Credit: Shutterstock photo

Credit: Shutterstock photoBy Matt Hylland :

Uncovering any type of value has been tough in this market.

Stocks are trading at their highest multiples in years after nearly a decade of rising stock prices. Even with the 2008 financial crisis, the S&P 500 has had just 1 negative year in the last 15 - a feat that has happened only once before in history (1982-1999 is the only other 15+ year period with only 1 negative year). The CAPE ratio is at a level above 30, a level which has never produced positive 10-year returns. The S&P 500's dividend yield is now below the 10-year treasury, something that last occurred a decade ago.

Historically, at times when stock markets have been so expensive, bonds have offered yields to help reward patient investors unwilling to invest in an expensive stock market. Before 2008, 10-year treasury bonds yielded 4.5%. Prior to 2000, that same bond yielded over 6.5%! But today, bonds are offering generational low interest rates that even in today's low inflation environment yield real returns around 0%.

But getting out of your comfort zone may prove worthwhile. Below we will look at a publicly traded third party trust that holds high yielding bonds in a specific company. However the trust is valued 38% less than the market value of the bonds that are within the trust.

We will then explore the ways to hedge our investment to eliminate credit risk in its underlying holdings. For large investors this is easy to do, but small investors need another option. We will use the findings of a 2011 academic paper to construct a put option position to completely hedge our position, theoretically leaving us with a 6.8% net annual yield and hopefully a one time 38% gain - completely independent of the general stock market's return.

What Are Third Party Trust Preferreds, Securities, Trust Certificates, etc?

First, and maybe most important to know before you invest in these - what are they?

To start, pretend you are a company looking to raise money from investors. You have 3 main choices; issue stock ( equity ), issue preferred shares, or issue bonds ( debt ).

Each option has its own benefits and drawbacks.

Issuing shares may seem as easy as printing money, and many companies act just this way, but the process also dilutes current shareholders (angry shareholders are never good!) and may also cost the company more in dividend payments if the company currently pays a dividend.

Issuing preferred securities will not dilute common shareholders, and for financial institutions can be an alternative source of tier 1 capital, but will likely come with a higher dividend cost that is ultimately more expensive for the company as dividends are not tax deductible.

Issuing debt also results in no dilution for current shareholders, but comes with interest payments. Also an advantage, interest paid on debt can be tax deductible, making $1 spent paying back debt ultimately cheaper for the company than $1 paid to investors through a dividend on preferred or common stock.

Many companies prefer selling bonds, however many retail investors avoid investing in individual bonds for a variety of reasons; commissions and price spreads can be high, the bonds may require large minimum investments - making it hard for retail investors to remain diversified by buying the security, or they may be concerned about the lack of liquidity in many individual bonds.

Trust Securities - Why do these securities even exist?

These type of securities offer a compromise.

To help bridge the gap between a retail investor and a company, a trust is created either by the company or by a third party which buys bonds that will be held in the trust. The trust sells certificates (effectively shares) of the trust to investors that represent ownership of a certain portion of the trust. These shares can be at a much lower price than a bond, say $10 or $25, and sold to the general public.

As interest to the underlying bonds held by the trust is paid, it is then paid out proportionally to the certificate holders of the trust.

Some of these trusts are pretty simple in their setup (like the one discussed today) and hold a single security, others may be more complex with multiple holdings. These trust shares are typically called third party trust preferreds, or asset backed securities, and despite the name do not necessarily have to hold or issue preferred shares.

These securities are also more convenient for investors in a few different ways:

First, investors in third party trusts that own debt are treated as bondholders, meaning that in a case of bankruptcy, they would be given better treatment than preferred stock or common stock holders. As we will find out when looking at this company's balance sheet - that may become important.

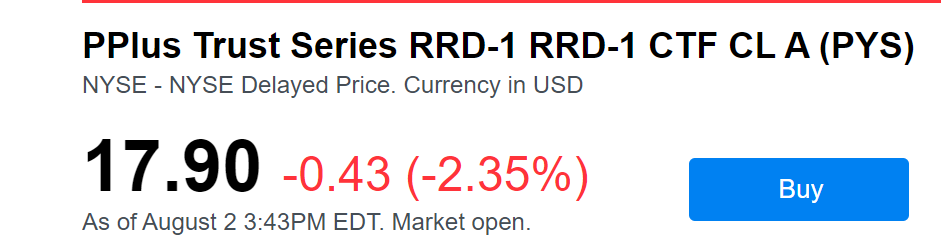

Next, this investment will have a much lower minimum for investment. Bonds will typically require a minimum order of $1,000, $5,000, or even $10,000. These third part trust preferreds just require you to purchase 1 share, which in this case of the security we are looking at today is $17.90.

Lastly, these securities offer more liquidity than their underlying holdings, hopefully making them easier to buy and sell.

A Third Party Trust With A Potential For Upside

The security I want to look at today is traded under the ticker symbol ( PYS ), and is called:

'Merrill Lynch Depositor PPLUS Trust 6.30% R.R. Donnelley Certificates RRD-1'

The prospectus for the security can be found here: https://www.sec.gov/Archives/edgar/data/1354371/000094787106000399/f424b5_022406-rrd1.txt

While we will spend most of the time discussing the securities that trade under the symbol PYS, note that there are many others. Here's a quick list that may help eager readers to find other opportunities:

Note, many of these are different than PYS. Some hold floating rate securities, while others hold only fixed rate securities. Some hold junk bonds (for example: 100 year JC Penny bonds), others hold very high quality securities (such as Goldman Sachs bonds). I am including the list below as an example to show that this is a somewhat common practice, not asinvestment adviceor to highlight other securities that offer the same value as PYS.

Ticker Symbols are listed below, links direct you to the prospectus of the issue.

- GYB - Prospectus

- GYC - Prospectus

- PFH - Prospectus

- JBK - Prospectus

- IPB - Prospectus

- PYT - Prospectus

- PIY - Prospectus

- HJV - Prospectus

- JBN - Prospectus

- JBR - Prospectus

- KTN - Prospectus

- KTBA - Prospectus

- KTP - Prospectus

- KTH - Prospectus

- GJH - Prospectus

- GJO - Prospectus

- GJP - Prospectus

- GJR - Prospectus

- GJS - Prospectus

- GJT - Prospectus

- GJV - Prospectus

So, if you are bored and need some reading, those prospectuses should keep you busy for a while, but now back to the primary security I want to discuss:

A Look At PYS

So, buying a share of PYS is buying a share in a third party trust that owns corporate bonds.

But what exactly are you buying?

The Assets in PYS

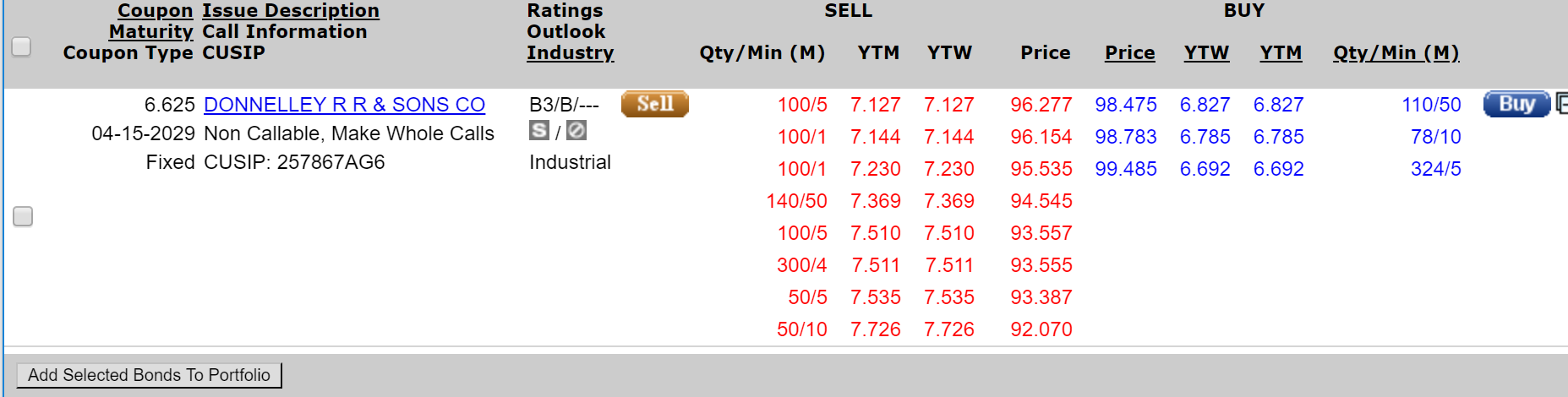

The trust is funded solely by $60,000,000 in bonds that mature in 2029 from R.R Donnelley & Sons, a publicly traded stock with the ticker symbol: ( RRD )

The bonds have a 6.625% coupon.

The underlying securities have a CUSIP number of 257867AG6.

These bonds are available for purchase outside of the trust as well, you can buy these bonds today at your broker:

If you just buy the bonds today, you can get a yield around 6.82% (lower if you need a smaller minimum - again showing the benefits of PYS instead of the bonds).

These bonds are the only assets that make up the trust.

Class A shares of the trust (which are what you buy when you purchase PYS), are entitled to receive 6.30% of interest from the bonds, or $1.575 per share per year in interest payments - $0.7875 paid semi-annually in April and October. With the price of PYS today, that's an 8.8% yield, quite higher than the underlying bonds that make up the trust, and the first glimpse of the mispricing that I believe exists in PYS today:

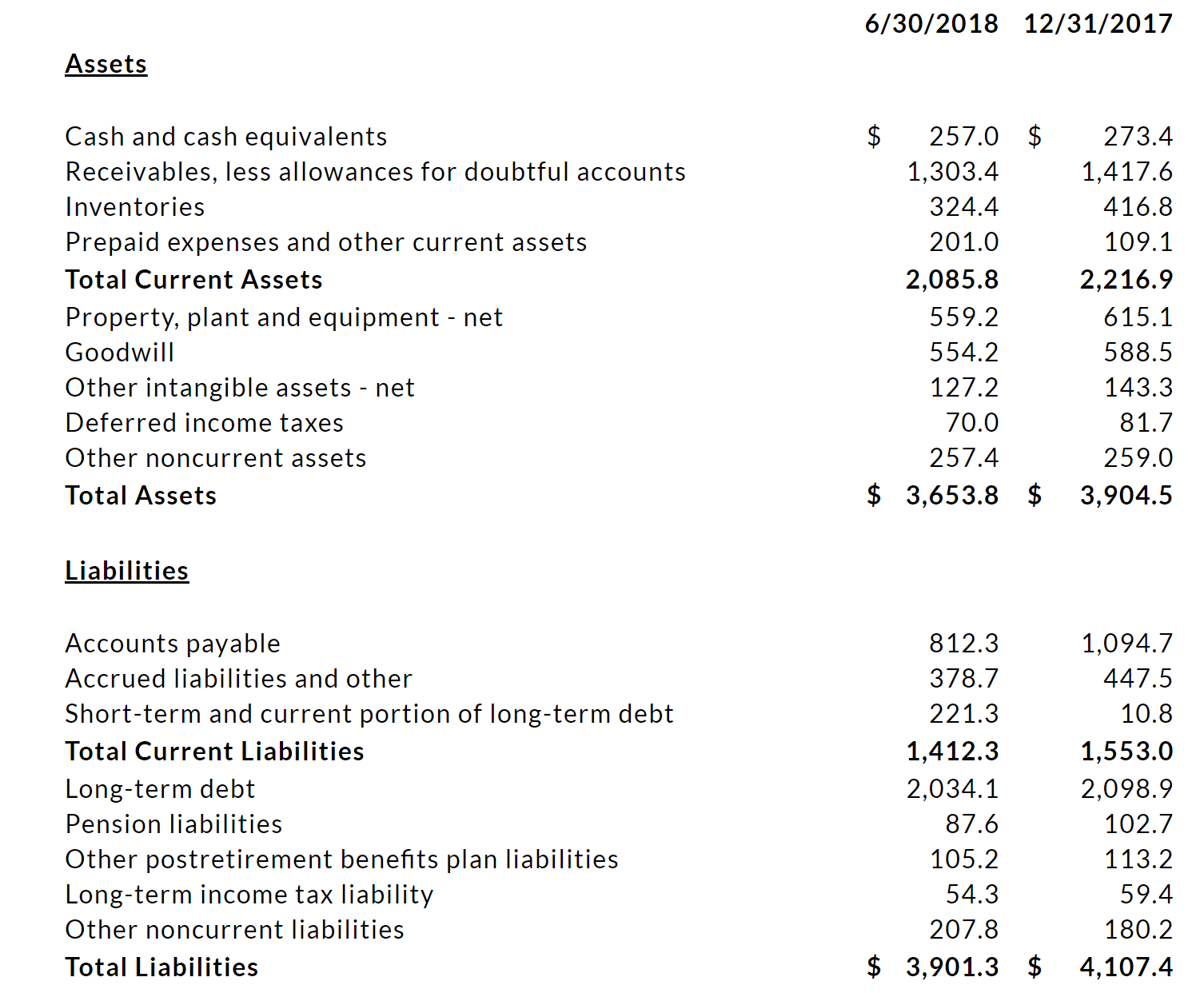

On top of that, their balance sheet is not the best I've seen:

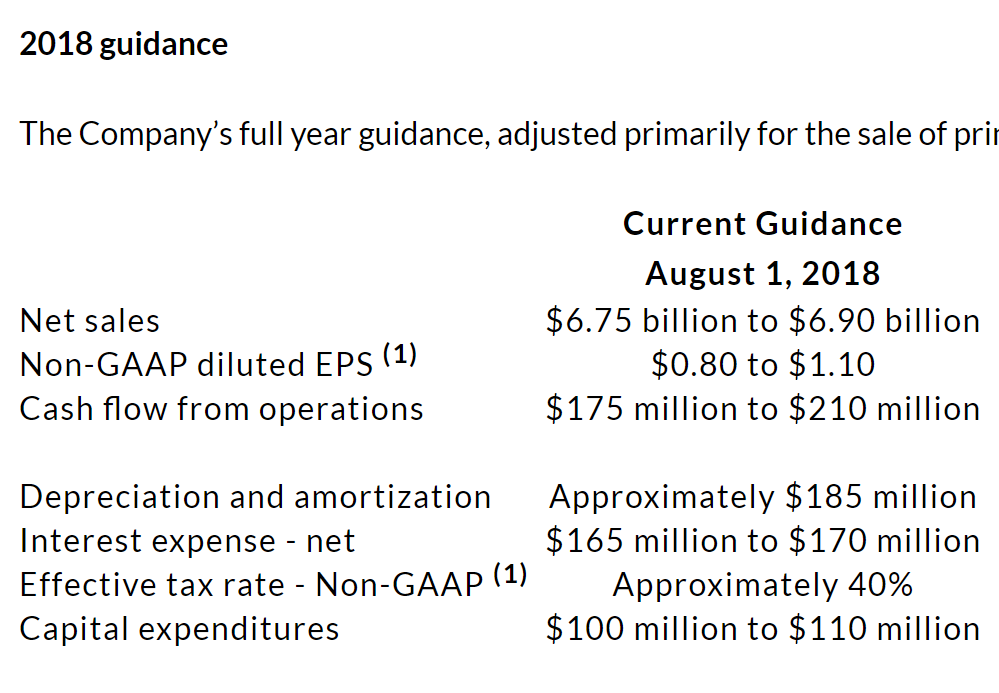

But, if you believe management, the company is turning around:

By management's guidance, it looks like RRD should be able to pay the bills.

But I don't want to wager my whole investment on management's guidance, because if they are wrong, even by 10% of estimated cash from operations, it gets tough for the company to pay the bills.

So I want some protection on my PYS purchase.

Option 1: Adding A Short - Making an Arbitrage Opportunity

When Warren Buffett ran his investing partnership in the late 50s and early 60s, he was not just buying stocks that he liked. In fact, he split his portfolio up into three different types of investments; "Generals", which were simple buy and holds, "Controls", which is buying entire companies, and "Workouts" which were arbitrage type of investments where Buffett saw special events or scenarios with a more market-independent return.

Here is how Buffett explained his investment style in his partnership letter summarizing the results from 1963 :

A workout, or arbitrage, type of investment *should* make money regardless on the direction of the market. Obviously there are times when general investments will do much better (think 2017 when stocks rose significantly), but in a down market, arbitrage types of investments will be superior. Over long periods (10-15 years) Buffett thought the returns in his fund from arbitrage investments would be about equal to his general investments.

And right now, the idea of adding more market neutral types of investments is appealing to me as it gets harder and harder to find good "general" investments today. The problem is they are hard to find.

So, we know that PYS holds bonds that yield 6.8% today, but the shares of the trust have sold off significantly to where the trust now yields 8.8% - much higher than the bonds.

But just buying PYS could be risky. R.R. Donnelley is in debt, and is struggling to make ends meet. If R.R. Donnelley defaults, the price of PYS will drop significantly.

What can we do to help eliminate the risks of simply owning PYS - Effectively turning this into a "workout" type of play instead of a "general" investment? And is there a chance it can actually produce a reasonable return?

Short the Underlying Bonds

Well first, we can simply short the bonds that make up the holdings of PYS.

Buying PYS pays you an 8.8% yield, the bonds pay 6.8%. So, buying PYS while shorting the bonds requires you to pay 6.8%, but you are getting 8.8% from PYS, so depending on your borrowing costs, you may be able to make some money there.

But the more rewarding scenario would be to see this pricing gap close. After all, these are effectively the same security! In an efficient world, PYS would eventually trade closer to the bond's yield.

What kind of return could an investor expect if they short the underlying bonds and buy PYS?

The bonds have a coupon rate of 6.625%, but currently yield 6.8% since they trade at a 1.525% discount to par.

If you read the PYS prospectus, you read that that the trust has split the 6.625% bonds into two separate securities. The A Class shares, which you buy by purchasing PYS, yield 6.30% at par. The B Class shares (which are not listed on an exchange) are given 0.325% yield at par.

The class A shares currently trade at $17.90, a steep discount to their par value.

If this gap closed completely, that is PYS traded at a similar discount to par that its underlying bonds trade at today, PYS would trade at about $24.61 - a 38% increase from today's price!

To me, based on the value of the underlying holdings in PYS, right now the fair value of PYS is somewhere around $24.61.

And remember, the idea of this trade is not to make a bet on whether R.R. Donnelley survives. This should be set up to be neutral whether R.R. Donnelley stock goes to $0 or $100. The idea is to capitalize when this spread narrows.

So, this should be easy to accomplish: For every 55 shares of PYS that you buy, short $1,000 in par value of the underlying bonds. (This is based on today's prices)

This option is very likely the best way to go to capitalize on this price difference.

But…

This option is unfortunately easier said than done for most investors. Shorting individual corporate bonds will likely require large amounts of capital and the right broker. So for you big investors out there, the option above represents a good play in my opinion. But small investors will not be able to do this. Fortunately, I think small investors have a way to play this too…

Option 2 - Buy PYS, Add Additional Downside Protection Using Put Options

The risk of buying PYS is that R.R. Donnelley defaults on the bonds and goes bankrupt. Shorting the bonds would work to eliminate that risk, but as we just mentioned, that is not possible for many small investors.

Buying credit default swaps ( CDS ) are another very common way that large institutional investors protect themselves from default. CDS act as insurance, paying out if the company goes into default. But, unfortunately for small investors, CDS are not available.

But there is one other way to protect our investment from an R.R. Donnelley default - Put options.

This is not quite a 1:1 hedge of risk like option 1 above. Let me say this again - This is not a perfect arbitrage setup - But there is some academic research showing that put options can produce returns exactly the same as a credit default swap ( CDS ) in the event of a bankruptcy.

One specific quote from the summary section of paper linked above:

While shorting individual corporate bonds is likely not to be possible for most retail investors. Buying options is.

A put option on R.R. Donnelley common stock will rise in value if the company's stock price declines.

Our main concern when buying PYS is that R.R. Donnelley will not be able to pay their bonds' interest payments, default, and go bankrupt.

In the event of bankruptcy, the common shares will likely be worth $0. Put options give us a way to make money on that situation and hopefully hedge our risk to R.R. Donnelley's credit risk. In fact, the purchase of a single, Deep-Out-Of-the-Money ( DOOM ) put option can act just like a CDS!

So, it just means finding the right put options to counteract R.R. Donnelley's credit risk that we are taking by buying PYS. Here's the options available that expire March 2019, which I think should give us enough time to see PYS's spread narrow a bit from its underlying bonds (if not, we can always roll these into later options).

We are a little limited here because of the low volume in RRD options, but we can still make this work.

Example: How To Hedge R.R. Donnelley Credit Risk Using Put Options

For this example, lets assume we are investing $10,000 in PYS. We want to protect that $10,000 in the event of a credit event, how many, and which put options should we buy?

Because we are limited by the open interest in these options, the $4 puts look to be the only option with ample liquidity.

Let's assume in the case of a default that bond holders would get 40 cents on the dollar (40% recovery rate).

In this case, we need to protect 60% of our $10,000 invested in PYS - $6,000.

To calculate the number of contracts that we need to purchase:

($ Protected ÷ Option strike price) ÷ 100

or, ($6,000 ÷ $4) ÷ 100 = 15

We need to purchase 15 $4 put options to protect our $10,000 PYS investment.

Each option will cost us $45 if we purchase at the ask right now. (Though, this is overpaying. A Black-Scholes option calculator says they should be 32 cents)

15 contracts at $45 costs us $675. (If we are patient, we should be able to get 15 contracts around $525).

So at today's prices currently being offered, we can buy these contracts for $675 to completely protect $6,000 of our investment in PYS.

Remember, $10,000 invested in PYS would pay $880 in dividends annually, more than covering the cost of the put options.

So, in total we can collect $205 per year (about 2.05%), and hopefully eventually collect 30-40% as the spread between PYS and its underlying bonds narrow, all completely independent from the general market's direction.

In Theory It Should Be Better

I used the $4 put options because they are currently the lowest strike price that has any implied interest. But I think patient investors could squeeze out even higher total returns if liquidity comes to lower strike price put options.

A $3 put should have a fair value price around 7.2 cents today - let's call it 10 cents.

Using the same equation above, we should be able to purchase 20 put option contracts with a $3 strike price for 200 dollars today, leaving us with a 6.8% net yield ($880 - $200 = $680 or 6.8% on $10,000) on PYS, and ample protection should R.R. Donnelley fail.

In other words, we should be able to collect 6.8% per year ($680 per $10,000 invested), until this gap in PYS's underlying bonds narrows - which could net up to 38% ($3,800 per $10,000 invested). Ideally, this return should come regardless of whether or not the market goes up, down or sideways.

Why Does This Opportunity Exist?

One thing I always try to ask myself when thinking of a trade is - "why?".

Surely a thousand investors can find this opportunity - so why do I think it still exists? What are others seeing that I am not? To be honest, I'm not totally sure, but here are a few ideas:

Liquidity

PYS has very little liquidity, it trades ~4,000 shares per day on average (a total value of $80,000 or so). It is well known that illiquidity drives a discount. This could be a small source for the difference in price between PYS and its underlying bonds.

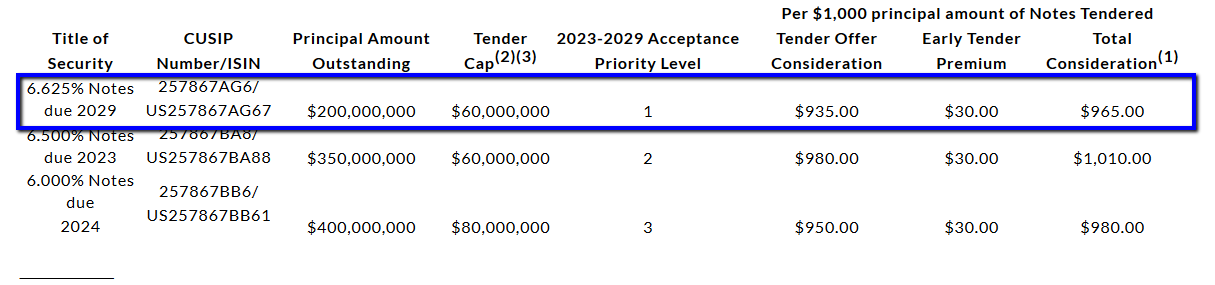

Recent Tender Offer

Also, R.R. Donnelley put out a tender offer not long ago to buy back many of the 2029 maturity bonds:

The company purchased more than a a quarter of the bonds outstanding a year ago - perhaps affecting the price of the bonds, but having no direct affect on PYS.

Indexing

We talked early on in the post about how many investors choose not to purchase individual bonds. Today's low cost ETFs and mutual funds make it very easy to be exposed to corporate bonds. These ETFs and mutual funds are likely buying the R.R. Donnelley bonds that make up the holdings of PYS.

However, there are no similar ETFs buying the trust PYS itself. So, it is very easy to imagine that in today's highly indexed world, the bonds in PYS are seeing large bids, while PYS itself is not.

Conclusion

PYS is seems underpriced based on the underlying securities of the trust. Today, there are ways for any investor large or small to capitalize on the mispricing without taking much credit risk.

In today's market, I think it is an intriguing opportunity worth pursing.

I also feel like this article deserves an extra clear disclosure: I make no guarantee to the accuracy or completeness of any of the information or analysis presented. I may be just too desperate to find a source of value in this market, anchored to low yields, or missed some valuable piece of information somewhere.

(This post was originally published at begintoinvest.com)

See also Geospace Technologies Corporation 2018 Q3 - Results - Earnings Call Slides on seekingalpha.com

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}