!"

Invest Where Others Aren't (MARGE - Upper Mid/Lower Large Cap)

- Investing where everyone else is investing means higher prices, higher valuations, lower implied returns, higher implied downside.

- Investing where others aren't means lower prices, lower valuations, higher implied returns, lower implied downside and a margin of error.

- Investing where others aren't also provides valuable diversification.

- If the market goes up, others are likely to follow, propelling prices.

- If the market goes down, others can't sell what they don't own, meaning less selling and downside pressure.

It's win/win.

Running Oak's goal is to maximize the exponential growth of clients' portfolios, while subjecting them to far less risk of loss. In other words, we aim to help your clients realize their dreams and avoid their nightmares.

If you appreciate critical thinking, math, common sense, and occasional sarcasm, we would love to speak with you. Please feel free to set up a time here: Schedule a call.

Seth L. Cogswell

Founder and Managing Partner

Edina, MN 55424

P +1 919.656.3712

For additional data and context regarding the claims made within this letter, please refer to the Disclosures and Additional Data document located here.

Investment Advisory Services are offered through Running Oak Capital, a registered investment adviser.

The opinions voiced in this material are those of Running Oak Capital’s, do not constitute investment advice, and are not intended as recommendations for any individual. To determine which investments and strategies may be appropriate for you, consult with us at Running Oak Capital or another trusted investment adviser.

*Past performance is no guarantee of future results. Performance expectations are no guarantee of future results; they reflect educated guesses that may or may not come to fruition. All indices are unmanaged and may not be invested into directly.

*Statements regarding the large gap in the middle of the typical equity allocation reflect the opinion of Running Oak Capital This is based on informal feedback and experience from interactions with investors and other financial professionals. Further, statements on where the most attractive risk/reward asymmetry lie, although based on observable data, reflect the opinion of Running Oak Capital.

*Statement regarding Mid Cap stocks outperforming Large is reflective of historical performance of the Russel Midcap Index vs Russell 1000 Index.

*Statement regarding “less than half of the downside risk of the S&P 500” refers to the extended history of the investment strategy, which includes unaudited performance predating the inception of Running Oak Capital in 2013, which was documented and generated on a real time (not back-tested) basis. Such results are from accounts managed at other entities prior to the formation of Running Oak Capital. Downside risk refers to the average downside capture ratio over the time period.

*Source of Mid Cap undervaluation & Large Cap overvaluation: Bloomberg

Latest articles

This data feed is not available at this time.

Data is currently not available