Restoration Hardware Holdings, Inc (NYSE: RH) is a luxury furniture company predominantly in the United States with international expansion on deck. The company was formerly known as Restoration Hardware and rebranded itself while changing to a subscription model in 2016.

RH CEO Gary Freidman is fond of quoting Bernard Arnault, CEO of Louis Vuitton Moet Hennessy (OTC: LVMUY), that "Luxury goods are the only area it is possible to make luxury margins." This is certainly true of RH and shareholders have enjoyed quite a ride since the rebranding in 2016.

Up until then, the stock was floundering. The company then pivoted from cash-and-carry retail to a subscription-based model. Customers are able to view furniture in luxurious galleries and then order through the company's catalogue today. When management announced the change it was not well received. However, an investment of $10,000 the day after the announcement in February of 2016 would be worth over $159,000 today. With demand strong, international expansion coming, and positive results there are still gains to be made for long-term investors.

Source: Getty Images.

Little competition as management looks to expand

RH does not have a major competitor in the luxury furniture space. Wayfair (NYSE: W) is more focused on volume and definitely does not produce luxury margins. Williams-Sonoma (NYSE: WSM) produces generous margins but does not have the same luxury status as RH. Instead Williams-Sonoma's website pitches Black Friday half-off sales and the other deals of a mainstream retailer. RH is less about mass appeal and typically does not market this way.. This isn't to say that either approach is wrong, simply that the two companies are after separate audiences and therefore are not direct competitors. RH caters to those who spend 10% of their house's value on furnishing it after purchase. This is why the company says they exist "in the 10%." The RH target customer spends upwards of $1 million on their primary home. No other retailer caters to this market which gives RH tremendous pricing power.

The lack of competition is also true internationally, and RH is looking to expand. Plans to expand to Europe were put off by the COVID-19 pandemic. Management wisely recognized that it would be better to push the gallery opening back than to try to debut during a worldwide health crisis. Locations in the United Kingdom and France are slated to open in 2022.

Our global expansion begins in the spring of 2022 with the opening of RH England, The Gallery at Aynhoe Park, a 73 acre historic estate designed in 1615 by Sir John Soane, arguably one of the most respected and celebrated architects of his time. RH England will feature The Aynhoe Architectural Library, The Aynhoe Organic Gardens, The RH Restaurant & Orangery, and The RH Champagne & Caviar Cellar among other unique experiences.

Pending reopening plans for France, our goal is to open RH Paris, The Gallery on the Champs-Elysees in the fall of 2022.

-Gary Freidman, CEO on the Q1 FY21 earnings call.

The company believes the international market will be a massive opportunity of more than $20 billion in revenue once scaled. For reference, RH has produced top-line revenue of $3.5 billion over the prior 12 months.

Revenue is growing while margins expand

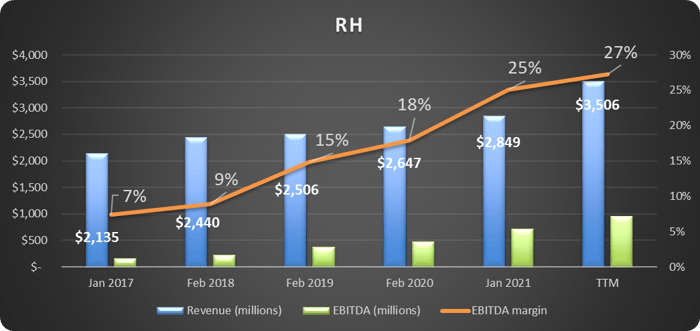

RH produced just $157 million in earnings before interest, taxes, depreciation, and amortization (EBITDA) in the first year after the 2016 reimagining. Over the last twelve months this figure is over $950 million. Shown below, revenue, EBITDA, and EBITDA margin are all growing significantly and in tandem.

Source: RH.

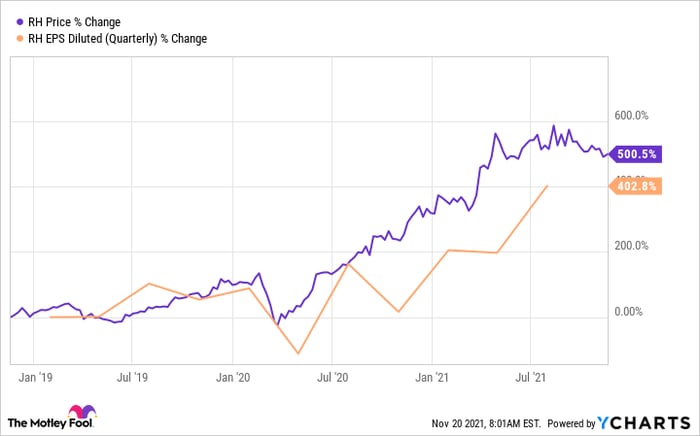

RH still trades in a reasonable range despite the massive increase in share price due to the equally massive increase in earnings. Over the past three years, the stock has gained over 500% -- however EPS has nearly kept pace by gaining over 400% over this period, as shown below.

Image source: YCHARTS

The stock currently trades with a PE of 37, however this drops to just 25 on a forward basis. Should management continue to execute and successfully expand internationally this stock could easily outpace the market moving forward.

Supply chain challenges remain

RH is facing supply chain issues like many manufacturers and retailers. A lot of RH furniture is made in Vietnam where manufacturing was shuttered for a period due to COVID-19 . The company also delayed catalogue releases in 2020 and 2021 due to supply chain woes. Now the entire United States is dealing with ports which are backlogged.

While these are challenges, it is much better to have supply issues than demand issues. The strong demand is illustrated by the increase in deferred revenue and customer deposits which rose from $281 million at January 31, 2021 to $397 million at July 31, 2021.

The Verdict

RH has handsomely rewarded shareholders since bravely altering its business model in 2016. Revenues, operating income, EBITDA, and margins are all increasing with each subsequent period. Still, the valuation remains reasonable. International expansion offers a massive opportunity for growth if done correctly, and management has a history of success. Short-term supply chain bottlenecks will cause headaches, however the long-term demand trends are extremely positive. RH stock should be a strong consideration for investors looking for a high margin and growing company with strong demand trends and expansion opportunities. .

10 stocks we like better than RH

When our award-winning analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

They just revealed what they believe are the ten best stocks for investors to buy right now... and RH wasn't one of them! That's right -- they think these 10 stocks are even better buys.

*Stock Advisor returns as of November 10, 2021

Fool contributor Bradley Guichard owns shares of RH. The Motley Fool recommends RH. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.