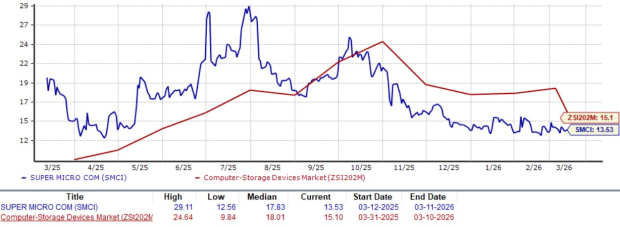

Super Micro Computer SMCI trades at a P/E multiple of 13.53X, lower than the Zacks Computer- Storage Devices industry’s 15.1X valuation, making it relatively undervalued at present. This undervaluation is further demonstrated by the Zacks Value Score of B.

SMCI Forward 12-Month (P/E) Valuation Chart

Image Source: Zacks Investment Research

Considering its undervaluation and massive demand for its server products, investors are wondering if this is the right opportunity to invest in the SMCI stock. Let us delve deeper into the fundamentals and financials of the stock to get a clear picture.

SMCI Gains From Rising Demand for AI Infrastructure

Super Micro Computer is well-positioned to benefit from the growing demand for AI infrastructure. The company is often the first to market with the latest AI servers, including systems built on NVIDIA’s B200 and GB200 platforms, giving it a strong edge. SMCI’s modular design approach allows rapid customization, supported by a large R&D team.

Super Micro Computer’s high-performance and energy-efficient servers are gaining traction among AI data centers, HPC and hyperscalers. SMCI has a broad AI portfolio spanning Super AI Station, Supermicro SYS-542T-2R, Supermicro AI PC, Supermicro Edge AI Systems and Supermicro's Fanless Compact Edge System.

SMCI is also expanding into full-stack IT solutions through DCBBS, bundling servers, cooling and networking into one offering. SMCI’s DCBBS technology combines SMCI’s rack-scale, plug-and-play server architecture with its latest direct liquid cooling technology, enabling fast deployment.

SMCI’s DCBBS accounted for 4% of SMCI’s profit in 2025, and the company expects the contribution to rise to double digits by the end of 2026. SMCI plans to roll out 6,000 racks per month, including 3,000 liquid-cooled racks and generate enough revenues so it reaches its $40-billion revenue goal in fiscal 2026.

However, SMCI is facing some near-term headwinds.

SMCI Grapples With Competitive & Concentration Risks

SMCI’s revenue streams are heavily dependent on the AI industry, with AI GPU platforms contributing more than 90% of revenues. This exposes SMCI to the boom and bust cycles of a single industry. Since SMCI works in a capex-heavy industry, its inventory has also surged to $10.6 billion in the second quarter of fiscal 2026 from $5.7 billion in the first quarter of fiscal 2026 and $4.7 billion at the end of fiscal 2025.

SMCI generated a negative free cash flow in the second quarter of fiscal 2026, indicating elevated working capital needs to support rapid growth. Super Micro Computer’s working capital problem further stems from the massive operational scale-up required to meet unprecedented AI rack demand. The competition from giants like Hewlett Packard Enterprise HPE and Dell Technologies DELL is adding to SMCI’s challenges.

Hewlett Packard Enterprise offers a range of servers, including HPE ProLiant, HPE Synergy, HPE BladeSystem and HPE Moonshot servers. Dell Technologies has built the Dell AI Factory in collaboration with NVIDIA. Dell Technologies also collaborated with Red Hat Enterprise Linux AI for Dell PowerEdge servers.

To escape the high competition in the server market, SMCI has entered Client, Edge and Consumer AI Markets. The venture into the newer market has brought SMCI to a crossroads with HP Inc., Lenovo LNVGY and Dell Technologies. Dell Technologies has numerous workstations that offer AI capabilities like XPS 13, Inspiron 14 Plus, Inspiron 14, Latitude 7455 and Latitude 5455.

Lenovo has AI PCs in some versions of ThinkPad, Yoga, IdeaPad and Lenovo Legion. The rising competition across markets has pushed SMCI’s bottom line to a single-digit growth rate despite having double-digit topline growth. The Zacks Consensus Estimate for SMCI’s fiscal 2026 earnings indicates single-digit percentage growth. Earnings estimates for fiscal 2026 have been revised downward in the past 30 days.

Image Source: Zacks Investment Research

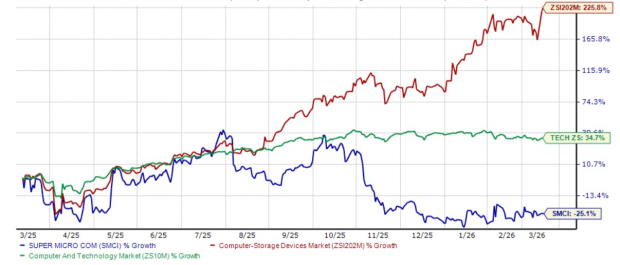

SMCI’s Stock on Constant Decline

These factors have raised investors’ concerns, pushing SMCI’s stock down. The SMCI stock has declined 25.1% in the past year, underperforming the Zacks Computer - Storage Devices industry and the broader sector’s growth of a whopping 225.8% and 234.7%, respectively.

SMCI's 1-Year Price Performance Chart

Image Source: Zacks Investment Research

Conclusion: Hold SMCI Stock Now

Super Micro Computer remains fundamentally strong due to its favourable positioning in the rapidly expanding AI infrastructure market and its relatively modest valuation of 13.53X earnings, which sits below the industry average. However, elevated inventory levels, negative free cash flow and rising competition are concerns for the stock. Given these mixed factors, we suggest investors retain this Zacks Rank #3 (Hold) stock at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks Names #1 Semiconductor Stock

This under-the-radar company specializes in semiconductor products that titans like NVIDIA don't build. It's uniquely positioned to take advantage of the next growth stage of this market. And it's just beginning to enter the spotlight, which is exactly where you want to be.

With strong earnings growth and an expanding customer base, it's positioned to feed the rampant demand for Artificial Intelligence, Machine Learning, and Internet of Things. Global semiconductor manufacturing is projected to explode from $452 billion in 2021 to $971 billion by 2028.

See This Stock Now for Free >>Dell Technologies Inc. (DELL) : Free Stock Analysis Report

Super Micro Computer, Inc. (SMCI) : Free Stock Analysis Report

Lenovo Group Ltd. (LNVGY) : Free Stock Analysis Report

Hewlett Packard Enterprise Company (HPE) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.