Sterling Infrastructure, Inc. STRL has moved away from low-bid, margin-dilutive projects and instead prioritized large, mission-critical developments where its execution capabilities create tangible value. This approach is most visible in the data center market, which has emerged as a core growth engine. In the third quarter of 2025, data center-related revenue grew at a triple-digit rate year over year, supported by strong customer demand and repeat business, highlighting the benefits of focusing on scale, complexity and long-term partnerships.

The payoff from this selectivity is evident in profitability metrics. Gross margins expanded meaningfully year over year, reflecting better project mix, tighter risk controls and improved pricing discipline. Management emphasized that contracts with clearer scopes and balanced risk allocation have helped limit cost overruns and execution surprises, a chronic issue in the construction sector. This has translated into stronger operating cash flow generation, giving Sterling added financial flexibility for debt reduction, share repurchases and strategic acquisitions.

Importantly, disciplined project selection has not come at the expense of growth. Backlog expanded sharply year over year, driven primarily by the E-Infrastructure segment’s awards and future phase opportunities, providing multiyear revenue visibility. By focusing on quality over volume, Sterling appears to be building a more resilient earnings profile.

Overall, the company’s selective bidding strategy is increasingly reflected in higher margins, stronger cash flows and improved returns on capital, reinforcing the view that project selection is a key pillar behind Sterling’s superior performance.

Sterling’s Competitive Position

Being exposed to the data center-driven market, Sterling faces notable competition from the key market players, including Quanta Services, Inc. PWR and EMCOR Group, Inc. EME.

Quanta is the largest player tied to data center demand through its dominance in power generation, transmission and high-voltage electrical infrastructure. Its growth is leveraged more to grid-scale investments than to the data center site itself. Conversely, EMCOR is more directly involved in data center construction through its mechanical, electrical and specialty contracting services. EMCOR’s exposure is broad and recurring, particularly in electrical and HVAC systems, but data centers represent one of several verticals rather than the core growth engine.

Sterling differentiates itself by combining site development with mission-critical electrical services, allowing it to capture earlier phases of data center projects and benefit from faster revenue conversion. This integrated positioning gives Sterling a more concentrated and higher-growth exposure to data center demand than either Quanta or EMCOR.

STRL Stock’s Price Performance & Valuation Trend

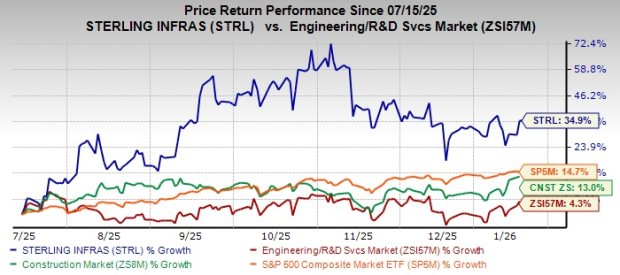

Shares of this Texas-based infrastructure services provider have gained 34.9% in the past six months, outperforming the Zacks Engineering - R and D Services industry, the broader Construction sector and the S&P 500 Index.

Image Source: Zacks Investment Research

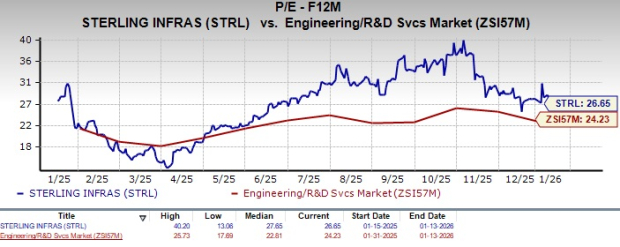

STRL stock is currently trading at a premium compared with its industry peers, with a forward 12-month price-to-earnings (P/E) ratio of 26.65, as shown in the chart below.

Image Source: Zacks Investment Research

Earnings Estimate Revision for STRL

STRL’s earnings estimates for 2025 and 2026 have remained unchanged over the past 60 days. However, the estimated figures for 2025 and 2026 imply year-over-year growth of 71% and 14.6%, respectively.

Image Source: Zacks Investment Research

Sterling currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Just Released: Zacks Top 10 Stocks for 2026

Hurry – you can still get in early on our 10 top tickers for 2026. Handpicked by Zacks Director of Research Sheraz Mian, this portfolio has been stunningly and consistently successful.

From inception in 2012 through November, 2025, the Zacks Top 10 Stocks gained +2,530.8%, more than QUADRUPLING the S&P 500’s +570.3%.

Sheraz has combed through 4,400 companies covered by the Zacks Rank and handpicked the best 10 to buy and hold in 2026. You can still be among the first to see these just-released stocks with enormous potential.

See New Top 10 Stocks >>Quanta Services, Inc. (PWR) : Free Stock Analysis Report

EMCOR Group, Inc. (EME) : Free Stock Analysis Report

Sterling Infrastructure, Inc. (STRL) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.