Test Driving the Access Fee Pilot

Now that the Access fee pilot is in the Federal Register, we thought it would be a good time to get data driven and analyze its potential impact.

The SEC won’t publish the actual baskets until one month before the pilot starts (well into the six-month long “pre-pilot” period). However, they did explain how they will sample stocks. So using their rules, we took the pilot for a test drive, creating baskets to see how the pilot might really look. What we see is pretty amazing.

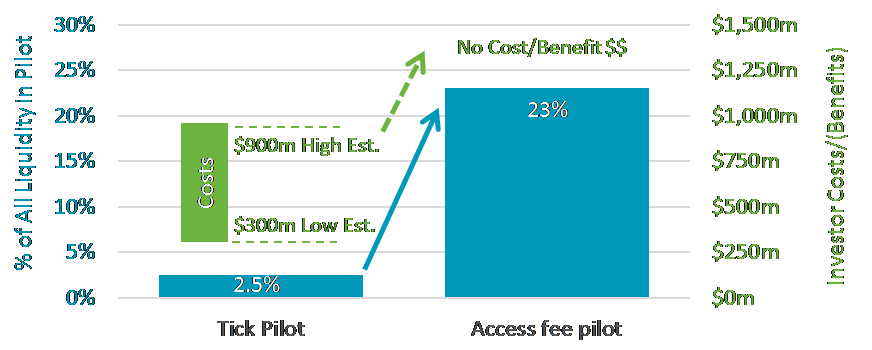

Access fee pilot impacts almost 10 times more liquidity than the tick pilot

To the SEC’s credit, in the final rule the pilot was halved in size. However it still includes around 1,500 stocks (including Canadian cross listings) vs the tick pilot’s 1,200, and five times larger than the 300 stocks that EMSAC proposed.

In contrast to the tick pilot, it includes liquid, large-cap, stocks. Consequently we estimate it will impact 23% of all liquidity, almost 10 times what the tick pilot affected (see chart 1).

Chart 1: The Access fee pilot will likely impact 10 times more liquidity than the tick pilot

One in four chance of inclusion for popular stocks

Looking at our “possible” pilot baskets on a ticker-by-ticker basis is even more revealing.

The pilot excludes stocks with less than 30,000 shares ADV and prices under $2 per share. That leads to the exclusion of around 34% of NMS stocks (grey zone in chart 2). However as those are, by definition, “thinly traded” stocks, most investors will hardly notice.

That also means remaining stocks have around a 25% chance of being in the pilot, and a one-in-eight chance of being in the zero rebate bucket. As these are by definition more liquid, “popular” stocks, pilot group stocks represent 23% of all liquidity. That’s around 1.6 billion shares per day.

Chart 2: Most popular stocks have a high probability of being in the pilot

Note: Basket allocations are estimates only, but are based on the rules, so should be representative

Looking across listing venues is interesting. NYSE listings are the most impacted exchange (thanks to NYSE’s smaller universe of emerging growth stocks) while Cboe listings are the least affected (thanks to Cboe’s concentration and mix of thinly-traded ETF listings).

Over 1 billion shares-per-day see a material change to NBBO economics

The pilot buckets use stratified sampling to select an equal quantity of names across three categories: liquidity, market cap, and stock price. However that doesn’t make the economic impact equal, as liquidity is still concentrated in the larger, more liquid stocks.

Why is that important?

As we recently highlighted, larger more liquid stocks are also the ones most likely trading around a one-cent spread. In fact we estimate that around 1.15 billion shares/day, or 71% of all liquidity in the pilot are stocks with a less than a two-cent spread. Those are also the stocks that are currently the cheapest spreads to trade.

Stocks with a one-cent spread will see their NBBO economics change the most dramatically. In theory, a two-sided market maker can capture 60mils on a round-trip trade (2 x 30 mils), that’s a 60% boost to its economics on a one-cent spread. In reality, that incentive is mostly used to offset adverse selection from larger directional trades, which are typically institutional. Reducing the incentives in these stocks will likely make liquidity providers more concerned about adverse selection. That, in turn, is widely expected to increase the cost of liquidity for takers. How much is a question for another day.

ETFs see stock and basket impact

One of the more controversial decisions of the SEC was to include ETFs in the pilot, and not group them by underlying exposure. This has the potential to significantly affect the competitiveness and spreads of competing tickers. For example in our mock-baskets, IVV is in the “no rebate” bucket, while other S&P 500 ETFs, SPY and VOO, are in the control. Although these tickers could easily be flipped, it’s highly unlikely that they will all be in the same group (technically a 0.2% chance).

Interestingly, more ETFs are thinly traded than stocks. In fact, we estimate about 50% of all ETFsare in the “grey zone” in the chart. However that might impact investors less than expected, as these tickers often have wide spreads already due to market makers pricing in other economic costs (as we detailed in our ETF rule comment letter).

Of course, if far-touch liquidity falls, hedging costs for ETF market makers will also increase. That will make it more expensive to hedge large trades, making RFQ pricing more expensive. This may even affect how closely lit ETF prices track NAV—something many investors take for granted today.

Lessons from the Tick Pilot?

Although many think there are no lessons to be learned from the tick pilot, Greenwich itself said one of the top four lessons was that a cost benefit should have been performed. The tick pilot cost investors more than $300 million on just 2.5% of market liquidity—this pilot affects almost 10-times as much liquidity.

Greenwich also noted that the design of the tick pilot was flawed. The Access Fee Pilot is designed to reduce broker routing conflicts. However it ignores all the other incentives and opportunity costs the buy-side faces. Something a recent FINRA study proved can be calculated without the expense of a pilot.

But most importantly, we are concerned about the market quality for new companies. Corporates were excluded from EMSAC, who originally proposed the pilot, and their comments were mostly ignored in the pilot design. If thinly traded stocks spreads widen, and the cost of liquidity increases, the biggest cost might turn out to be less IPO’s in the U.S. That will be bad for everyone.

Go here to sign up for Phil's newsletter to get his latest insights on the markets and the economy.

More from Economic Research

Three Charts that dispel the Price Improvement Myth

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

Other Topics

Economy Stocks US Markets

Phil Mackintosh

Nasdaq

Phil Mackintosh is Chief Economist and a Senior Vice President at Nasdaq. His team is responsible for a variety of projects and initiatives in the U.S. and Europe to improve market structure, encourage capital formation and enhance trading efficiency.

Read Phil's Bio