With Black Friday sales setting a new record in the U.S., Dillard’s DDS is a retail stock to consider that currently holds a spot on the coveted Zacks Rank #1 (Strong Buy) list.

As a leading department store chain that focuses on fashion apparel and home furnishings, Dillard’s stock is up over +50% year to date due to stellar earnings that have exceeded analyst expectations and broader optimism tied to Federal Reserve rate cuts.

Although DDS trades at a lofty price tag of over $600 a share, Dillard’s immense profitability and digital presence could lead to even more upside. To that point, Dillard’s operates a full e-commerce site and mobile app while having one of the most efficient brick-and-mortar operations of any retail chain.

Image Source: Zacks Investment Research

Dillard’s Unique Business Model

For those who are wondering, the major reason Dillard’s is exceptionally profitable compared to other department store chains is that it owns most of its stores rather than leasing them. This ownership structure reduces ongoing rent expenses, stabilizes costs, and gives the company valuable assets on the balance sheet. Notably, Dillard’s has been able to buy most of its department stores rather than leasing because it pursued a long-term, debt-averse expansion strategy that emphasized real estate ownership from its very beginnings when founder William T. Dillard opened his first store in 1938.

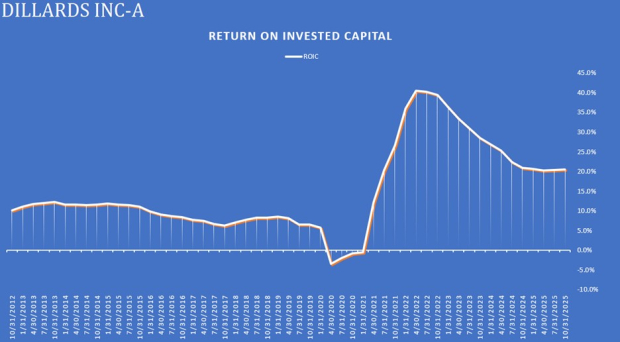

As you can imagine, Dillard’s efficiency metrics are very admirable. This is highlighted by a 20% ROIC, a very high return on invested capital for a department store chain, and above the often preferred range of 10-15%. Additionally, Dillard’s has an excellent free cash flow conversion rate of 108%, with an FCF conversion rate of 80% or higher illustrating a company’s ability to turn its accounting profits into actual cash available for reinvestment, debt repayment, or shareholder returns.

Image Source: Zacks Investment Research

Positive EPS Revisions

Indicating that now may be an ideal time to buy Dillard’s stock is that EPS revisions for its current fiscal 2026 have risen 5% in the last 30 days from estimates of $30.92 to $32.61. While Dillard’s robust bottom line is projected to contract in its next fiscal year, FY27 EPS estimates are up over 6% in the last month from estimates of $28.10 to $29.93.

Image Source: Zacks Investment Research

Dillard’s Modest P/E Valuation

Making the trend of rising EPS revisions more appealing is that Dillard’s stock still trades at a reasonable 20X forward earnings multiple. Despite being one of the most profitable companies in the broader retail sector, DDS is at a slight P/E discount to Kohl’s KSS and is not at a stretched premium to Macy’s M 11X.

Image Source: Zacks Investment Research

Bottom Line

Dillard’s has remained a unicorn among retail stocks and has certainly been a portfolio leader for many investors. Optimistically, this may continue as Black Friday gave more solidification to what is expected to be a record-breaking holiday shopping season, and Dillard’s is likely to capitalize.

Zacks Names #1 Semiconductor Stock

This under-the-radar company specializes in semiconductor products that titans like NVIDIA don't build. It's uniquely positioned to take advantage of the next growth stage of this market. And it's just beginning to enter the spotlight, which is exactly where you want to be.

With strong earnings growth and an expanding customer base, it's positioned to feed the rampant demand for Artificial Intelligence, Machine Learning, and Internet of Things. Global semiconductor manufacturing is projected to explode from $452 billion in 2021 to $971 billion by 2028.

See This Stock Now for Free >>Dillard's, Inc. (DDS) : Free Stock Analysis Report

Macy's, Inc. (M) : Free Stock Analysis Report

Kohl's Corporation (KSS) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.