Closed-end funds sometimes give us hard choices ... like do we want high dividends or really high dividends?

Okay, so maybe I'm being a little flippant here--but not much!

A reader got me thinking about this recently, with a question about the differences between the 10.9%-yielding Western Asset High Income Opportunities Fund (HIO) and its sister fund, the 14%-yielding Western Asset High Income Fund II (HIX).

Both are managed by the same team, are in the same asset class (high-yield bonds) and have virtually the same name. So surely they're pretty much the same, right?

Not so fast. In reality, choosing the right CEF is part science and part art, and a deep dive into these two to determine which is, in fact, the best buy is a good way to get a handle on the process. Let's dig in.

Start With the Discount to NAV

I always tell readers that a fund's discount to net asset value (NAV, or the value of its underlying portfolio) is the first thing you want to look at. Typically, the bigger, the better (note I said typically here--there are exceptions). And since these two funds are similar, surely the one with the bigger discount will win out, right?

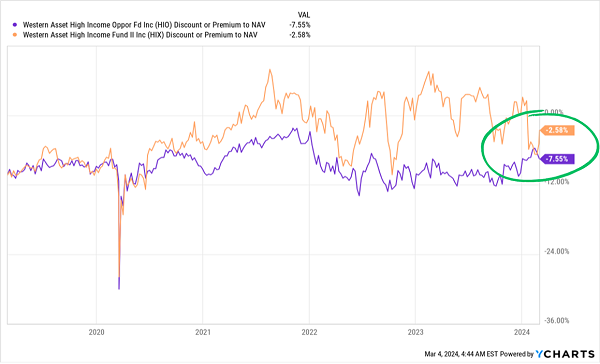

HIO Is Cheaper Than Its Sister Fund

We see here that HIX (in orange) was trading at a bigger discount than HIO (in purple) quite recently, but HIX's bigger 14% yield attracted a lot of interest, so it's now trading at a smaller discount.

In other words, HIX is not the better pick on this front. Note, too, the volatility in HIX's discount: its big moves up and down make it a better swing-trade opportunity, while the more consistent climb in HIO's discount makes it more interesting as a long-term hold.

So which fund wins here? It depends on what you're going for, but if you want long-term income at a discount, HIO seems to have the advantage.

From Discounts to Dividends

We don't just want income, we want reliable income, and that means a fund that hasn't had a history of dividend cuts. So who wins here?

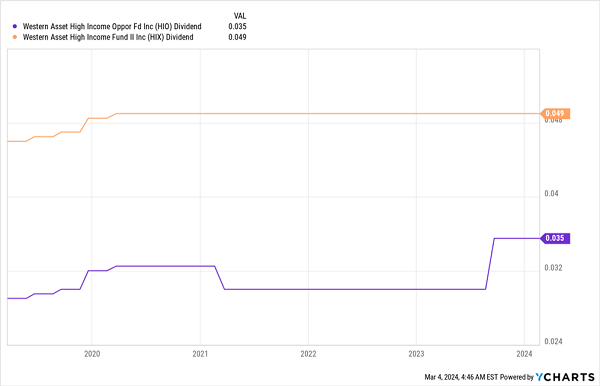

HIO and HIX Both Sport Reliable Income Streams

In both cases, we've seen years of no real dividend cuts, and since HIO (in purple) raised its payouts in 2019 only to cut them back to where they originally were in 2021, I'd say that shouldn't be held against it too much. What's more interesting is HIO's recent dividend hike, which shows that the fund's income stream is becoming more reliable, prompting managers to pay out more.

From that perspective, it does seem like HIO is now a more reliable income provider, especially when we consider that its 10.9% is lower than HIX's 14%. By the way, that mammoth 14% payout is a bit nerve-racking: HIX will have to maintain a very aggressive strategy to sustain it.

That said, what if HIX does cut? It would have to cut 20% for its yield to match that of HIO, and in the meantime you'd be getting a higher yield, so HIX does seem to be the winner here all along--provided you prepare yourself for a payout cut in the next year or so (and provided the cut isn't too big).

So let's call this another tie.

Historical Returns Put Discounts and Yields in Perspective

Income is good, but total returns are where the rubber really hits the road. We can't buy a fund that just returns our money to us; we need our capital to either hold steady or grow. On a total-return basis, how have these funds done?

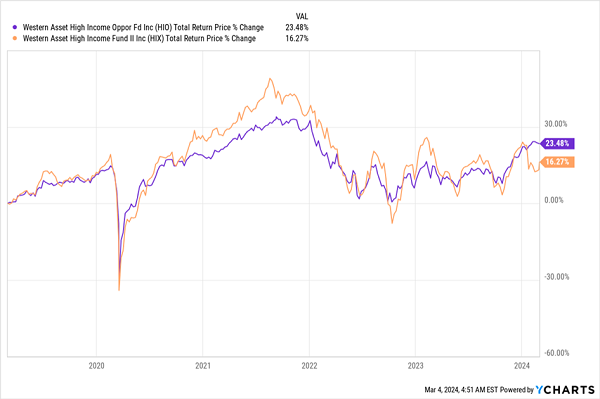

HIO Takes the Performance Prize

This has been a tough time for corporate bonds, and the fact that both funds survived the pandemic and the 2022 freakout--as well as the big interest-rate hikes we've seen--means that both are well managed. But since HIO (in purple) has a higher return, we can say it really is the better fund on this basis.

Pay Attention to Fees (But Remember: Performance Is Worth Paying For)

Finally, how much do these funds cost to hold? While CEF fees are more expensive than those of ETFs due to their active management, we don't want to pay too much: fees cut into performance no matter how you slice it. So is one more expensive?

Management fees for HIX are 1.42% and 0.94% for HIO, so HIO is the winner there. In fact, this difference in fees might account for much of the difference in HIO or HIX's total returns in the past.

Still, HIX's bigger income stream and bigger swings in pricing mean it's likely to get more investor interest when rates are cut (something the Fed has telegraphed will begin later this year). That means HIX might be a short-term outperformer as investors rediscover it when the market begins to price in those rate cuts.

This is especially true since HIX uses leverage and HIO doesn't, which means HIX's leverage costs will fall, as well. And, in theory, its total returns using leverage will rise.

So which fund is the winner? It's a close call, and it depends on your time horizon, but the important point is that both offer something valuable to income investors looking to buy corporate bonds.

Next Step: Build Your 9.2%-Yielding Monthly Payout Portfolio With These 5 CEFs

Before we leave these two bond funds, there's one other thing they both provide that few people realize: monthly dividend payouts. And they're far from the only CEFs that do this: in fact, the majority of the CEFs out there kick out dividends every 30 (or 31) days.

I know that regular readers of this column (contrarian dividend investors they are!) love monthly dividends. There's a convenience factor here, for sure. You can scrap the spreadsheet you use to track your payouts and simply look forward to a new dividend every 30 (or 31 days) from your monthly payers.

But there's more here, because you can also reinvest your payouts faster when they roll in monthly. That's a nice bonus feature of monthly payouts that helps you "optimize" your returns just a little bit more.

Of course, we never want to invest based solely on something like payout frequency. And luckily with CEFs, we don't have to. CEFs from across asset classes offer monthly payouts, and I've assembled the best of them in my 9.2%-yielding monthly payout portfolio.

These 5 highly diversified funds hold utility stocks, S&P 500 stocks, tech stocks, corporate bonds and real estate investment trusts. And they set you up for price upside, too, thanks to their deep discounts.

The best way to get to know these 5 dynamic monthly payers is to check them out for yourself. Click here and I'll share my research on each of them and give you the opportunity to download a free Special Report revealing the names and tickers of each one.

Also see:

Warren Buffett Dividend Stocks Dividend Growth Stocks: 25 Aristocrats

Future Dividend Aristocrats: Close Contenders

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.