The 2025 Q3 earnings cycle continues to chug along, with a nice chunk of S&P 500 companies already delivering results. The period has so far been one of resilience, with overall growth remaining strong and an above-average number of companies exceeding quarterly expectations.

Wayfair posted notably strong results, raising guidance as a result. Let’s take a closer look at the release.

Wayfair

Wayfair posted a double-beat concerning our headline expectations, with adjusted EPS of $0.70 climbing 220% year-over-year and sales of $3.1 billion growing 8.1%. Further, its 6.7% adjusted EBITDA margin reflected its highest read ever outside of the pandemic.

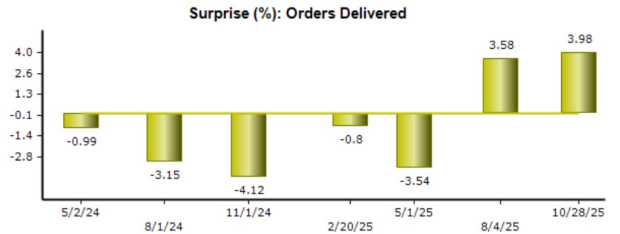

Orders delivered grew by more than 5% year-over-year, including new orders now growing mid-single digits for two consecutive periods. As shown below, the company has now strung together a few sizable beats concerning its Orders Delivered, reflective of the above-mentioned momentum.

Image Source: Zacks Investment Research

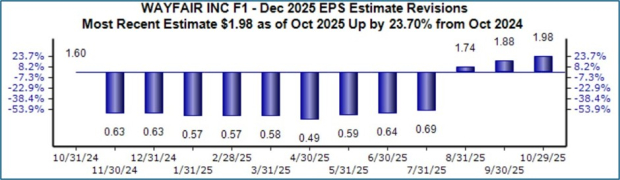

The stock sports a favorable Zacks Rank #2 (Buy), with EPS expectations moving higher for its current fiscal year. It’s reasonable to expect Wayfair’s EPS outlook to remain bullish in the near-term on the back of the strong quarterly results.

Image Source: Zacks Investment Research

Bottom Line

The 2025 Q3 earnings season has so far been stellar, with an above-average number of companies exceeding quarterly expectations. Growth has remained strong, with the big banks also giving us a solid read on the state of the consumer.

And concerning post-earnings pops so far, Wayfair W posted results that had investors celebrating.

Zacks' Research Chief Picks Stock Most Likely to "At Least Double"

Our experts have revealed their Top 5 recommendations with money-doubling potential – and Director of Research Sheraz Mian believes one is superior to the others. Of course, all our picks aren’t winners but this one could far surpass earlier recommendations like Hims & Hers Health, which shot up +209%.

See Our Top Stock to Double (Plus 4 Runners Up) >>Wayfair Inc. (W) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.