")

Stocks Higher on Earnings and GDP Data

Market Movers

- Q2 Advance GDP rose 2.1% more than forecast (1.8% but below Q1's 3.1% increase.

- Earnings are a net positive for stocks today as large companies continue to report.

- Stocks look to close a see-saw week in positive territory.

Mike’s Commentary

This week we’ve seen back and forth action with earnings as a backdrop. Today’s net assessment of the multiple releases was positive, with Twitter and Alphabet gaining and Amazon trading lower after an earnings miss attributed to one-day delivery costs. Twitter beat on sales and user growth so shares rose more than $2 to above $40/share. Among less digital stocks, Weyerhaeuser and McDonald's also are trading higher post-results with industrial machinery company Illinois Tool Works missing on earnings estimates and guiding lower and shedding about 2% at the open as a result.

Market performance for this week is in the eye of the benchmark. Through last night, the Dow was down for the week and the index is currently underperforming. The S&P, meanwhile, began this morning over 27 points above last Friday’s reading and seeks to add to gains, while the Nasdaq Composite hope to close out the day at a new record though the 8,321 level achieved on Thursday may be a bit out of reach.

European stocks are rebounding today from the ECB’s "worse and worse" assessment of economic conditions yesterday and that also appears to be helping sentiment today.

Today’s advance GDP reading for Q2 came in at 2.1% annualized, better than the forecast of 1.8%. Personal consumption rose 4.3%, also more than expected (4.0%) and the GDP price index rose 2.4%. The results mark a slowdown from the 3.1% registered in Q1 and but beat expectations thanks to consumer spending increases that outweighed weaker business investment and exports. This seems to perfectly frame the decision confronting the FOMC next week – cut to get ahead of slowing growth or stand pat in a decent economy.

The real action comes next week with the Fed’s preferred inflation indicator, the PCE deflator, to be announced on Tuesday just before the Fed’s rate decision on Wednesday, where the institution is widely expected to cut rates by at least 25bp.

The case for a 25bp cut is that other central banks are easing and market rates are falling even though the economy as measured by employment and consumer confidence is still good. The argument for more stimulus is that the Fed needs to get ahead of recession indicators and the fact the next meeting is not until September. Though with a 50bp cut, communication is key. Some academic research suggests that with rates low, an early and significant rate cut will have more impact, but the downside is the signaling effect to the market that economic conditions are worse than they appear.

With the market not doing much, we though we’d share some back-of-the- envelope analysis we did around short position changes for Russell 2000 additions and deletions. We often attribute increases in short interest for Russell 2000 additions to hedging by funds that directly track or benchmark to the Russell 2000 index and short positions initiated by ETFs that seek to provide inverse exposure to the Russell 2000 (e.g. RWM). Russell 2000 deletions often see a reversal of this phenomenon.

Russell 2000 additions saw a significant increase in short positions while Russell 2000 removals saw a decline – largely as we expected. It shows that not all short positions are bets against a specific company. Please see the Technical Take section for more.

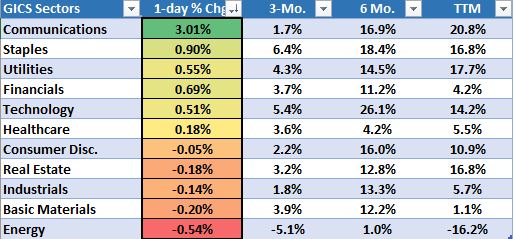

Sector Recap

Technical Take

Brian's awesome Technical Take returns on Monday...

Using short position data from 6/14/19 and 7/15/19 (since the Russell reconstitution date of 6/28/19 was a short interest settlement date and this muddied the waters) we see that Russell 2000 additions had a huge increase in short position, removals had a significant decline, and the Russell 2000 as a whole had a slight increase – largely as we expected.

In the aggregate Russell additions saw a 122 million share increase in short position while removals saw a 95 million share decrease.

- There was an eye-popping 333% average increase in Russell addition shorts.

- Even calculating a “trimmed mean” taking out the top and bottom 10% of outlier values resulted in an average 159% average increase.

- The median increase for Russell additions was 99%.

- Russell deletions saw a 36% average decrease and 34% median decrease

- The Russell 2000 overall saw a 38% increase in simple average short position and a 6% median increase.

Short Interest Change

| Pre-Post Russell | Simple Avg. Change | Median Change | Aggregate Avg. Change | |

|---|---|---|---|---|

| Russell 2000 additions | 333% | 99% | 42% | |

| Russell 2000 removals | -36% | -34% | -22% | |

| Russell 2000 Index | 38% | 6% | 6% | |

Nasdaq's Market Intelligence Desk (MID) Team includes:

Charles Brown is Associate Vice President on The Market Intelligence Desk with over 20 years of equity capital markets experience. Charlie has extensive knowledge of equity trading on both floor and screen based marketplaces. Charlie assists with the management of The Market Intelligence Desk and works with Nasdaq listed companies providing them with insightful objective trading analysis.

Steven Brown is a Managing Director on the Market Intelligence Desk (MID) at Nasdaq with over twenty years of experience in equities. With a focus on client retention he currently covers the Financial, Energy and Media sectors.

Christopher Dearborn is a Managing Director on the Market Intelligence Desk (MID) at Nasdaq. Chris has over two decades of equity market experience including floor and screen based trading, corporate access, IPOs and asset allocation. Chris is responsible for providing timely, accurate and objective market and trading-related information to Nasdaq-listed companies.

Brian Joyce, CMT is a Managing Director on the Market Intelligence Desk (MID) at Nasdaq. Before joining Nasdaq Brian spent 16 years as an institutional trader executing equity and options orders for both the buy side and sell side. He also provided trading ideas and wrote technical analysis commentary for an institutional research offering. Brian focuses on helping Nasdaq’s Financial, Healthcare and Transportation companies, among others, understand the trading in their stock. Brian is a Chartered Market Technician (CMT).

Michael Sokoll, CFA is Associate Vice President on the Market Intelligence Desk (MID) at Nasdaq with over 25 years of equity market experience. In this role, he manages a team of professionals responsible for providing NASDAQ-listed companies with real-time trading analysis and objective market information.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.