Sysco Corporation SYY appears poised, on the back of its Recipe for Growth as well as focus on business transformation. Moreover, gains from prudent buyouts have been aiding the company. That being said, hurdles associated with the pandemic, especially in the International segment, are a concern. Also, the company has been encountering product cost inflation in the U.S. Foodservice segment for a while now. In the third quarter of fiscal 2021, U.S. Broadline saw a 3.5% product cost inflation, mainly due to meat and poultry categories, as well as paper and disposables. Let’s delve deeper.

Recipe for Growth Bodes Well

Sysco at its recent Investor Day unveiled efforts to transform into a more growth-oriented, customer-focused and innovative company. To this end, it spoke about its Recipe for Growth initiative, which involves five strategic priorities aimed at enabling the company to grow 1.5 times faster than the market by FY24-end. The five strategic pillars include enhancing customers’ experience via digital tools. Further, the company is focused on improving the supply chain to cater to customers efficiently and consistently, on the back of better delivery and omnichannel inventory management. Next, Sysco aims at providing customer-oriented merchandising and marketing solutions to augment sales. The company also targets having team-based selling, with an emphasis on important cuisines. Finally, Sysco is focused on cultivating new capacities, channels and segments, alongside sponsoring investments via cost-saving initiatives.

Incidentally, Sysco offered financial guidance for the coming years, as part of which it targets cost curtailments of $750 million for the period FY21 to FY24. For FY22, the company envisions earnings per share of $3.23-$3.43. For FY24, management expects adjusted EPS to be more than 30% higher than the bottom line in FY19. Sysco also anticipates a net leverage goal of 2.5x-2.75x adjusted EBITDA, to be backed by plans to lower debt by at least another $1.5 billion in FY21 and FY22. Additionally, it unveiled a share buyback plan of $5 billion, which will be available till it is fully used. Apart from these, Sysco is on track to exceed its target of achieving cost savings of $350 million in fiscal 2021.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Other Drivers

Sysco has been on track with its business transformation as it navigates through the pandemic. The company has been dedicated to supporting restaurants and preparing for the rebound in foodservice demand. To this end, the company’s Restaurants Rising program is worth noting. Also, waiving off delivery minimums on regularly scheduled delivery days is a factor. Apart from helping customers, Sysco is focused on investing in its people. Moreover, the company is making technological investments to enhance customers’ experience. This includes Sysco Shop technology, the company’s new pricing software, and enhancements to supply-chain systems. Certainly, Sysco has been making solid investments to prepare for business recovery and these investments are likely to continue in the fourth quarter.

Additionally, the company has been carrying out various acquisitions over the years to grow its distribution network and customer base and boost long-term growth. To this end, the company, on May 20, unveiled that it has entered a deal to buy Greco and Sons from Arbor Investments and the Greco family. Markedly, Greco and Sons is a leading independent Italian specialty distributor, which will operate as a standalone unit within Sysco, once the acquisition deal is closed. Certainly, the inclusion of Greco and Sons is likely to help Sysco better cater to Italian-focused customers. We note that this acquisition goes in tandem with its Recipe for Growth initiative. In earlier developments, Sysco acquired J. Kings Food Service Professionals in August 2019. Prior to this, the company took over sister firms J & M Wholesale Meats and Imperio Foods in April 2019.

Main Downsides

Sysco has been bearing the brunt of coronavirus-led softness in food-away-from-home demand. This continued in the third quarter of fiscal 2021 as well, wherein the top and bottom lines declined year over year and the former missed the Zacks Consensus Estimate. Sales declined in both the U.S. Foodservice and International Foodservice segments. Nevertheless, trends improved in the United States toward the end of the third quarter, thanks to lower curbs and the return to normal activities.

International segment sales plunged 31.3% to $1,723.1 million in the third quarter. Stern lockdowns in Europe, Latin America and Canada affected performance in the segment. Sluggish progress related to vaccination was also a factor. On its lastearnings call Sysco stated that the restrictions in Europe were tougher than the ones witnessed in the United States in April 2020. Consequently, sales in Europe have been down considerably from 2019 levels. Apart from these, the company’s business related to travel, hospitality and foodservice management sectors was down in the third quarter. Management expects the sluggish international recovery to continue affecting its fourth-quarter performance and the early quarters of fiscal 2022 (depending on the vaccination status of different countries).

Wrapping Up

Although the company’s sales declined 13.7% year over year in the third quarter of fiscal 2021, it reflected sequential improvement as the second quarter saw a decline of 23%. The independent restaurant space has been doing well and the company expects to see continued gains as the re-opening phase progresses. Management particularly expects such upsides to continue in the largest parts of its portfolio during the fourth quarter.

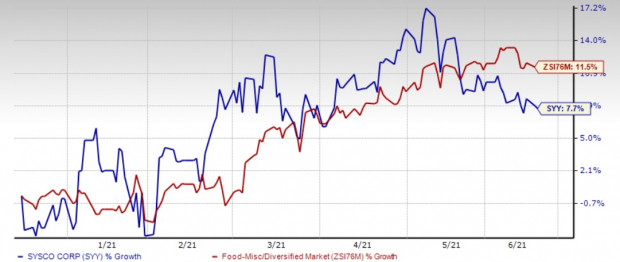

Shares of this Zacks Rank #3 (Hold) company have increased 7.7% in the past three months compared with the industry’s growth of 11.5%.

Binge on These 3 Food Stocks

Medifast MED, which currently carries a Zacks Rank #1 (Strong Buy), has a trailing four-quarter earnings surprise of 12.7%, on average. You can see the complete list of today’s Zacks #1 Rank stocks here.

Hain Celestial HAIN has a Zacks Rank #2 (Buy) and its bottom line outpaced the Zacks Consensus Estimate by 26.4% in the trailing four quarters, on average.

Nomad Foods NOMD has a Zacks Rank #2 and its bottom line outpaced the Zacks Consensus Estimate by 10.3% in the trailing four quarters, on average.

Zacks' Top Picks to Cash in on Artificial Intelligence

In 2021, this world-changing technology is projected to generate $327.5 billion in revenue. Now Shark Tank star and billionaire investor Mark Cuban says AI will create ""the world's first trillionaires."" Zacks' urgent special report reveals 3 AI picks investors need to know about today.

See 3 Artificial Intelligence Stocks With Extreme Upside Potential>>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

The Hain Celestial Group, Inc. (HAIN): Free Stock Analysis Report

Sysco Corporation (SYY): Free Stock Analysis Report

MEDIFAST INC (MED): Free Stock Analysis Report

Nomad Foods Limited (NOMD): Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.