Robert Jankiewicz, Director of Index Product Development at Nasdaq

Rhea Zhou, Senior Analyst of Index Product Development at Nasdaq

As we discussed in our last post, dividend distributions that occur within a taxable account are considered taxable events. Even if an investor receives dividends and chooses to reinvest, the investor still owes taxes today. What if there was a way we could eliminate this friction and improve the overall investor experience? In today’s post, we explore the mechanics of a new strategy that attempts to preserve the benefits of reinvesting dividends without the drag.

It's all about the ex-date

Each time a security, whether a stock or a fund, makes a distribution, the price will adjust downward by roughly the same amount as the dividend (Chart 1).

Chart 1: Ex-dividend Price Response

This is because at the open of a security’s ex-date, new buyers of the security are not entitled to the dividend payment. Thus, the stock price trades without the dividend factored into the current price (i.e. hence the term “ex-div”).

When do securities go “ex-div?”

Not all common stocks pay dividends. However, if an exchange-traded fund (ETF) is holding underlying securities that do pay dividends, the ETF must distribute the income to investors each year. Typically, ETFs will distribute quarterly (for equity ETFs) or monthly (for fixed income ETFs) (Chart 2).

Chart 2: Fixed Income vs. Equity ETF Distributions

However, not all funds will make distributions on the same date; even funds that offer identical investment exposure. For example, Chart 3 shows four S&P 500-tracking ETFs offered by three of the largest ETF issuers.

Chart 3: S&P 500 ETF Risk & Return

Despite the similarities in risk & return, Chart 4 shows that each fund typically makes a distribution on a different date.

Chart 4: S&P 500 ETF Ex-Dividend Calendar

This means that although SPY, VOO, SPLG and IVV each have nearly identical returns for nearly the same level of risk, each fund adjusts for distributions on different dates.

To reinvest or not to reinvest?

If an investor receives a dividend in a taxable account, she can either:

- Keep the distribution and pay taxes

- Reinvest the distribution and still pay taxes (if invested in a taxable account)

If an investor doesn’t need the income today, option #2 may be the best path towards achieving long-run total returns. However, the tax owed on reinvested dividends represents a ‘drag’ on long-term performance (Chart 5). And, as we saw before, the tax drag on fixed income securities is greater than the drag on low dividend-paying equities.

Chart 5: Impact of Taxes

Is there a solution to the drag?

Let’s assume that we want to invest in U.S. aggregate bonds using the iShares Core U.S. Aggregate Bond ETF (AGG). Generally, AGG distributes income once each month. If an investor is indifferent about receiving income, and decides to reinvest, she can attempt to achieve total return, with a tax-related drag due to the distribution (yellow bar in Chart 6).

Chart 6: Total Return vs. Taxed Total Return

Is there a way to potentially replicate total returns (blue bar in chart above) without having to reinvest dividends?

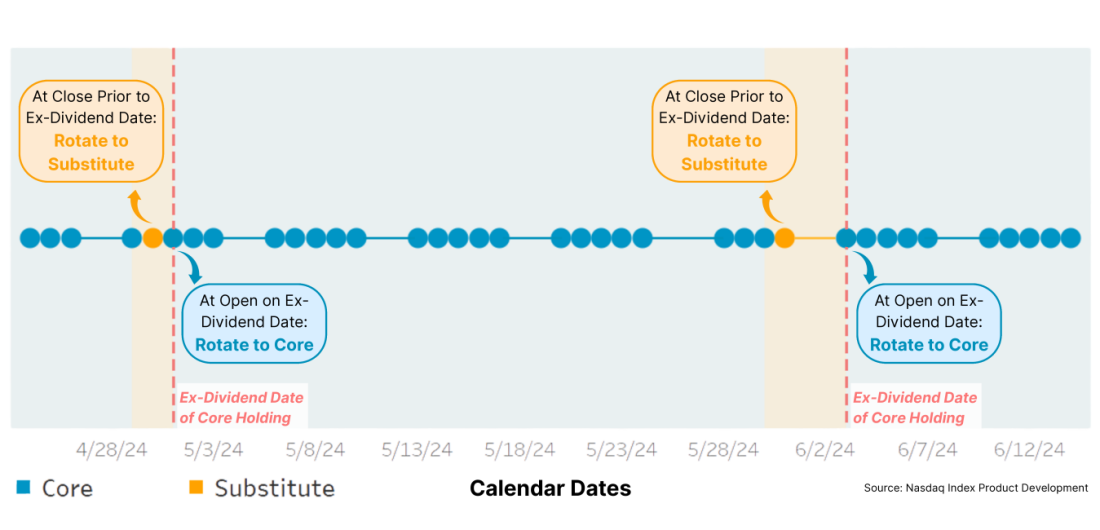

Since we learned above that not all securities go ex-dividend on the same date, one possibility would be to temporarily hold a near-identical AGG substitute on each AGG ex-date (Chart 7). Doing so would avoid receiving the AGG distribution entirely, but the return experience would be as if we had reinvested the dividend.

Chart 7: Example of Rotation

It’s worth noting that an individual would be unable to accomplish this on their own in a personal taxable brokerage account. This is due to potential capital gains taxes and potential violations of wash-sale rules, especially since such a switch could only be executed through a trade transaction. However, using the existing creation/redemption mechanism of the ETF structure, a fund might be able to temporarily rotate into an identical, non-dividend paying, security to maintain a similar risk and return exposure, while avoiding the distribution.

A systematic way to achieve total returns without dividends

Sticking to our U.S. aggregate bond example, to avoid the distribution, one would need to dispose of AGG prior to AGG’s ex-dividend date. However, to maintain exposure to AGG-like returns, the investor would need to temporarily rotate into an AGG-like fund that is not going ex-dividend. Could this be done in a systematic way? The short answer is yes.

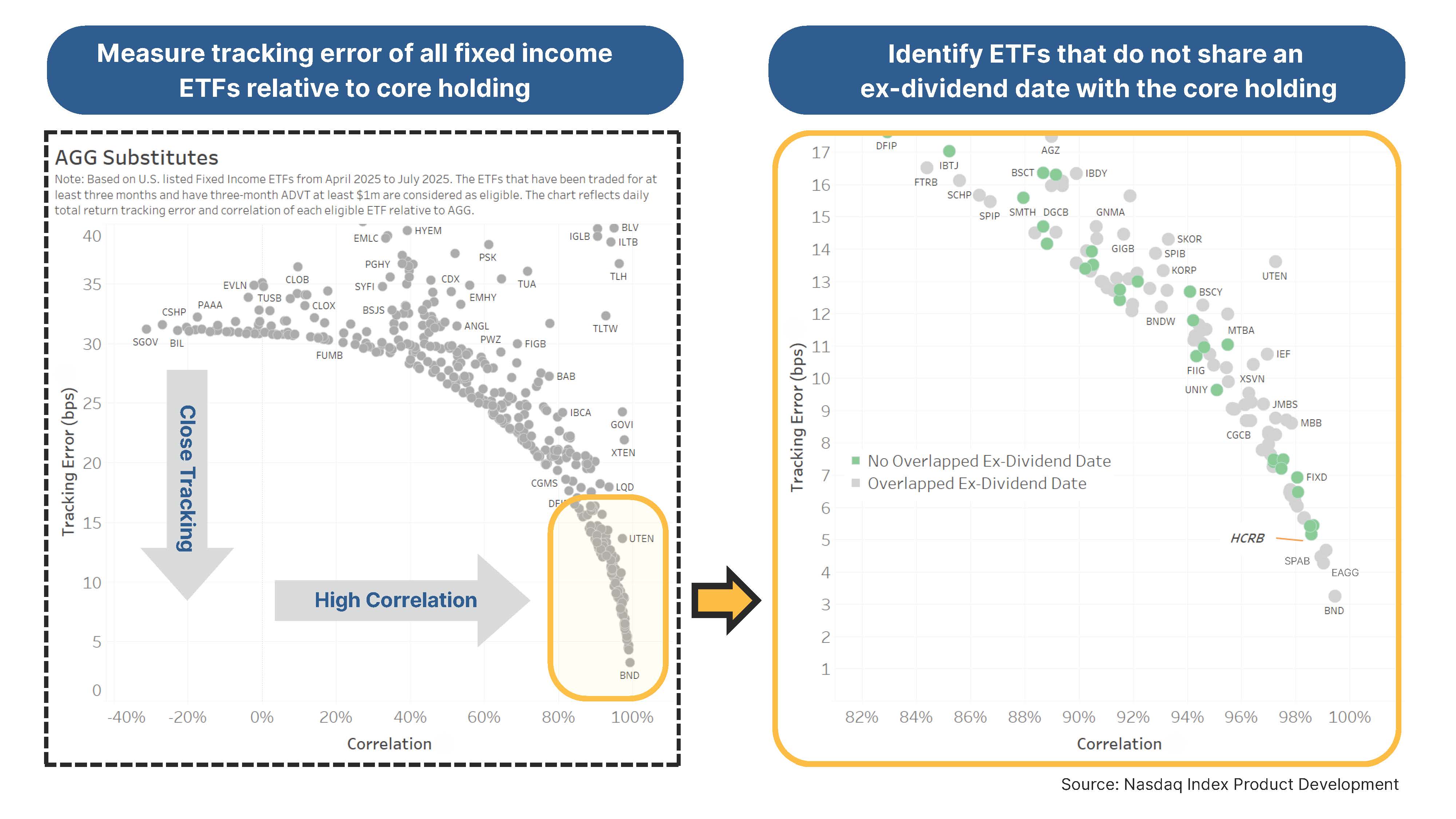

One way to identify a substitute is by measuring tracking error (or deviation of returns). The lower the tracking error, the better the match. Chart 8 below compares the returns of all U.S. listed fixed income ETFs to AGG. On the X-axis, we plot the correlation of returns between each fund and AGG. On the Y-axis we plot the tracking error to AGG.

Chart 8: Selecting a Substitute for AGG

On the right-hand side of Chart 8 we focus on the funds with the lowest tracking error to AGG. Note that we also color each fund by ex-dividend overlap. We see that funds like BND, SPAB, and EAGG would generally represent the best substitutes (based on returns). However, their ex-dates overlap. Thus, we need to move up the curve to find the next best substitute that does not share an ex-date with AGG. In the sample above, this results in HCRB being the best non-overlapping match.

By repeating this process each time AGG goes ex-dividend, we could potentially replicate total returns without having to reinvest dividends.

Chart 9: AGG Price Return without Dividends

In Chart 9, the blue line represents the hypothetical total return (assuming no taxes are paid on reinvested dividends). Assuming an investor must pay taxes on those reinvested distributions, realized performance may look closer to the yellow line in Chart 9 above.

By temporarily rotating into an AGG-like substitute on AGG distribution dates (which are generally the beginning of each month), we could potentially generate a price return (i.e. no dividends reinvested) that is nearly equivalent to total return (with dividends reinvested). Thus, the ~100bps in tax drag from Chart 6, can now be considered ~100bps in tax alpha – a material amount for investors who may not need income today (Chart 10).

Chart 10: Turn Tax Drag into Tax Alpha

A final thought on fees

An important consideration, though, for such a strategy would be potential fees. If the cost exceeds the potential tax savings, there isn’t much improvement to the investor experience. For this reason, higher-yielding assets may be more suitable for this type of strategy, as there will likely be residual savings after fees.

Conclusion

ETFs usually make dividend distributions, which are typically taxable events within taxable accounts. Income-agnostic investors must still pay income taxes on distributions, even if they choose to reinvest their dividends. Finding a way to reduce this friction may help investors meet their long-term financial goals, while improving the investing experience along the way.

Disclaimer:

Information set forth in this communication contains forward-looking statements that involve a number of risks and uncertainties. Nasdaq cautions readers that any forward-looking information is not a guarantee of future performance and that actual results could differ materially from those contained in the forward-looking information. Forward-looking statements can be identified by words such as “will,” “believe” and other words and terms of similar meaning. Forward-looking statements involve a number of risks, uncertainties or other factors beyond Nasdaq’s control. These risks and uncertainties are detailed in Nasdaq’s filings with the U.S. Securities and Exchange Commission, including its annual reports on Form 10-K and quarterly reports on Form 10-Q which are available on Nasdaq’s investor relations website at http://ir.nasdaq.com and the SEC’s website at www.sec.gov. Nasdaq undertakes no obligation to publicly update any forward-looking statement, whether as a result of new information, future events or otherwise.

Nasdaq® is a registered trademark of Nasdaq, Inc. The information contained above is provided for informational and educational purposes only, and nothing contained herein should be construed as investment advice, either on behalf of a particular security or an overall investment strategy. Neither Nasdaq, Inc. nor any of its affiliates makes any recommendation to buy or sell any security or any representation about the financial condition of any company. Statements regarding Nasdaq-listed companies or Nasdaq proprietary indexes are not guarantees of future performance. Actual results may differ materially from those expressed or implied. Past performance is not indicative of future results. Investors should undertake their own due diligence and carefully evaluate companies before investing. ADVICE FROM A SECURITIES PROFESSIONAL IS STRONGLY ADVISED.

© 2025. Nasdaq, Inc. All Rights Reserved.

Latest articles

This data feed is not available at this time.

Data is currently not available