The Trump administration has never been afraid of rocking the boat, even if that means capsizing historical political norms. Its stance on Ukraine and Russia has been a significant departure from previous US policies, marked by a controversial approach that has drawn both domestic and international criticism, but praise from his loyalists.

It is a notable shift in rhetoric and policy. Unlike his predecessors, President Trump has often refrained from directly blaming Russia for its aggression in Ukraine. Instead, he has suggested that Ukraine bears some responsibility for the conflict, a stance that has raised eyebrows among US allies and lawmakers.

One of the most contentious aspects of Trump's policy has been his reluctance to condemn Russian President Vladimir Putin. Trump has repeatedly expressed a desire to improve relations with Russia, even as Moscow continues its military operations in Ukraine. This approach has led to accusations that Trump is too lenient on Russia and that his policies undermine US support for Ukraine.

His allies take a different stance, citing that isolating Russia, specifically Putin, is like cornering a rabid racoon and that perhaps giving Putin a seat at the table is the best way to calm tensions and reach a more reasonable resolution. On the third anniversary of Russia's full-scale invasion of Ukraine, the US joined Russia, Belarus, and North Korea in voting against a European-drafted resolution condemning Moscow's actions at the United Nations. This vote marked a significant departure from previous US positions, which had consistently supported Ukraine and condemned Russian aggression.

The US also proposed its own resolution calling for a swift end to the conflict, but avoided labeling Russia as the aggressor or acknowledging Ukraine's territorial integrity. This move was seen as an attempt to shift the focus from assigning blame to seeking a resolution, but it was met with widespread criticism from US allies and lawmakers.

This stance will undoubtedly have major implications for the North Atlantic Treaty Organization (NATO) and Europe. By aligning more closely with Russia and distancing itself from traditional allies, the US has created uncertainty about its commitment to NATO and European security. This shift has raised concerns among European leaders, who fear that the US may be preparing to reduce its involvement in NATO or even withdraw from the alliance altogether.

European countries have been urged to increase their defense spending and take greater responsibility for their own security, with a renewed focus on strengthening European defense capabilities and reducing reliance on the US. However, the prospect of a diminished US role in NATO has also heightened fears of Russian aggression and the potential for further destabilization in the region.

Broader Implications of the Russia-Ukraine Conflict

The Russia-Ukraine conflict has far-reaching implications beyond Europe. The war has disrupted global supply chains, particularly in the energy and food sectors, leading to increased prices and economic instability, as well as highlighting the importance of international law and the need for a coordinated global response to aggression.

By taking a more conciliatory stance towards Russia, the US risks undermining the international consensus on the need to hold Russia accountable for its actions, a seemingly non-concern for the Trump cabinet.

Arming the Alliance

The shifting stance of the US and its intention to pressure other members of the Alliance to increase their own spending on defense may be a boon for aerospace and defense firms both at home and abroad. Even prior to the arrival of the Trump administration and its newfangled rhetoric, non-US NATO members have significantly increased their spending on defense. Since Russia’s invasion of Ukraine in early 2022, non-US NATO members have increased annual defense spending to $380 billion and many are expected to meet their 2% GDP target (i.e., spending the equivalent of 2% of their GDP on defense) for the first time since it was set in 2014. Whereas only 10 NATO members met their 2% GDP target in 2023, 23 are expected to meet that target in 2024. According to current estimates, non-US NATO members are expected to have collectively increased their defense expenditure by 17.9% and equipment expenditure by 36.9% in 2024 alone. Separately, defense spending remains politically popular with broad bipartisan support amongst US legislators; annual funding for US defense acquisition, procurement, research, and development is projected to rise to $330 billion by 2038 according to the Congressional Budget Office (CBO).

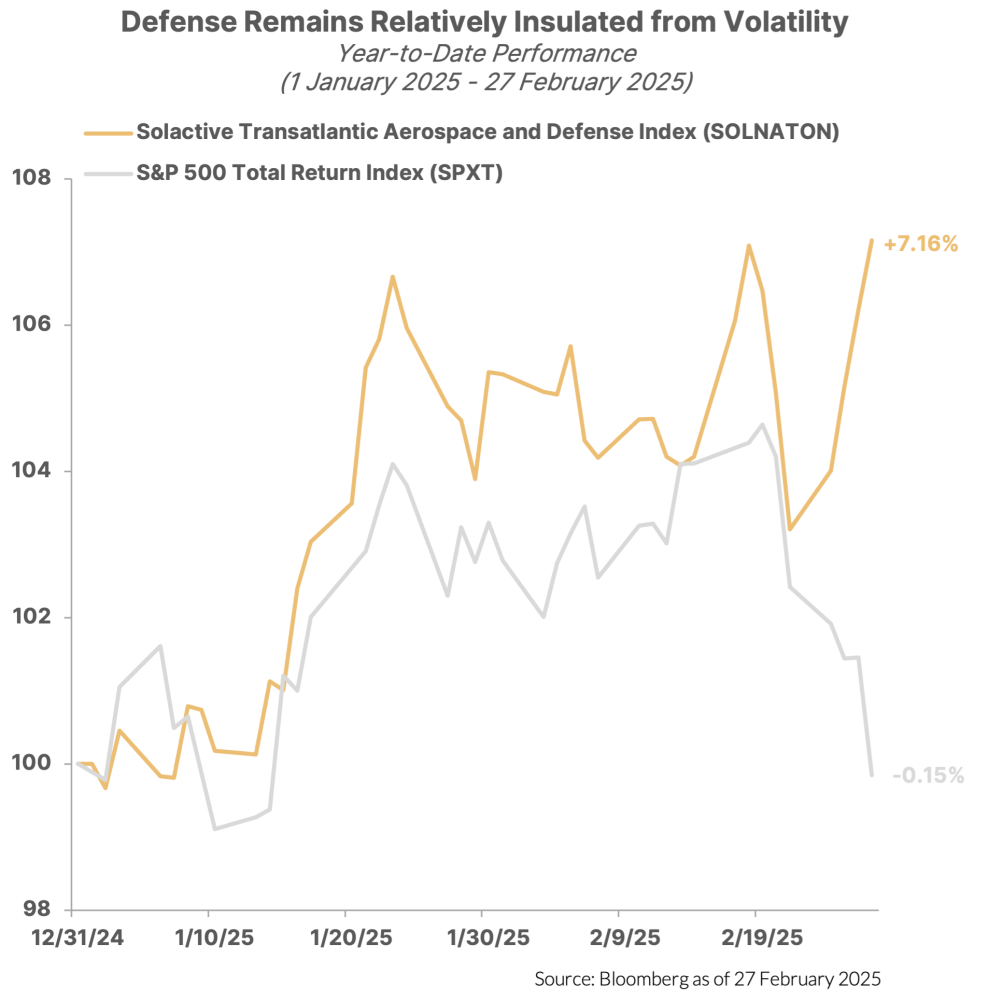

These substantial increases in defense and equipment expenditure have driven significant outperformance in aerospace and defense firms. Since Russia’s invasion of Ukraine in early 2022, the Solactive Transatlantic Aerospace and Defense Index (SOLNATON), which identifies aerospace and defense companies headquartered in NATO member countries, has delivered a total return of +79.96%, outperforming the S&P 500 (+29.09%) by over 50% over the same time period. Year-to-date, the SOLNATON index has also remained relatively insulated from recent volatility, delivering a 7.16% return and outperforming the S&P 500 (-0.15%) which recently turned negative for the year. Given both rising defense spending by non-US NATO members and the continued bipartisan political popularity of defense spending in the US, strategies tracking aerospace and defense companies remain on robust footing.

Investment Themes

Nvidia (NVDA): The ability to call your shot is rarely accomplished, most famously by Babe Ruth in game three of the 1932 World Series, and most recently by Nvidia, which forewarned of “insane” demand for its new Blackwell chips and that gross margins would be squeezed in the first half of 2025. Nvidia blew away revenues, earnings, and guidance. Yet, like they forewarned, gross margins were tighter but still an impressive 73%, which, like Ruth, is rather legendary. Somehow investors were disappointed with all of that “predictability,” and the shares were down after hours. Ruth calling his shot captivated baseball fans for almost a century now, but the stunning performance and ability to forecast with precision somehow left investors with a bad taste in their mouth. Maybe a good night’s sleep will give the market a better appreciation for just how dominant Nvidia has performed in the most important tech revolution to take place since the dawn of the internet and the smartphone. AI is just at the beginning of a multi-year buildout, and the numbers speak for themselves. Nvidia continues to outperform and Blackwell's sales were extraordinary. With no end in sight to continued demand, attempts to find weaknesses in Nvidia’s report is tantamount to a nitpick, at best, and perhaps one day they will speak of Jensen Huang and AI as they do of Ruth and Baseball.

Super Micro (SMCI): The biggest concern for SMCI was that it would not meet the deadline, or that it would submit an incomplete, incoherent filing and be delisted from Nasdaq. And even though SMCI filed in the very last minutes, it satisfied requirements and the company will remain listed on the Nasdaq. As for the spike, the earnings were very strong and likely fueled speculators, who were nervous to get in before, but piled in to ride the momentum. It was an unsurprising development in today’s casino-like markets. There are two ways to look at the "adverse opinion" BDO has of SMCI's internal controls. One is that it is a sign of more issues to come, especially with the SEC and DOJ still investigating the matter with the company. On the other hand, one can be more positive and believe that BDO's oversight and recommendations could fix existing issues making the company more compliant moving forward. It depends on how much confidence you have in SMCI management to address and fix the problems that were discovered. The bulls are seemingly taking a more positive view.

Major US Economic Reports & Federal Reserve System Speakers (Times in EST)

MONDAY, MARCH 3

9:45 am S&P Final US Manufacturing PMI

10:00 am Construction Spending

10:00 am ISM Manufacturing

12:35 pm St. Louis Fed President Musalem Speaks

TUESDAY, MARCH 4

2:20 pm New York Fed President Williams Speaks

TBA Richmond Fed President Barkin Speaks

WEDNESDAY, MARCH 5

8:15 am ADP Employment

9:45 am S&P Final U.S. Services PMI

10:00 am Factory Orders

10:00 am ISM Services

2:00 pm Fed Beige Book

THURSDAY, MARCH 6

8:30 am Initial Jobless Claims

8:30 am US Productivity (Final)

8:30 am US Trade Deficit

10:00 am Wholesale Inventories

3:30 pm Fed Governor Christopher Waller Speaks

7:00 pm Atlanta Fed President Bostic Speaks

FRIDAY, MARCH 7

8:30 am US Jobs Report

8:30 am US Unemployment Rate

8:30 am US Hourly Wages

8:30 am Hourly Wages Year-over-Year

10:15 am Fed Governor Michelle Bowman Speaks

10:45 am New York Fed President Williams Speaks

12:20 pm Fed. Governor Adriana Kugler Speaks

12:30pm Fed Chairman Jerome Powell Speaks

3:00 pm Consumer Credit

Disclosures:

All data sourced from Bloomberg as of 27 February 2025

Views expressed in this newsletter are the current opinion of the author. The author’s opinions are subject to change without notice. Information contained in this report was received from sources believed to be reliable, but accuracy is not guaranteed. Past performance is not indicative of future results. Investing always involves risk and you may incur a profit or loss. No investment strategy can guarantee success.

Themes Management Company LLC serves as an adviser to the Themes ETFs Trust. The funds are distributed by ALPS Distributors, Inc (1290 Broadway, Suite 1000, Denver, Colorado 80203). Themes ETFs are not sponsored, endorsed, issued, sold, or promoted by these entities, nor do these entities make any representations regarding the advisability of investing in the Themes ETFs. Neither ALPS Distributors, Inc, Themes Management Company LLC nor Themes ETFs are affiliated with these entities.

This report is provided for informational purposes only and is not intended to be, and should not be construed as, an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Recipients should not rely upon this information as a substitute for obtaining specific legal or tax advice from their own professional legal or tax advisors. References to specific securities and their issuers are for illustrative purposes only and are not intended and should not be interpreted as recommendations to purchase or sell such securities. Indices and trademarks are the property of their respective owners. Information is subject to change based on the market or other conditions.

Certain information contained herein has been obtained from third party sources and such information has not been independently verified by Themes. No representation, warranty, or undertaking, expressed or implied, is given to the accuracy or completeness of such information by Themes or any other person. While such sources are believed to be reliable, Themes does not assume any responsibility for the accuracy or completeness of such information. Themes does not undertake any obligation to update the information contained herein as of any future date.

Certain information contained herein constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance or a representation as to the future.

Latest articles

This data feed is not available at this time.

Data is currently not available