Target Corporation TGT announced aggressive actions to optimize its inventory for the rest of fiscal 2022 in response to the tough operating environment, thanks to soaring inflation and changing consumer behavior. The actions include additional markdowns, removing excess inventory and canceling orders. Some other notable efforts are the addition of incremental holding capacity near ports to enable supply-chain flexibility, pricing actions in a bid to mitigate high transportation and fuel costs, and working with suppliers to shorten travel time in the supply-chain process.

We note that inventory rose 43% year over year in the last reported quarter. Target ended up carrying high inventory in several categories, wherein the slowdown in sales was more pronounced than expected. Also, the first-quarter fiscal 2022 operating margin contracted 450 basis points to 5.3%.

The company is also undertaking cost-control measures, such as working with vendors to offset inflationary pressures and driving continued operating efficiencies. It is on track to add five distribution centers in the next two fiscal years to enhance its supply-chain situation.

TGT remains focused on maintaining strength in frequency categories like Food & Beverage, Household Essentials, and Beauty. The company plans to sell fewer products in its home categories as customers have reduced discretionary spending due to the ongoing inflation.

Actions to clear excess inventory, be it deep discounts or cancellation of orders, are likely to weigh on margins. As a result, management envisions a second-quarter operating margin rate of 2%, down from the aforementioned 5.3%.

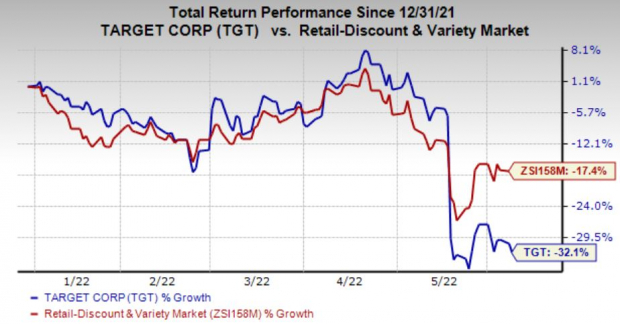

We note that shares of this company have plunged 32.1% year to date compared with the industry’s decline of 17.4%.

Image Source: Zacks Investment Research

However, this Zacks Rank #3 (Hold) stock expects to get back on track in the second half of fiscal 2022 and beyond. Notably, TGT predicts an operating margin rate of 6% for the second half of fiscal 2022. Also, the company continues to anticipate low to mid-single-digit revenue growth for fiscal 2022.

Target has been undertaking several strategic endeavors — be it new stores, owned brand innovations, national brand partnerships, or expansion of same-day services and rollout of sortation centers — to drive engagement, traffic and market share gains.

These have been contributing to the company’s sales performance, as evident from first-quarter fiscal 2022 results, wherein the top line beat the Zacks Consensus Estimate and grew year over year. Comparable sales increased for the 20th successive quarter, gaining from growth in both store and digital channels. Target registered a sturdy performance in Food & Beverage, Essentials and Beauty categories.

Stocks to Consider

Here are three better-ranked stocks to consider — Boot Barn Holdings BOOT, Dillard’s DDS and Kroger KR.

Dillard’s operates as a departmental store chain, featuring fashion apparel and home furnishings. It presently sports a Zacks Rank #1 (Strong Buy). DDS has a trailing four-quarter earnings surprise of 224.1%, on average. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Dillard’s current financial-year sales suggests growth of 6.1%, while the same for EPS indicates a decline of 33.9% from the year-ago period’s reported numbers. DDS has an expected EPS growth rate of 12.6% for three-five years.

Boot Barn, which provides western and work-related footwear, apparel and accessories, currently has a Zacks Rank #2. The company has a trailing four-quarter earnings surprise of 25.2%, on average.

The Zacks Consensus Estimate for Boot Barn’s current financial-year sales and EPS suggests growth of 17% and 4.4%, respectively, from the year-ago period’s reported figures. BOOT has an expected EPS growth rate of 20% for three-five years.

Kroger, which provides an array of goods ranging from household essentials, groceries and electronics to toys and apparel for men, women and kids, currently carries a Zacks Rank #2. KR has a trailing four-quarter earnings surprise of 22.1%, on average.

The Zacks Consensus Estimate for Kroger’s current financial-year sales and EPS suggests growth of 3.2% and 4.1%, respectively, from the year-ago period’s reported figures. KR has an expected EPS growth rate of 9.9% for three-five years.

Zacks' Top Picks to Cash in on Electric Vehicles

Big money has already been made in the Electric Vehicle (EV) industry. But, the EV revolution has not hit full throttle yet. There is a lot of money to be made as the next push for future technologies ramps up. Zacks’ Special Report reveals 5 picks investors

See 5 EV Stocks With Extreme Upside Potential >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Target Corporation (TGT): Free Stock Analysis Report

Dillard's, Inc. (DDS): Free Stock Analysis Report

The Kroger Co. (KR): Free Stock Analysis Report

Boot Barn Holdings, Inc. (BOOT): Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.