Buying high growth, flashy companies might be exciting, but it can also be problematic if they don't execute on their vision flawlessly. Snowflake (NYSE: SNOW) is nearing that point, as its revenue growth has deaccelerated enough that its stock might not be worth the price tag.

However, a better pick could be Adobe (NASDAQ: ADBE), long heralded as one of the most consistent software stocks. So is Adobe a better choice than Snowflake? Let's look at the businesses and find out.

Slightly different business models

Snowflake and Adobe software caters to completely different audiences. Snowflake's software is meant for companies trying to manage data flows better. Because you can store, process, and feed data into various applications using Snowflake, it has a broad reach for nearly every data-driven company.

Adobe's products are used as tools for more-creative and art-focused careers. Many of Adobe's products are the industry standard in graphic design. They are taught to students at the high school level and up, giving the software an impressive foothold with future generations.

The only thing that links Snowflake and Adobe is that their products are delivered the same way as a software package. But how they charge for them is slightly different.

With Adobe, customers are charged a monthly fee per license that can include just one product or a bundle. This provides a significant advantage during a difficult economy, when many businesses are forced to continue paying Adobe for their product. Otherwise, their employees wouldn't be able to produce anything of value.

Snowflake uses the consumption model. Clients only pay for Snowflake's services as they are used, so if a customer only needs to run a query every quarter, it isn't paying nearly as much as a monthly subscription.

This aligns the company's interests with the customers' because it must produce an excellent product that makes its users want to deploy it continuously. But clients could pull back their usage and hurt Snowflake if times get tough and it isn't an everyday essential.

Snowflake probably has the edge in good times, but in tough times, Adobe takes the cake. This adds to Adobe's consistency: It might not have the booming business of Snowflake, but it isn't subject to the downside risks, either.

While this is a subtle advantage, do the financials back it up?

Adobe stock is much cheaper than Snowflake

Directly comparing Adobe's and Snowflake's growth rates might lead to false conclusions, since Snowflake is young and still capturing its initial market. But what we can do is see if their growth rates warrant the valuations of the stocks.

In the fourth quarter of fiscal 2023 (ended Jan. 31), Snowflake's product revenue rose 54% to $555 million. But the company posted a net-loss margin of 35%. Snowflake has a long way to go before producing meaningful profits; Adobe is already there.

The first quarter of fiscal 2023 (ended March 3) was quite strong for Adobe, as revenue grew 9% to $4.66 billion. While this isn't close to Snowflake's growth rate, it's hard to match that when your revenue levels are already that high. So even though Adobe's earnings per share (EPS) only rose 1.5% to $2.72, it shows its superior profitability with a 27% margin.

Now to valuation. With Snowflake's high price-to-sales (P/S) ratio of 21, it must substantially grow to become reasonably valued. In its 2022 investor day, Snowflake displayed its long-term operating model, which included adjusted operating income of 20% by fiscal 2029.

Adjusted operating income doesn't include stock-based compensation or taxes, but if you apply a 20% tax rate to that figure, you will get a profit margin of 16%. Dividing its P/S by that profit margin yields its hypothetical price-to-earnings (P/E) ratio, which would be an expensive 131 times earnings.

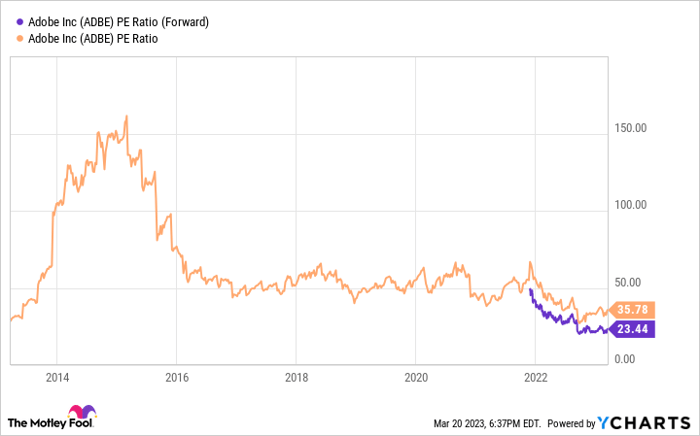

Snowflake is almost too expensive compared to Adobe, which trades at a historically low P/E.

ADBE PE ratio (forward) data by YCharts.

Investors shouldn't take a bargain buy like Adobe for granted, especially with its long-term track record. Snowflake has a huge growth runway, but the expectations are pretty high. On the other hand, Adobe is executing well, and the stock is cheap.

So even though Snowflake is growing much faster than Adobe, I won't be surprised if it outperforms Snowflake (and the market) over the next three to five years, making it a strong buy.

10 stocks we like better than Adobe

When our award-winning analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

They just revealed what they believe are the ten best stocks for investors to buy right now… and Adobe wasn't one of them! That's right -- they think these 10 stocks are even better buys.

*Stock Advisor returns as of March 8, 2023

Keithen Drury has positions in Adobe and Snowflake. The Motley Fool has positions in and recommends Adobe and Snowflake. The Motley Fool recommends the following options: long January 2024 $420 calls on Adobe and short January 2024 $430 calls on Adobe. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.