Understanding Investment Styles

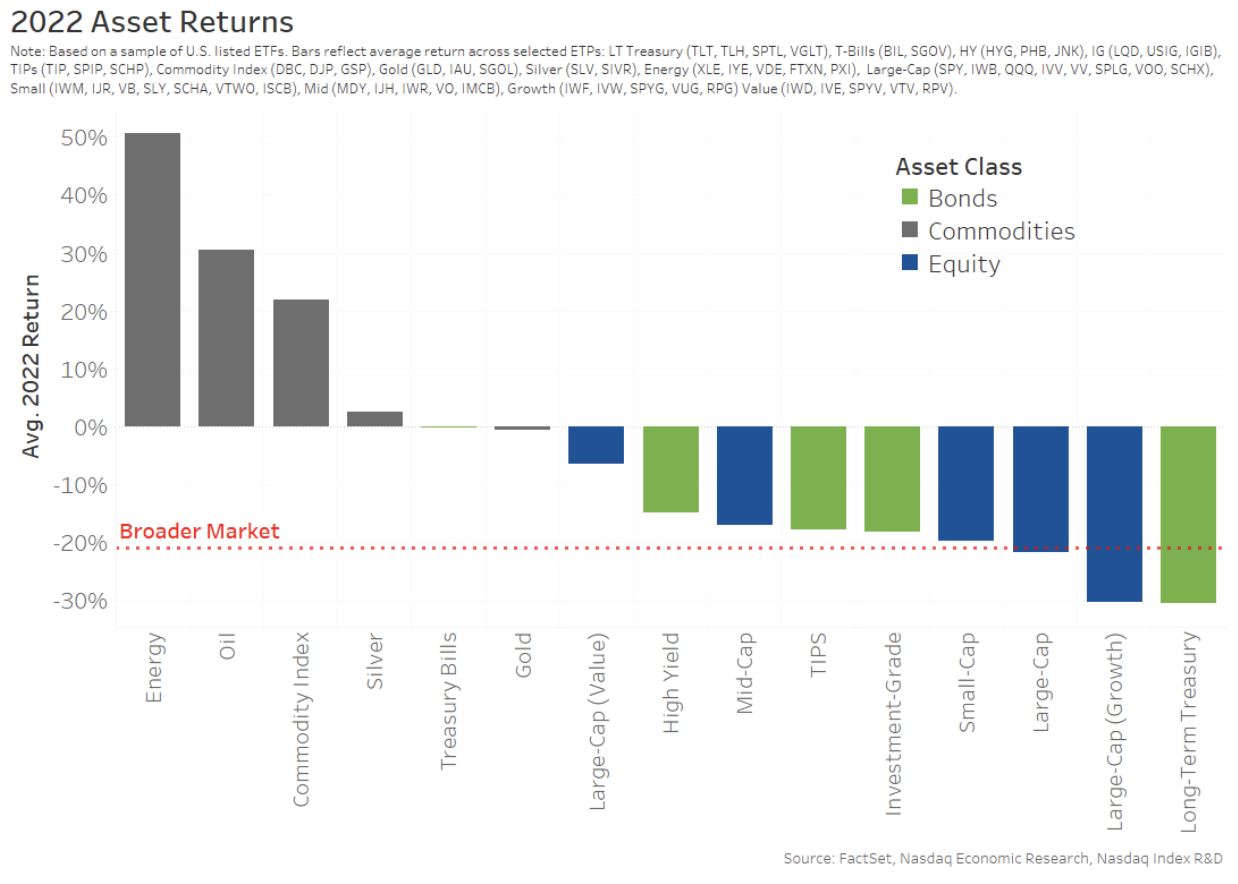

We recently talked about how bonds and stocks both fell during 2022, with U.S. equities (NQUSB™) declining 21% and U.S. bonds (AGG) down 15%. We’ve also shown how those returns were driven by rising rates in response to inflation.

What is more interesting is how some types of stocks performed better (and worse) than the broader market. So-called ‘value’ stocks outperformed ‘growth’ stocks, and (to a lesser degree) smaller stocks somewhat outperformed larger stocks.

Today we dive into the different ways to segment stocks and build portfolios that might outperform the market for specific periods of time.

Chart 1: Value stocks and small-cap stocks outperformed the broad market last year

How do portfolio managers pick stocks?

It’s the job of many mutual fund portfolio managers to try to build portfolios that outperform the broad market. They do this by picking stocks that they think will perform better given where things like the economy and company earnings are going.

Some portfolio managers analyze the accounting statements and business opportunities of each company separately to see which businesses are likely to perform better in the future.

But others classify stocks based on groups of similar characteristics known as factors.

Some of the more common factors are available in ETF form and include:

- Size: Comparing small-cap companies and large-cap companies.

- Style: Value companies are meant to give good returns compared to their upfront investment, while growth companies are expected to grow faster — both of which should make a stock more attractive for investments.

- Momentum: Looks at whether a stock is rising or falling, with the expectation that the trend could continue.

- Quality: Typically looks at more fundamental metrics, like leverage and management and earnings stability.

Table 1: Common Factors Used to Segment Stocks

Today we focus on the most common factors: size and style.

How does “Size” work?

Size is the easiest factor to understand since most of us know which are large companies and which are smaller companies. Size as a factor is typically based solely on the market cap of the stock.

Large companies have some benefits – they often dominate their industries, giving them more economies of scale and more customers. A stronger balance sheet can also reduce financing costs.

However, being smaller can be an advantage too. Often, there are more opportunities to grow revenues and expand to new customers. Smaller management teams can also make it easier to innovate with new products or at least focus on doing market niches really well.

For an example of how size portfolios can be constructed, our blog last week looked at how different ETFs cover the Nasdaq-100® market cap spectrum. With ETFs tracking the large-cap Nasdaq-100 (NDX), the mid-cap Nasdaq Next-Gen™ (NGX) and the small-cap Nasdaq Innovators Completion™ (NCX) (Chart 2). Chart 2 also shows that larger companies have more daily trading, which can make it harder to build small-cap portfolios.

Chart 2: Market-cap spectrum of Nasdaq-listed securities, colored by the constituents in different-sized portfolios

How does “Style” work?

Style, on the other hand, is usually determined based on more detailed firm-specific accounting data.

Style is typically split into “value” or “growth,” but in reality, what makes a company a growth company is different than what makes them a value company. For example, Nasdaq indexes:

Scores a company for growth based on:

- Higher rate of historic sales growth

- Higher historic earnings growth rate

- Price momentum, which will capture market expectations for future growth

While the accounting data used to score companies for value are different:

- Lower price-to-book ratio

- Lower sales-to-enterprise value ratio

- Lower price-to-earnings ratio

In theory, with a value company, each dollar you invest buys you more underlying assets or sales or earnings than other companies offer. It’s similar to how you might think about buying a house or a car; you want more features for the same price.

In contrast, a small company with no earnings now would look like poor value based on historic earnings. But if they grow to be one of the largest companies, their future earnings might justify a significant valuation. Because stock markets are good at pricing in those future expectations, companies expected to grow faster usually cost more per unit of historic earnings (they have higher price-earnings multiples).

How should you think about factor portfolios?

As the economy and consumer trends change, it often creates opportunities that benefit specific types of companies.

For example, we saw above that rising interest rates affected growth companies much more than value companies. We also saw that global events made energy companies more profitable, helping them to outperform. And during Covid, we saw that consumer behaviors changed in ways that benefitted companies with non-touch services over in-person services.

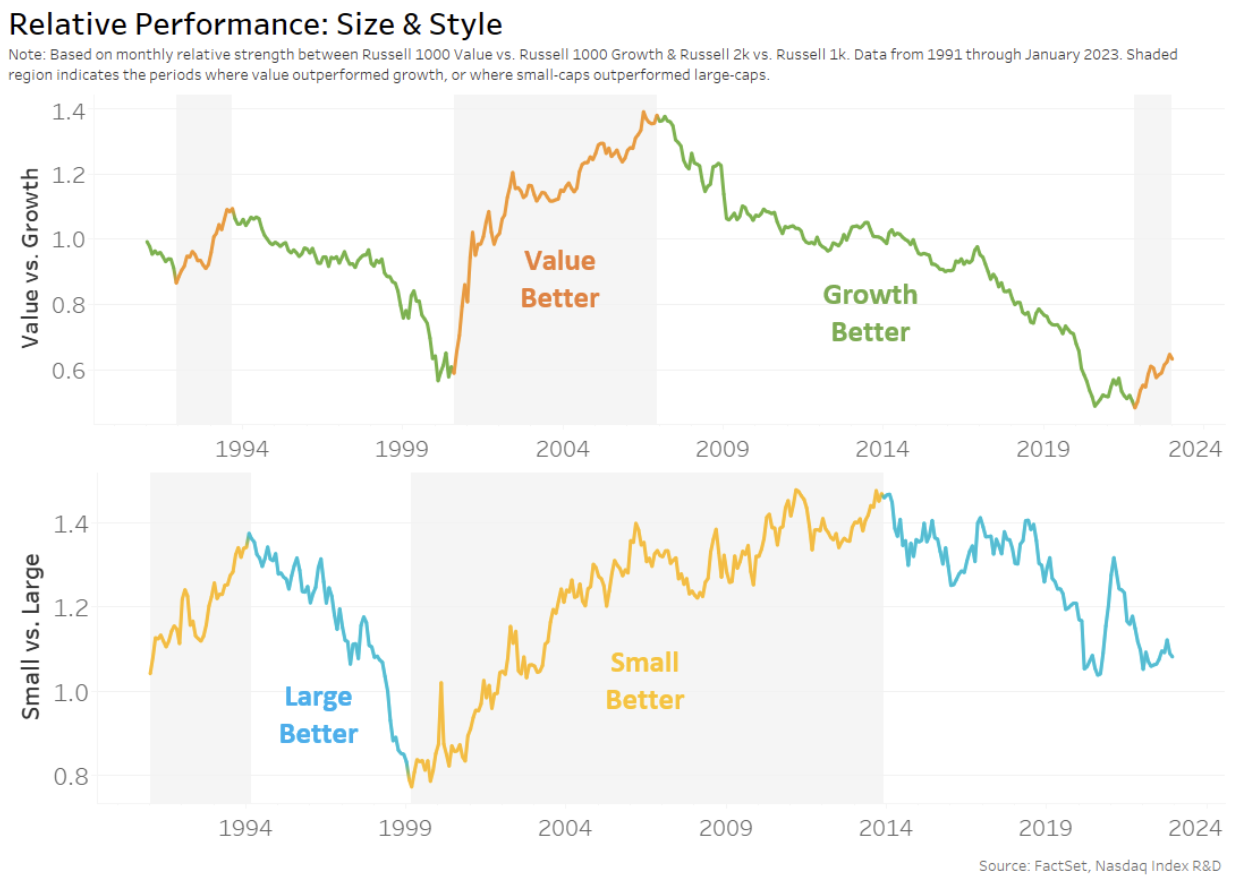

In fact, if we look over long periods of time (Chart 3), we see that style and size factors tend to experience years of over and underperformance. We also see clearly that the turning points for performance of different factors are different, indicating that different underlying drivers change different factor returns.

Chart 3: Styles go in and out of favor

Factor scoring U.S. ETFs

We mentioned earlier that there are a number of U.S. equity ETFs that allow investors to make factor investments. In fact, if we look across the spectrum, it is possible to classify almost all ETFs as some combination of size and style.

In Chart 4 below, we attempt to categorize all the U.S. equity ETFs using a technique called Returns-Based Style Analysis (RBSA).

First, we look at the returns for four Nasdaq style indexes (large-cap growth, large-cap value, small-cap growth, and small-cap value) that were built by classifying underlying companies into each portfolio using the fundamental metrics we discussed above.

Then we mathematically regress the returns of each ETF against the four Nasdaq style indexes, with some constraints. The closer the returns of a portfolio match each of these underlying indexes, the closer that ETF goes to the corner representing that index.

Applying this technique shows that the range of all U.S. Equity ETFs also represents a range of exposures to size and style factors. A ticker like:

- XLE (the energy sector ETF) is currently strongly value but also very large cap (bottom right corner).

- FTCS (tracking a capital-screened index) and RDVY (tracking companies with rising dividends) both also have a larger-cap-value tilt.

- QQQ (tracking Nasdaq-100) has a large-cap-growth tilt (upper right), whereas QQQJ (next in line for NDX) has a smaller tilt relative to QQQ while still maintaining the overall growth tilt.

- IWM, the market-wide Russell 2000 index fund, sits to the left (small) but almost on the axis (highlighting the combination of value and growth small-cap companies in its index).

- QUAL, despite picking stocks based on balance sheet stability metrics, is actually quite a large-cap growth portfolio.

- YOLO, the ETF designed for MEME stock traders, is very small cap but also has quite a high growth score.

Chart 4: Scoring U.S. ETFs across the size and style spectrum

Also note that the circles (ETFs) in Chart 4 are colored by 2022 relative performance versus a “total market” index (NQUSB, the Nasdaq US Benchmark Index™).

There are roughly the same number of green (outperformance) and red (underperformance) circles. We also see that, in 2022, most of the green was at the bottom of the chart. That shows how the value factor dominated the growth factor as interest rates rose. However, some growth ETFs still outperformed, like ICLN (with exposure to Biden’s clean energy initiatives) and MOAT (which has companies that are attractively priced but also have sustainable competitive advantages).

What does this all mean?

Using some of the same techniques that professional investors use to build portfolios, we can classify ETFs by factor exposure. This shows that although there are thousands of ETFs, most offer a different combination of exposure, even to just these two factors (size and style).

We know that the ETF market ranges from plain-vanilla index portfolios to ETFs with more complex stock selections. This diversity of ETF exposure benefits investors as it enables them to gain targeted exposures based on their investment preferences and views of the economy – helping them build portfolios of ETFs that might also outperform the market.

Of course, there are more factors than just size and style, but we will save that for another day!

Phil Mackintosh

Nasdaq

Phil Mackintosh is Chief Economist and a Senior Vice President at Nasdaq. His team is responsible for a variety of projects and initiatives in the U.S. and Europe to improve market structure, encourage capital formation and enhance trading efficiency.

Read Phil's Bio

Robert Jankiewicz

Nasdaq

Robert Jankiewicz is a Senior Director, Nasdaq Index Research & Product Development, responsible for index product development in the Americas (United States, Canada and Latin America).