Credit: Shutterstock photo

Credit: Shutterstock photoBy John Winsell Davies :

22 July 2015

JWD Weekly Call - The Tribble with Telcos

"Your phone is off the hook, but you're not,"Exene Cervenka/John Doe,X - Los Angeles, 26 April, 1980

Verizon Communications, Inc.( VZ )

Sector: Telecommunications

Industry: Telecom Carrier

Action: Short

The Macro

In 1984, the U.S. Justice Department broke up "Ma Bell," the fixed-line telephone monopoly that dominated consumer telecommunications in America and Canada since being founded by Alexander Graham Bell in 1877. 99% of Americans already had access to a fixed-line telephone in the 1980s, and the Bell System's domination of virtually all facets of the industry stifled competition. Citing anti-free market and anti-consumer business dealings, the DOJ first brought suit in 1977. The Bell System's ultimate demise was determined to be in the interests of the public good. But like most people at the time, I remember initially being unhappy about the breakup, because services went down and prices went up.

American Telephone and Telegraph was divided up into seven regional telecom operators "Baby Bells," Bell Labs, Western Electric, and AT&T ( T ) long distance. With $149.5 billion in assets at the time of the breakup, Bell was the 4th largest company in America after Exxon ( XOM ), General Motors ( GM ), and Mobil.

In some ways, the world has changed less since that day than one might anticipate. The two largest components of the old Bell System today (Verizon Communications and AT&T) have a combined market cap of $376B, making the entity the 4th most valuable company in America after tech titans Apple ( AAPL ) $760B, Google (GOOG) (GOOGL) $461B, and Microsoft (MSFT) $379B. So what has changed? 97% of Americans still have access to a fixed-line telephone in 2015 (a slight decline), but fully 99.5% have access to a mobile phone and 64% are "smart phone" owners (1 April, 2015, Pew Research Centre Report).

Investors in the market-leading telecom carrier and wireless operators, including AT&T and Verizon, enjoy high share prices, solid earnings, and generous distribution of free cash flow in the form of large quarterly dividends.

Executive Summary

So 30 years after the breakup … break out the band and blue skies forever? - No. I am going to take the unpopular position that the good times are over, the sector peaked in 1999 and it is going to get worse from here. Everything changed, but the changes are poorly understood and difficult to recognize at distance.

Incumbent telecom carriers and wireless operators should consider a future of increasingly unattractive fundamentals, declining profitability, and shrinking market capitalisation.

Indeed, very much like the traditional television broadcasting and cable companies or traditional publishing and print media companies, the traditional telecom carriers and wireless mobile operators have already entered a period of long-term structural decline. Voice plans and data plans share the same future as bundled cable packages and the daily rag.

Why? Because technology is irreversibly changing consumer preferences, buying habits, behaviours and choice. Innovators will not only benefit from the new economy in telecommunications, but will also likely determine the way that consumers communicate, what devices they use to communicate, who and how they will pay, for both the hardware and connectivity. This future will be divined at the expense of the old economy incumbents.

A telephone carrier and wireless operator (heretofore a "telco"), is neither the creator of the new technologies nor the architect of the new business paradigm. The telco is removed from the "value-added" segments of the business. The telco is not the designer of new high margin hardware. It is neither the developer of content, nor the archivist of complex client data files.

The telco is instead conjoined to the unwieldy and unprofitable, Mcap-intensive, infrastructure assets and their associated upkeep. The telco is like the great railroad operator before everyone figured out, that there was a better way to fly. His expansive networks, like the silver rails that connected San Francisco to New York City, is a giant hungry mule that he must constantly feed. It moves somebody else's goods from point A to point B for a fee, until that somebody finds something faster, cheaper, and cleaner than an ass, to cart the load.

Whatever does he mean by this cantankerous characterization? A telco drives revenues from unambiguous businesses, which are sometimes cryptically titled units such as enterprise, federal, consumer, wholesale, small business, etc. But they are really just four tariff charging segments, and I see it like this:

- Wireless

- Long distance

- Data packet transmission

- Local

Wireless profitability is imperiled by price wars (above) as well as the simple fact that … the consumer no longer needs to pay money to a wireless operator to make a wireless call. Voice-over-IP (VOIP) technology built into iOS, Android, Windows, and BlackBerry smart phone apps by players like Apple, FaceTime, Viber Media (private, Las Vegas Nevada, US-based, Byelorussian outsourced, Israel's) and others, is available for free in 40 languages with global reach. The field will grow.

Long-distance profitability is threatened by Voice-over-IP technologies allowing for free long-distance communications with or without video. Mainstream acceptance was pioneered by Skype (acquired by Microsoft). In addition to Google Hangouts and many others, free long-distance is available on virtually any operating system; Windows, Mac, Linux, Android, iOS, Windows Phone, BlackBerry, Nokia X, Fire OS, Xbox One, PlayStation Vita and PlayStation Portable.

Skype is already approaching 50% of the U.S. long distance call volumes and this is just the beginning. Some say that entrants like Microsoft are just waiting until they have reached critical mass before figuring out how to monetize their Skype base by charging for long-distance calls. Maybe they are, but that is not going to help the telecom carriers - is it?

Data packet transmission revenues are being shorn by social media platforms like WhatsApp and Facebook (FB) Messenger that offer free messaging on far better platforms. And broadband revenues did not get a boost on 26 February, 2015, when the FCC voted to retain net neutrality rules. So, where is the good news?

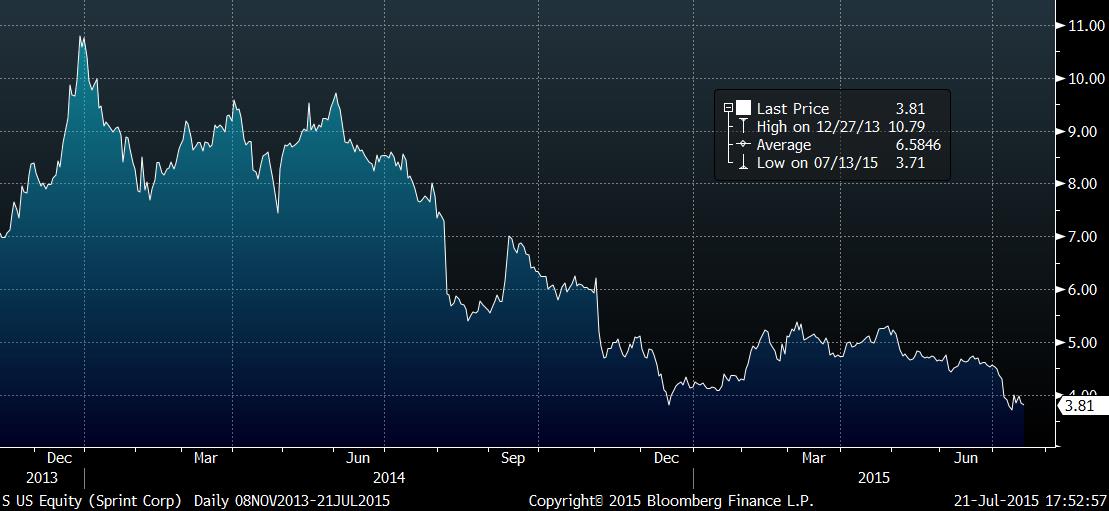

One such mule … Sprint.Sprint (S), America's third-largest wireless network, has dropped -64.65%. Without the backing of Japan's SoftBank (SFTBY)(TYO:9984), the shares might be trading lower.

What do you do when you have nothing left to sell on other than price? Sprint, the third-largest wireless network operator in America with 57.1MM subscribers, announced at year-end 2014 that it would embark on an ill-advised price war. The telco offered half-price wireless services to customers who switched to its service from Verizon and AT&T. The move to gain subscribers burned cash and Deutsche Telekom's (DTEGY) T-Mobile USA joined the fray.

Sprint's $9 billion in cash on 1 Jan., 2015, might be halved as early as mid-2016, just in time for the U.S. government's 2016 auction of wireless spectrum. Wireless carriers burn huge capex on airwaves to meet unending subscriber demands for ever increasing data transmissions. Sprint is anticipated to need +/- $10 billion to participate in the 2016 auction.

Anecdotal unplugged

In addition to broadcast/cable television, I have also been "unplugged" without a home telephone since 2008. I do not use my iPhone to SMS, make or receive calls. The only reason that I bought a SIM card for my mobile in the past many years is because (very specifically here in Singapore) a unique mobile phone number is mandated by the Ministry of Manpower to receive an employment card. And because a unique mobile phone number is also required by the DBS Bank, Singapore, to open an account. So Elizaveta bought an M1 pay-as-you-go SIM for $10 SGD, my number is +65 6643 5362 and I have not made a call or sent an SMS since. Why would I? I can open accounts and forms. It can receive incoming SMS for free.

Another … old fixed-line telephone is expensive. Have you ever watched the telephone poles blur by from the seat of a train? The U.S. Federal Communications Commission (FCC) allocates $4 billion per annum to make sure that every American, no matter how remote, has access to a telephone service, which are subsidised at up to $3,000 per line.

According to a study by the Alliance for Generational Equity, 99.9% of the U.S. households have access to mobile voice service which is non-subsidized. The study takes the position that fixed-line service is no longer a necessary component of America's telecommunications infrastructure, considering VoIP and mobile alternatives.

Ultimately, AGE concludes that "economic welfare would increase if the entire $9 billion per year FCC program were eliminated." "One of the primary benefits of using an IP PBX is that it lacks the cumbersome and expensive physical hardware that has apparently resulted in billions of dollars of waste at the federal level."

Enterprise Specific

Verizon is a nearly $200 billion, large-cap Dow component that is widely held, widely followed and receives considerable research coverage from the investment community. Some might question how a single manager can profit from taking a position in a name. This, when teams of analysts with industry sector-specific expertise have spent years tracking streams of cash flows and developing modeling tools, to perhaps, more accurately predict future earnings. Simply because the number of market participants has no negative impact on the success or failure of the investment.

Conversely, the more stakeholders, the higher the volumes; the larger the market capitalisation and associated ASOs, the lower the friction costs and more efficient the investment. The issue that impacts profit and loss is being on the right side of the trade, and that starts with the macro.

The avoidance of large caps is the same as saying that it is not possible to drive powerful returns from sovereign credit, global Fx, or base commodities, because these large markets are so well covered. But as always the only practical consideration is being right or wrong. A manager does not have to invent a new undiscovered theory that no one else has ever thought about to profit. No, he simply has to be correct in his analysis and the same holds true for stock selection.

But that being said, I suggest that in this particular name and in spite of the broad coverage universe, we are going consider the investment case in a third light. Whereas the "Street" is principally looking at Verizon two ways, we are going to understand this short somewhat differently.

Buyers say:

- Low beta .37 implying lower systematic risk

- The market is broadly constructive on Verizon

- ANR consensus 4 [BUY] rating with only 5% with [SELL] rating (2 of 39 analysts tracked on Bloomberg)

- Giant 4.68% dividend

- Institutions, yield buyers and value buyers (on an earnings basis - 11.92x 2015'E P/E) all love it

- VZ is a core holding in many retail mutual funds and pensions

Sellers say:

- Grossly overvalued (on an asset basis) - the Price/Book is not defensible at 20.78x

- Dangerously overleveraged; the books are laden with massive borrowings, and total debt-to-common equity stands at 921%

- VZ has a combined short-term and long-term debt of $113 billion

Trades as 4% corporate bond with no maturity date. Near $200 billion Mcap, Verizon is trading at $47.59, in the middle of a three-year trading range, within 10% of the 2013 highs.

My take:

- They are both right but that is not what we are focused on in our investment case

Verizon like all the telcos in this unattractive, Mcap heavy space, has had to assume huge debts to build, maintain and improve infrastructure.

Dangerously thin line, able to service $131 billion debt on $127 billion revenues. Razor's edge, able to finance dividend with 90% payout on $9.6 billion in net income with $8.6 billion paid out. It looks like management is bleeding the victim like a vampire, keeping it on the edge of eternal sleep. Or perhaps more like Abramovich ran Sibneft (MCX:SIBN) in the finals days, because he knows that he would be taken out by Gazprom neft (GZPFY). This is a no growth, no future strategy … cash cow management of I suggest, an imperiled core business model.

And the payout looks somewhat like desperation. If you have do not have a growth strategy, why not pay down some of the monster debt? The shares have plateaued in a trading range based on 4% yield for three years, so that makes sense. You are buying a corporate bond with an equity teaser. But what will happen when rates go up as has often been debated here with the same ultimate conclusion? Or just as likely, what happens on a revenue miss? Can't borrow any more money with the 2016 U.S. government auction of wireless spectrum - right?

And voila, the company reported a net loss of 138,000 wireless phone subscribers in the last quarter, 21 April, 2015. These are customers who switched to either T-Mobile or Sprint in the price war. When you are a commodity product, a mule in this case, you have to compete on price.

The U.S. wireless market is positively saturated as we have already discussed. How to drive subscriber growth? >60% of Verizon's growth in 2014 came from tablets, but iPad sales are slowing to a crawl. What next? And that was luck. Verizon's future fleeting growth blips are at the fate of a technology company which invests a new product that might require the services of a mule.

Sprint and T-Mobile believe that value-destructive cash-burning price war (like the one that crippled the U.S. airlines for much of the last 20 years) is the answer. On one hand, firms may desperately try to take from each other's table by slashing price plans. On the other hand, that are being forced to cut roaming (long distance) as the consumer is quickly moving to WiFi? What else can Verizon do to raise sales? As detailed, the company's is a pretty simple business and the answer is not much. What might Verizon do to get those customers back and try to shield top line in order to protect the dividend? Because when the dividend is cut, institutions and retail investors alike will move to the exits.

Disclaimer: Telecom carriers and wireless operators should expect a longer shelf life and more durable profitability in the R.O.W. The current assignment is U.S. centric and like CBS (CBS) in the television broadcasting and cable space, Verizon is a U.S. player with no meaningful global foot print. New technologies and changing consumer preferences in America should directly impact the firm's profitability.

Project Fi

Can it get any worse? Hell yes it can. What about Project Fi? Project Fi, from Google the Friendly Giant may soon shatter any remaining hopes for Verizon and the tech retardant entrenched players.

Project Fi is a mobile phone service that promises unlimited domestic talk and text, unlimited international messaging, tethering and 2G-only international service in over 120 countries for $30 a month. T-Mobile and Sprint combine to provide coverage area and are almost giving away the roaming agreements to Google as price takers not price setters. This represents to me an historical acquiescence similar to the music industry caving in to Apple for $1.00 a tune, just to get on iTunes and find a marketplace, any market place for their music.

Dumb Pipes

I do not see this as a blockbuster for Google, no, rather as an omen of death for the carriers. Why? Because the network switches will be seamless, meaning the customer will not know whether they are using Sprint's or T-Mobile's spectrum. It will move back and forth depending on the signal strength. What that means is a validation of what I have written here, that Google has proven that the carriers are dumb pipes.

Google will now deliver your content on somebody else's fixed investment, and bypass the telco's front office. You don't even need to deal with them anymore. They are telling the investment community that these are commodity-priced mules who haul other people's content across and unprofitable and expensive to maintain, telecommunications infrastructure.

US Peer Comps

The future of telcos … All these guys could go the way of Windstream (WIN), a credible peer comp as recently as 2014, with market capitalization of $527MM.

Other, brain damage

I would like to devote a future report to the subject of cellular radiation and brain damage. There is not further time today, but this remains a long-term risk multiple entrant in the telecom food chain.

Conclusion

The future for telecom carriers, wireless operators and "data mules" is one that might be characterized by deteriorating core business fundamentals, shrinking earnings and falling share prices. This is because innovation giants have permanently changed the way we communicate. Similar to what has been detailed with streaming media and Internet TV, new technologies give the consumer new "choices," which have evolved our behaviours, buying habits and preferences away from the old economy operators.

Long-term industry profitability has been marginalized by commodity pricing, which has ushered in a new era of value destructive, cash burning, price wars. Google's Project Fi is just the latest illustration of the "dumb pipe" conundrum facing the telcos. As long as the telecom carriers and mobile operators fail to innovate, they will be the faceless maintenance workers tasked with oiling, cleaning and upgrading the profitless network (cloud hosting analogy).

Don't let the P/E and the dividend scare you. Verizon is one bad quarter away from a house of cards. Investors are buying a 4% corporate bond with no maturity date, no return of principal and the real possibility of the dividend cut. On an asset basis, the shares are grossly overvalued with a P/B of 21x. The books are dangerously overleveraged, with total debt-to-common equity standing at 921% and $113 billion in debt.

The core business is hemorrhaging mobile subscribers, and there is no credible growth strategy. Management is managing the company by walking tightrope, able to service $131 billion debt on $127 billion revenues. Razor's edge, able to finance dividend with 90% payout on $9.6 billion in net income with $8.6 billion paid out.

Recommended Action

Short Verizon

John Winsell Davies is the Chief Investment Officer of Tano Singapore Advisors Pte Ltd.

This is an original opinion piece which may not reflect the views of the Firm

The opinions expressed here are his own

In some cases Seeking Alpha format does not allow for my charts, graphs, tables and illustrations. As such clarity and impact of original report has been marginalized. Original report available by contacting me

See also Can You Find The Bottom On Starbucks? on seekingalpha.com

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

{kind=link}

{kind=link}

{kind=link}

{kind=link}