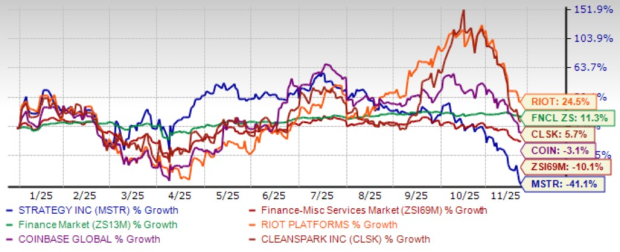

Strategy MSTR shares have plunged 41.1% year to date (YTD), underperforming the broader Zacks Finance sector’s growth of 11.3% and the Zacks Financial- Miscellaneous Services industry’s decline of 10.1%.

Strategy shares have also lagged behind key peers, such as Riot Platforms RIOT, CleanSpark CLSK and Coinbase Global COIN, year to date. While Riot and CleanSpark have gained 24.5% and 5.7%, respectively, Coinbase has declined 3.1% over the same period.

Strategy's share price decline reflects growing concerns over its high valuation and the implementation of its Bitcoin-focused strategy. This stock is highly sensitive to the broader crypto-market downturn and Bitcoin's ongoing volatility.

MSTR Stock's Performance

Image Source: Zacks Investment Research

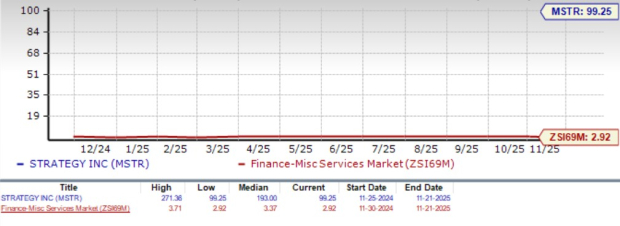

Strategy’s Rich Valuation Raises Concerns

From a valuation standpoint, Strategy remains highly expensive, trading at a forward 12-month price-to-sales ratio of 99.25X — far above the industry average of 2.92X. Its Value Score of F reinforces concerns that the stock is significantly overvalued. Even key peers such as Riot Platforms (6.4X), CleanSpark (2.86X) and Coinbase (7.91X) trade at far more reasonable multiples, underscoring Strategy’s stretched valuation.

Price/Sales Ratio (F12M)

Image Source: Zacks Investment Research

While the near-term picture appears challenging, several underlying factors continue to support its long-term potential. Let’s take a closer look.

Bitcoin Accumulation Drives MSTR’s Growth Path

Despite near-term challenges, the company’s long-term prospects remain firmly anchored in its massive Bitcoin treasury and disciplined accumulation strategy. As of Oct. 26, 2025, the company held approximately 640,808 BTC, valued at nearly $71 billion. This represents one of the largest corporate Bitcoin positions globally and provides a powerful balance-sheet asset that continues to shape the company’s financial trajectory. Year to date, Strategy has generated a 26% BTC yield and nearly $12.9 billion in Bitcoin-related gains, underscoring the strength of its treasury approach. With a full-year BTC yield target of 30% for 2025, the company remains focused on long-term value creation.

A key driver of Strategy’s Bitcoin-accumulation model is its broad and reliable access to capital markets. During the third quarter, the company raised approximately $5.1 billion in net proceeds through its various equity-based financing programs, which include the Common Stock ATM Program, STRK ATM Program, STRF ATM Program and STRD Stock ATM Program. These programs collectively supply the liquidity required to scale its Bitcoin holdings.

Furthermore, from Oct. 1 to Oct. 26, Strategy generated an additional $89.5 million in net proceeds across these ATM platforms, demonstrating consistent capital inflows. The company’s fundraising capacity was further strengthened by the successful IPO of STRC Stock, which broadened its capital-raising ecosystem and added another vehicle to support future Bitcoin acquisitions. These capital market moves support its large Bitcoin strategy and support long-term growth.

Software Growth Strengthens Strategy’s Core Business

Strategy’s software business continues to show steady momentum, providing a solid foundation beneath the company’s Bitcoin-heavy strategy. In the third quarter of 2025, total software revenues rose 10.9% year over year, supported by rising demand for its analytics solutions and increased customer adoption.

Subscription services were a key highlight, surging 65.4% year over year, marking a strong shift toward recurring, high-margin revenues. This growth in subscriptions enhances revenue stability and reduces reliance on one-time license sales.

By consistently expanding its software segment alongside its Bitcoin treasury strategy, Strategy is strengthening its long-term value proposition. The growing analytics platform not only diversifies revenues but also helps balance the higher volatility associated with digital-asset holdings.

MSTR Maintains Positive 2025 Earnings Guidance

Strategy reaffirmed its full-year outlook, underscoring management’s confidence in meeting its targets. The company’s projection of $80 per share reflects expectations for remarkably strong profitability in 2025.

The Zacks Consensus Estimate for 2025 earnings is pegged at $78.04 per share, marking a sharp turnaround from a loss of $15.73 per share over the past 30 days. The company reported a loss of $6.72 per share in 2024, highlighting a favorable earnings trajectory.

Earnings Estimate Trend

Image Source: Zacks Investment Research

Conclusion: Stay on Hold for the Time Being

Strategy’s deep Bitcoin exposure, strong capital-raising capacity and steady software growth continue to support its long-term potential. However, the stock’s steep year-to-date decline, elevated sensitivity to crypto volatility and extremely rich valuation create a challenging near-term setup. With strengths balanced by meaningful risks, investors may be best served by adopting a wait-and-see stance on this Zacks Rank #3 (Hold) stock for now. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the favorite stock to gain +100% or more in the months ahead. They include

Stock #1: A Disruptive Force with Notable Growth and Resilience

Stock #2: Bullish Signs Signaling to Buy the Dip

Stock #3: One of the Most Compelling Investments in the Market

Stock #4: Leader In a Red-Hot Industry Poised for Growth

Stock #5: Modern Omni-Channel Platform Coiled to Spring

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor. While not all picks can be winners, previous recommendations have soared +171%, +209% and +232%.

Download Atomic Opportunity: Nuclear Energy's Comeback free today.Strategy Inc (MSTR) : Free Stock Analysis Report

Riot Platforms, Inc. (RIOT) : Free Stock Analysis Report

Cleanspark, Inc. (CLSK) : Free Stock Analysis Report

Coinbase Global, Inc. (COIN) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.