Credit: Shutterstock photo

Credit: Shutterstock photoBy Chilton REIT Team :

Remember the good old days when cell phones were displacing home phones as the preferred method for communication? Now, voice is just one of many things that a typical US cell phone can do. According to Cisco, 73% of North American cell phones are considered 'smart' as of December 31, 2015, and companies worldwide are competing to find new ways to use smartphones to enhance our daily lives.

According to AT&T (NYSE: T ), data use on its network has grown 150,000% since 2007. The numbers are staggering, and show no sign of slowing. The 'Big 4' (AT&T, Verizon (NYSE: VZ ), Sprint (NYSE: S ), and T-Mobile (NASDAQ: TMUS )) have fully embraced the video trend and are marketing extensively to those interested in high quality streaming through apps like Facebook (NASDAQ: FB ), YouTube, ESPN, Hulu, Netflix (NASDAQ: NFLX ), and Vevo. The result is billions spent on their networks, putting the boring steel structures that provide the backbone for cellular service squarely in the middle of a race that is sure to continue for decades.

The association with technology and thus Moore's Law has been viewed as a risk to some traditional REIT investors looking at cell tower companies. However, it appears that cell towers are becoming even more valuable as technology advances. We are substantially overweight this sector in our portfolios supported by familiar rationale: irreplaceable assets that produce a durable and growing income stream to investors.

The Tower Business Proposition

In the early days, the wireless carriers owned most of their own tower infrastructure. However, as cell phones became more prevalent and usage began to strain networks, the wireless carriers found themselves with an increasing need to be on more towers to keep up with consumer demand and sustain competitive positioning. While they may have originally viewed a proprietary tower portfolio as an advantage to force other carriers to find and build their own, customers demanded better network quality. The opportunity costs of not being able to meet customer demand, spend more money on obtaining new customers, buy spectrum, or maintain a strong balance sheet became too much to ignore. Thus, they began to systematically sell the towers to aggregators starting in earnest in 2005, as shown in Figure 1 .

When a tower company purchases a tower portfolio from a carrier, it is a perfect example of how an asset is worth more to the buyer than the seller. Because carriers are not keen on leasing their towers to competition, the number of tenants per tower, and thus the profitability of carrier portfolios, is low. In contrast, a tower owner with no ties to a wireless carrier can lease to any and all carriers, thereby doubling or tripling revenues. Especially important to the business model is the extremely high margin of adding an additional tenant, estimated to be 95% or higher by the tower companies. While a tower with one tenant may generate an annual return of 4%, the return can increase to 12% with two tenants, and 20% with three tenants. Historically, the tower companies have been able to increase the average tenants per tower on a portfolio by 0.1 per year. As of December 31, 2015, Crown Castle (NYSE: CCI ) estimates that towers it has owned for over ten years have an average of 2.7 tenants per tower and yield 15%!

Examples of recent transactions show the value that is created at a wireless carrier by deciding to sell a portfolio of towers. In 2015, Verizon sold a portfolio of towers to American Tower (NYSE: AMT ) for $5.1 billion, or $440,000 per tower. Concurrent to selling the towers, VZ agreed to lease the space on those towers for a yield of 4.4% to AMT. Similarly in 2013, Crown Castle purchased a portfolio of towers from AT&T for $4.9 billion , or $540,000 per tower, at a 4.5% initial yield.

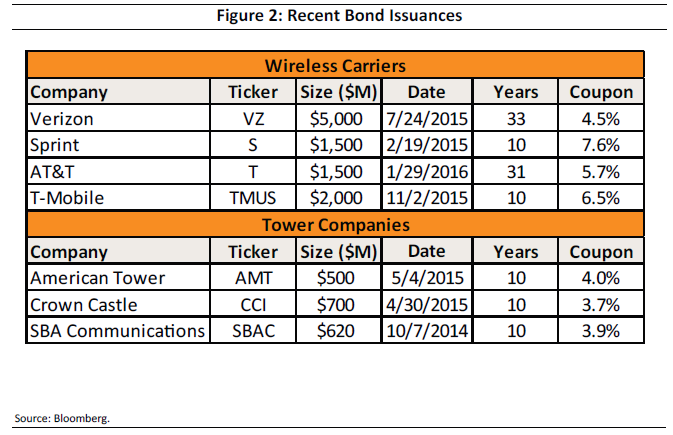

The permanent capital raised in the transactions by both AT&T and Verizon can be compared to their weighted average cost of capital, or WACC. In 2015, VZ raised $5 billion in the bond market with a coupon of 4.5% and a maturity of 33 years, and AT&T raised $1.5 billion at a 5.7% coupon with a maturity of 31 years in 2016. Figure 2 contains the cost of some recent bond issuances for both carriers and tower companies. After factoring in the cost of equity, which is traditionally much higher than debt costs, a sale of towers below a carrier's WACC creates immediate value for a carrier. As shown by the lower issuance coupons, the tower companies can afford to pay these high multiples (low yields) thanks to their low cost of capital and the expected revenue growth from increasing the number of tenants. Therefore, it should be no surprise that 80% of US towers are owned by the three publicly traded tower companies: AMT, CCI, and SBA Communications (NASDAQ: SBAC ).

Data-Dependent Consumers

Another much-promised but often failed thesis that actually works with towers is that supply creates demand. The creation of more capacity and speed for data has always been filled with new uses. So far, we have expanded from voice to emails, text messages, photos, high quality photos, music, video, and HD video. Next up will be 4k video, 10k video, 3D video, and eventually, augmented and virtual reality. Even those who decide they could eschew watching video or listening to music from their smartphone will find a fast wireless connection necessary as more activities and items will be able to be controlled and enhanced by our smartphones - also referred to as the Internet of Things (or IoT). Eventually, it will be called IoE, or Internet of Everything!

The capacity for wireless carriers has been playing a game of catchup for some time. Now that smartphones have so broadly penetrated the US market, the consumers' insatiable appetite for data is being used as a tool by the wireless carriers to take market share. Across all of the 'big 4' carriers, they each are trying to one-up each other with data plans with more data at lower prices, or free streaming from certain sites, or any other gimmick they can think of to get the incremental customer to switch. In short, data consumption will only continue to grow. According to Cisco, mobile data is expected to grow by a compound annual rate of 42% from 2015 to 2020 in the US, the equivalent of increasing by a factor of 6x!

The constraints on what the carriers can offer come in the form of 1) spectrum; 2) coverage, and 3) equipment. A weakness in one of those three can have an effect on the entire network.

Spectrum

Spectrum could be thought of as the 'pipe' through which data travels. Each carrier owns spectrum on which it is deploying its network, but they also must have special equipment that can send and receive data at each end of the pipe. It can take years to deploy sites on a new spectrum level, so each carrier has to buy more spectrum for needs that may be years away. Importantly, each new deployment of spectrum will result in new amendments or leases with the tower owners.

Currently, there is 65 MHz of spectrum from the AWS-3 auction that is owned but not used by the carriers. However, there is also a large amount of spectrum that is owned by companies that do not have a network (mostly DISH Network (NYSE: DISH ) and Ligado Networks, formerly LightSquared (private)). Furthermore, the government owns 600 MHz of remaining broadcast spectrum that it will sell in periodic auctions.

The value of this spectrum continues to climb dramatically, as the most recent auction (AWS-3) in January 2015 raised $41 billion, or more than double what was forecasted. The FCC plans to hold the next auction on March 29, 2016 , which should result in more deployments by the winners that have a network. If DISH decides to sell to or merge with a carrier, the deployment of its spectrum would also be a catalyst for further revenue to tower companies.

Coverage

Coverage is meant to represent the number and capacity of sites, not only in terms of geographic area, but also in fullness of coverage within that area. The reality is akin to a traffic jam where increasing demand coupled with physical constraints like tall buildings or trees can significantly weaken a signal from a tower. While carriers would like to put up an additional site to fix these 'holes' in their network, restrictions on building new towers by cities and municipalities often limit the construction of new towers (the familiar phrase "NIMBY" applies, or Not In My BackYard). In such areas, wireless carriers can use what are broadly known as 'small cells'.

Small cells, typically Distributed Antenna Systems (or DAS), can be thought of as a series of strong WiFi routers that connect to fiber that eventually reaches the same 'backhaul' that the traditional cell sites (also called 'macro cells' or 'macro sites') use. Unlike macro sites, small cells do not have a large radius and therefore must have many nodes to cover the same area or population. DAS can be found in stadiums, office buildings, light poles, rooftops, trees, and where necessary, fake trees, fake gas lamps, or fake light poles.

While the building of new US macro sites is minimal and very few macro cell portfolios are likely to trade (the biggest carrier-owned portfolio belongs to US Cellular ( USM ) wit h 4,000 towers), we are only in the first or second innings for small cell development. Currently, VZ is the only carrier investing significantly in small cell networks. We expect that all of the big 4 carriers will eventually have dense small cell networks as they are able to free up capital.

Crown Castle has been at the forefront of small cell network development, claiming 12% of its revenues in 4Q 2015 came from small cell sites. With its acquisition of Sunesys in 2015, the company now owns 16,000 miles of fiber in the top 25 US cities on which it can deploy small cell networks. The deployment of new small cell networks is generating organic growth much faster than the cell tower business, as shown in Figure 3 . In comparison, AMT derives about 3% of its US revenues, or 2% of total revenues, from small cell sites. AMT and CCI earn 6-8% on its invested capital with one tenant, but annual returns increase to the high-teens with three tenants.

Equipment

The equipment necessary on a tower is dependent upon the number of users in an area, the amount of data used, the technology used (2g, 3g, 4g-LTE, etc.), and spectrum. Each time there has been an upgrade in the technology, there has been a wave of tower portfolio sales by the carriers to raise capital to fund the new network. The addition of equipment to handle the next generation network does not necessitate additional revenue for the tower owner. However, if carriers wish to optimize the new equipment, they must either add new antennas, which results in a lease amendment at a higher rate, or sign a new lease for additional space on the tower. Sometimes, an upgrade does coincide with taking down equipment (i.e. swapping 2g for 4g); however, they almost always put up equipment that is heavier (thus more revenue) due to the enhanced data needs.

Upgrades and densification by all four major carriers offer organic growth potential for the tower REITs. AT&T and Verizon are in the process of deploying Voice over LTE, or VoLTE, which will result in higher quality voice transmissions than the current equipment. Currently, almost all voice transmissions use 2g equipment. Following VoLTE will be the 5g upgrade, though we could be five or more years away from it being a significant driver of lease amendments. AT&T has announced that it will be testing some 5g sites in Austin by the end of 2016 , with plans for it to be 10-100 times as fast as current 4g-LTE speeds!

Tenant Risk

As with anything related to technology, there are obsolescence risks. Better, smaller, lighter equipment, the ability to do more with less spectrum, and the potential for a new technology to displace the need for sites could impair the viability of the tower business. However, the need for data is growing so quickly that most of these upgrades will be necessary just to keep up. There will be instances of non-renewals at sites (called 'churn') when consolidation results in redundant sites or old equipment becomes obsolete (1g for example). Historically, annual churn has averaged 1-2% of revenues.

The lack of a diversified tenant base is a risk should any of the big 4 carriers consolidate or endure financial troubles that could decrease spending on network quality. In comparison, traditional REITs have hundreds or even thousands of tenants where consolidation or bankruptcy of one tenant would have an almost immeasurable effect. We believe the Department of Justice will continue its course after blocking the proposed AT&T and T-Mobile merger. Also, there will be an additional tenant taking space on towers in the next several years called FirstNet. The government is planning to use some of the capital raised in spectrum auctions to create a new network dedicated to public safety. Finally, we believe the risk of a carrier experiencing financial issues is mitigated by the fact that the network is a carrier's most valuable asset so that it will be one of the last expenses to be cut.

Waiting for the REIT Hug

Despite the many attractive qualities of tower companies, not least of which is a recurring revenue stream from non-cancellable long-term leases to various credit tenants with high barriers to entry, the cell tower companies have not yet been fully embraced by REIT investors. Though they are included in a few REIT indexes, CCI and AMT are not in some of the most heavily used REIT benchmarks (SBAC does not plan to convert to a REIT until 2017 or later). The August 31, 2016, creation of the 11th GIC sector for Equity REITs within the S&P, Dow Jones, and MSCI indexes is a potential catalyst for increased interest in the tower REITs by both REIT-dedicated and generalist investors, which could result in significant purchases by ETFs and mutual funds.

The lack of index inclusion has resulted in CCI and AMT trading at a valuation discount to other S&P 500 REITs as of February 29, 2016. The key difference between AMT and CCI is the geographic focus. While CCI is 100% domestic, AMT derives approximately 30% of its revenues from outside of the US. While they carry more economic, geopolitical, and currency risk, international markets have the potential for higher returns given the lower penetration of smartphones. Importantly, cell towers, regardless of who owns them and what is happening with a particular tenant, will continue to be essential for increasing data capacity and speed in a world with an insatiable appetite for data. We believe the tower companies present a predictable growth business model that is no longer able to be ignored by select investors.

See also This Chart Shows The First Big Crash Is Likely Just Ahead on seekingalpha.com

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

{kind=link}