Key Points

Walmart's price-to-earnings multiple of 45 is high in relation to the S&P 500.

The business has been resilient over the years, but its growth rate is typically in the single digits.

- 10 stocks we like better than Walmart ›

Walmart (NASDAQ: WMT) is an iconic big-box retailer that customers rely on every day for both necessities and discretionary purchases. And the company's resiliency over the years has made it a go-to investment for all types of investors.

Over the past 12 months, it has risen by 28% in value, which has pushed its valuation to a market cap of just over $1 trillion. It's a huge milestone for the business, symbolizing just how special it really is, with it being one of the only non-tech stocks in the trillion-dollar club. But does that also mean the stock has become deeply overvalued?

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Image source: Getty Images.

Just how expensive is Walmart's stock?

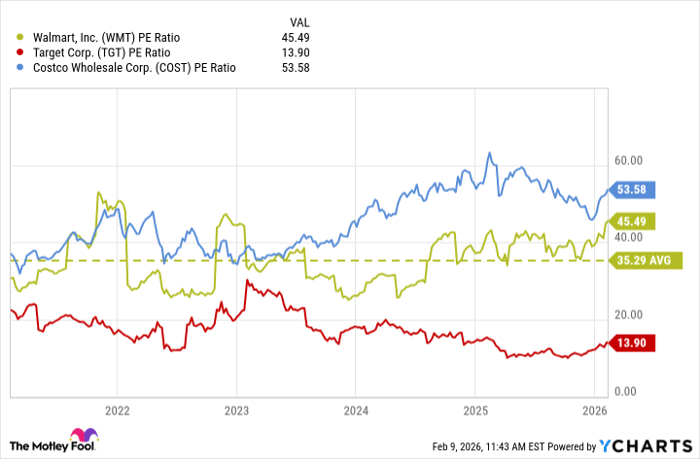

A $1 trillion market cap may sound high, but to truly gauge how expensive or cheap a stock is, it's important to turn to the price-to-earnings (P/E) multiple, which puts the valuation into context of earnings. Currently, Walmart's stock trades at a P/E of 45. Here's how that compares to other retail stocks.

Retail PE Ratios data by YCharts

There's a wide discrepancy between what investors are willing to pay for poor-performing retail businesses (such as Target) versus ones that are doing exceptionally well, like Walmart and Costco Wholesale. But the big question is whether valuations have gotten out of hand; Walmart's five-year average P/E ratio is 35. And the S&P 500 averages a multiple of just 25.

Investors have been loading up on safe-haven stocks such as Walmart in droves, and that has driven its valuation incredibly high. The problem is that its growth rate may not be high enough to suggest that the premium is warranted.

Why the valuation looks troubling

Walmart has a fantastic business. It has been growing online, and its acquisition of Vizio in 2024 opened up new opportunities for its advertising business. But despite all that, its growth rate remains in the single digits. When it last reported earnings in November, its growth rate was around 6%. It's a solid rate, but to pay 45 times earnings for a stock that's growing that much is difficult to justify. Normally, stocks that are trading at such high premiums have exceptionally strong growth rates, but that isn't the case with Walmart.

As great a business as you think Walmart may be, that doesn't mean that its stock is a good buy at any price. If you pay a high premium for a stock, that could result in limited gains or even losses, despite the business itself being strong. That's why I'd avoid Walmart's stock, as it is far too expensive to buy, and there are plenty of other retail stocks that can make for better long-term investments today.

Should you buy stock in Walmart right now?

Before you buy stock in Walmart, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Walmart wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $443,299!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,136,601!*

Now, it’s worth noting Stock Advisor’s total average return is 914% — a market-crushing outperformance compared to 195% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of February 9, 2026.

David Jagielski, CPA has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Costco Wholesale, Target, and Walmart. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.