As the initial rush surrounding chatbots powered by artificial intelligence (AI) wears off, investors are finally starting to come to their senses that Microsoft's Bing chatbot isn't the end of Google search. Alphabet (NASDAQ: GOOGL) (NASDAQ: GOOG) didn't want to rush the launch of this technology, which is smart, because Microsoft's chatbot has been giving users some disturbing answers.

While many investors want to focus on AI, there is one area that could be even more important for Alphabet: cloud computing. This segment carries immense opportunity for Alphabet and could hold the keys for its next growth phase.

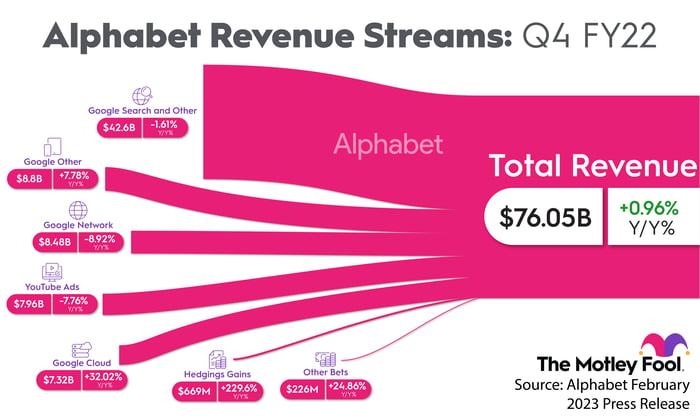

Google Cloud doesn't make up a massive amount of Alphabet's revenue yet

If you look at the infographic below, search still makes up much of Alphabet's revenue.

Image source: The Motley Fool.

However, of its major segments, none is growing faster than Google Cloud. Despite being in third place among the major cloud providers, Google Cloud outpaced its primary competitors in Q4, growing faster than Amazon Web Services (AWS) (20%) and Microsoft Azure (31%).

While growing when you're smaller is easier, it's still impressive to outpace the competition. But the growth isn't done, as cloud computing is a massive market opportunity.

Precedence Research predicts the global cloud computing market could reach $1.6 trillion by 2030. In Q3, Synergy Research Group estimated Google Cloud held about an 11% market share. So if Alphabet can maintain its current position by 2030, it could be pulling $176 billion in annual sales from Google Cloud.

That's an aggressive projection, but it wouldn't be surprising with how vital cloud computing is becoming in daily business functions.

A lot of earnings will also be made from this revenue stream.

When Google Cloud turns profitable, it will have a significant boost on Alphabet's finances

Google Cloud isn't profitable, but it is trending in the right direction.

| Quarter | Google Cloud Operating Margin |

|---|---|

| Q1 2022 | (16%) |

| Q2 2022 | (13.7%) |

| Q3 2022 | (10.2%) |

| Q4 2022 | (6.3%) |

Data source: Alphabet.

Although we don't know what the final operating margin for Google Cloud will look like in 2030, we can use AWS's Q4 operating margin of 24% as a baseline. With $176 billion in projected revenue by 2030, Alphabet would generate $42.2 billion in operating income from Google Cloud. After taxing this amount at Alphabet's 16% trailing-12-month average tax rate, you'd get $35.5 billion in net income.

For reference, Alphabet generated $60 billion in net income in 2022 from its current operations, but this number would rise to $63 billion if the operating losses for Google Cloud were subtracted. So in eight years, Google Cloud has the potential to grow Alphabet's earnings by 59%, solely based on Google Cloud's trajectory.

That's a loose growth model for Google Cloud, but it displays how big a part it will be for Alphabet in the coming decade.

While Alphabet can't lose the AI battle (the majority of its revenue still comes from search), cloud computing is another area investors should be looking at. With Alphabet trading at 20 times earnings, I think it is an excellent time to establish a position in the stock.

10 stocks we like better than Alphabet

When our award-winning analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

They just revealed what they believe are the ten best stocks for investors to buy right now... and Alphabet wasn't one of them! That's right -- they think these 10 stocks are even better buys.

*Stock Advisor returns as of February 8, 2023

Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. John Mackey, former CEO of Whole Foods Market, an Amazon subsidiary, is a member of The Motley Fool’s board of directors. Keithen Drury has positions in Alphabet and Amazon.com. The Motley Fool has positions in and recommends Alphabet, Amazon.com, and Microsoft. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.