It has been a strong few quarters for consumer technology platforms. Inflation is coming down, gross domestic product is growing quickly, and consumer spending keeps climbing.

After worries of an economic malaise in 2022, most world economies have regained a solid footing. Growing consumer spending -- especially in travel and entertainment -- has been a boon to many stocks.

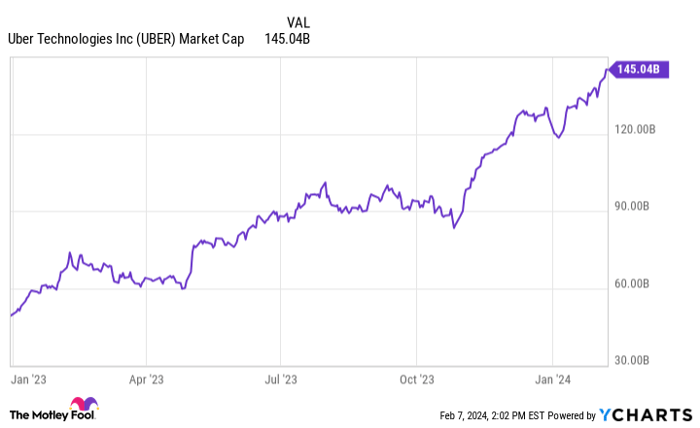

Uber Technologies (NYSE: UBER) is one of the big beneficiaries of a healthy consumer. The stock has soared 185% since the start of 2023, crushing the returns of the S&P 500 over that time frame, which is "only" up 30%. Uber now has a market cap of about $145 billion, making it one of the largest companies in the world.

But the best could be yet to come for the disruptive mobility platform. Should you buy shares of Uber at these prices? Let's investigate further to find out.

Global growth in mobility and expanding margins

Uber disrupted the transportation market with its smartphone ride-sharing app around 15 years ago. Today, it's still gaining market share versus traditional modes of transportation.

In just the last three months of 2023, Uber's mobility segment (which excludes food delivery) posted $5.5 billion in revenue, up 34% year over year. This was on top of 82% revenue growth in the fourth quarter of 2022.

As the dominant ride-hailing application in many markets, Uber has a clear line of sight to continue growing revenue while expanding margins. Its mobility segment's adjusted earnings before interest, taxes, depreciation, and amortization (EBITDA) hit $1.5 billion in the fourth quarter of 2023, growing 43% year over year. That gives it an adjusted EBITDA margin of 26.1% compared to 24.5% a year ago.

Investors used to be worried Uber's ride-sharing business would never be profitable. The company has proved definitively this is no longer a concern.

Can advertising make food delivery profitable?

There is more to Uber's business today than ride-hailing. It has built a formidable food and grocery delivery business called Uber Eats.

Food delivery has been a notoriously tough market, one that has burned billions of dollars in investor capital. Just look at DoorDash, the leading food delivery application in the United States, which posts an operating loss every quarter.

But it looks like Uber might have solved the food delivery profitability issue with a new segment: advertising. Similar to the sponsored listings you see on Amazon, Uber Eats now offers restaurants and other shops the ability to promote their products to users.

In Q4 2023, Uber said advertising hit a $900 million annual revenue rate. This undoubtedly helped the delivery segment grow its adjusted EBITDA 98% year over year to $476 million during the quarter.

Data by YCharts.

Should you buy shares?

With two segments -- mobility and delivery -- expanding margins and growing revenue, Uber is now highly profitable on a consolidated basis. In the fourth quarter, it posted $652 million in operating income for a 6.6% operating margin. This was up from a loss in the same period in 2022.

For the entirety of 2023, Uber generated $37.3 billion in revenue. It looks well on its way to hitting $50 billion in annual sales in the next two to three years. If margins can expand to 10%, this company could be generating $5 billion in operating profits.

The problem is the market already seems to be pricing in this potential. Uber's market cap is $145 billion as of this writing, giving the stock a forward price-to-earnings ratio of 37.

That's more expensive than the market average of approximately 27, which is already close to an all-time high. And remember, these multiples are based on theoretical forward earnings estimates, not what Uber is earning today.

Uber is a good business, but after a nearly 200% rally in the past year and change, the stock looks too expensive. Keep it on your watch list for now.

Should you invest $1,000 in Uber Technologies right now?

Before you buy stock in Uber Technologies, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Uber Technologies wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of February 6, 2024

John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool's board of directors. Brett Schafer has positions in Amazon. The Motley Fool has positions in and recommends Amazon, DoorDash, and Uber Technologies. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.