Walmart Inc.’s WMT U.S. segment delivered a solid performance in the third quarter of fiscal 2026, with comp sales rising 4.5%. This growth was supported by increases in both transactions and unit volumes, signaling broad-based consumer engagement rather than reliance on only pricing. Traffic gains were seen both in stores and online, underscoring the strength of Walmart’s omnichannel setup.

Management pointed out that comp sales were positive across each month of the quarter, suggesting stable demand rather than a one-off seasonal or promotional spike. Share gains were also described as broad-based across income groups, with upper-income households continuing to shop at Walmart more frequently, while middle-income customers remained steady. Even as lower-income consumers faced pressure, Walmart’s value positioning helped sustain traffic.

Efforts to enhance convenience and speed played quite a role in boosting transactions. Faster fulfillment resonated strongly with customers, with a growing share of digital orders delivered within three hours. Management emphasized that customers are responding positively to these convenience enhancements, which are increasingly central to Walmart’s U.S. comp sales performance.

WMT expressed confidence that the underlying drivers of transaction growth remain intact as the company moves into fiscal 2026. A continued focus on value, disciplined pricing actions and faster fulfillment is expected to support sustained customer engagement. While the consumer environment remains dynamic, Walmart’s ability to attract shoppers across income levels positions U.S. comp sales to continue being driven by transaction growth.

What the Latest Metrics Say About Walmart

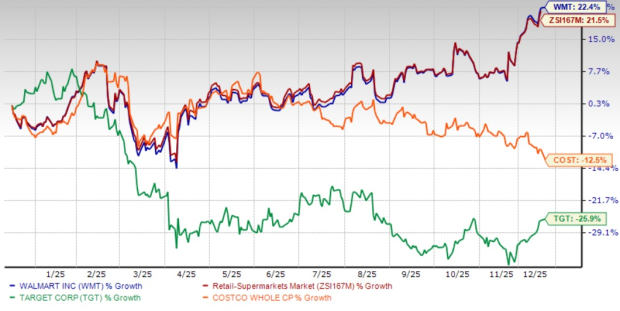

Walmart, which competes with Costco Wholesale Corporation COST and Target Corporation TGT, has seen its shares rally 22.4% in the past year compared with the industry’s growth of 21.5%. Shares of Costco have declined 12.5%, while Target tumbled 25.9% in the aforementioned period.

Image Source: Zacks Investment Research

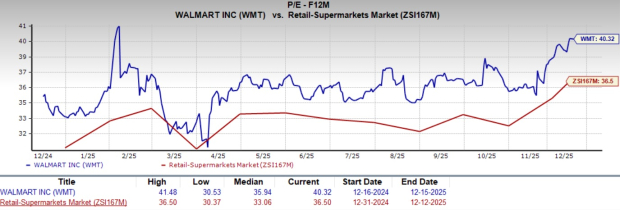

From a valuation standpoint, Walmart's forward 12-month price-to-earnings ratio stands at 40.32, higher than the industry’s 36.5. WMT carries a Value Score of C. Walmart is trading at a premium to Target (with a forward 12-month P/E ratio of 12.71) but at a discount to Costco (41.81).

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for Walmart’s current financial-year sales and earnings per share implies year-over-year growth of 4.5% and 4.8%, respectively.

Walmart currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks Naming Top 10 Stocks for 2026

Want to be tipped off early to our 10 top picks for the entirety of 2026? History suggests their performance could be sensational.

From 2012 (when our Director of Research Sheraz Mian assumed responsibility for the portfolio) through November, 2025, the Zacks Top 10 Stocks gained +2,530.8%, more than QUADRUPLING the S&P 500’s +570.3%.

Now Sheraz is combing through 4,400 companies to handpick the best 10 tickers to buy and hold in 2026. Don’t miss your chance to get in on these stocks when they’re released on January 5.

Be First to New Top 10 Stocks >>Target Corporation (TGT) : Free Stock Analysis Report

Walmart Inc. (WMT) : Free Stock Analysis Report

Costco Wholesale Corporation (COST) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.