Synopsys SNPS posted a backlog of $10.1 billion in the third quarter of fiscal 2025. Behind this massive backlog are multiple factors like growing demand for Synopsys.ai’s GenAI, AgentEngineer and multi-die and advanced packaging offerings.

Industry-wide investments in AI and high-performance computing are fueling demand for advanced chip design tools, emulation, and prototyping platforms, such as ZeBu Server 5 and HAPS-200, benefiting Synopsys.

Synopsys is also gaining from continued strength in Europe and North America, with Simulation & Analysis products performing well in high-tech, aerospace, and automotive sectors. Additionally, the acquisition of Ansys has expanded SNPS’ addressable market.

The acquisition of Ansys has significantly added to Synopsys’ addressable market and strengthened its position as a silicon-to-systems player. Ansys has also diversified SNPS’ revenue sources and customer base, adding strong Simulation & Analysis capabilities to the existing Electronic Design Automation (EDA) portfolio.

These factors have led SNPS to provide a revenue projection of $7.03 billion to $7.06 billion for fiscal 2025 ending in October. The Zacks Consensus Estimate for the same has been pegged at $7.05 billion, indicating growth of 12.5%.

How Competitors Fare Against Synopsys

Synopsys faces competition from EDA vendors, such as Cadence Design Systems Inc. CDNS and Siemens SIEGY. Siemens EDA, which is Siemens' electronic design automation division and Cadence Design System both provide EDA tools, like software, hardware, and services essential for designing chips and semiconductor devices.

These EDA Vendors, including Cadence and Siemens, offer products focused more on distinct phases of the IC design process and provide a range of services to companies worldwide to help optimize their product development process, among other things. Their facilities could increase competition, leading to lower prices and profits for Synopsys.

SNPS’ Price Performance, Valuation and Estimates

Shares of SNPS have lost 1.5% year to date against the Computer - Software industry’s growth of 22.3%.

Image Source: Zacks Investment Research

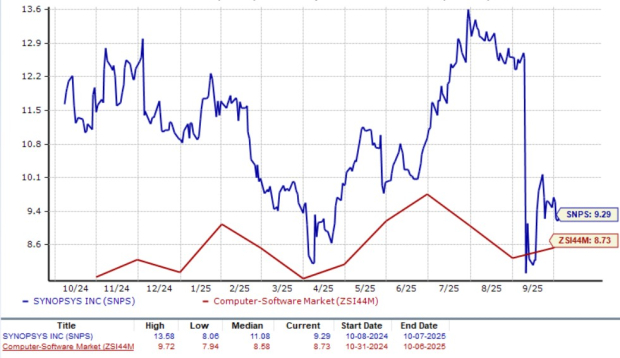

From a valuation standpoint, SNPS trades at a forward price-to-sales ratio of 9.29X, higher than the industry’s average of 8.73X.

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for SNPS’ fiscal 2025 earnings implies a year-over-year decline of 2.8%, while the consensus estimate for 2026 earnings implies year-over-year growth of 9.5%. The consensus estimate for fiscal 2025 and 2026 has been revised downward in the past 30 days.

SNPS currently carries a Zacks Rank #5 (Strong Sell).

Image Source: Zacks Investment Research

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. Little-known AI firms tackling the world's biggest problems may be more lucrative in the coming months and years.

See "2nd Wave" AI stocks now >>Synopsys, Inc. (SNPS) : Free Stock Analysis Report

Cadence Design Systems, Inc. (CDNS) : Free Stock Analysis Report

Siemens AG (SIEGY) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.