Data warehousing expert Snowflake (NYSE: SNOW) reported earnings on Wednesday evening, crushing Wall Street's consensus estimates but setting up fairly modest guidance targets for the next reporting period. The company also took this opportunity to go all-in on artificial intelligence (AI).

In other words, Snowflake did exactly what it was supposed to do in the first quarter. Some investors acted surprised, and Snowflake's stock opened Thursday trading 15% below Wednesday's closing price. But the soft guidance simply followed the familiar pattern of setting up another lowball target while stomping all over the last one.

Here's what you need to know about Snowflake's report for the first quarter of the 2024 fiscal year. In a digital nutshell, Snowflake is doing business as usual despite a challenging economy, and the company is making a sharp turn into an explosive AI opportunity.

Snowflake's Q1 by the numbers

As usual (more on the repeatable trend in a moment), Snowflake delivered financial results above the top end of management's guidance.

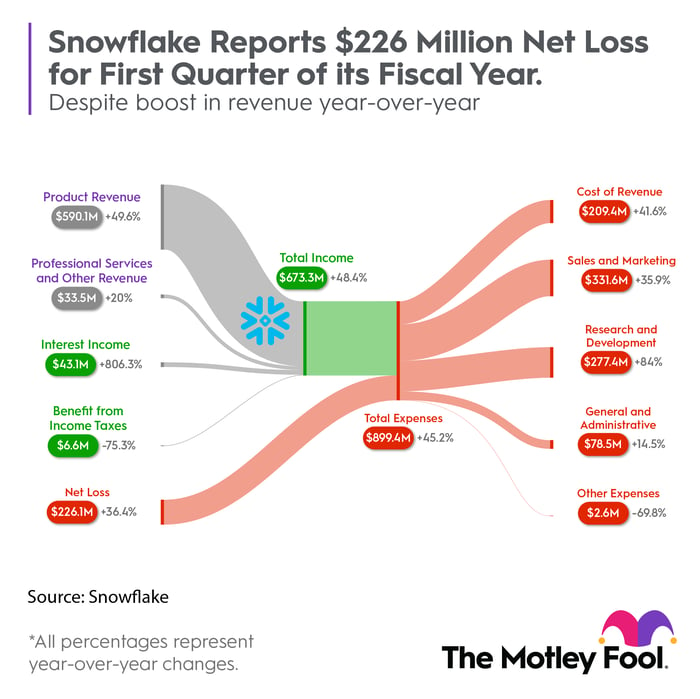

The guidance range for first-quarter product revenue topped out at $573 million, but the actual product sales came in at $590 million. That's a 50% year-over-year increase, driven by rising interest in feeding data into AI and machine learning systems.

Management expected the adjusted operating margin to stay near the breakeven point, where it landed in the year-ago report. Instead, the robust top-line performance widened this key margin to 5%.

On top of that operating surprise, Snowflake also saw a ninefold increase in interest income. When interest rates go up, Snowflake's bottom line follows suit. That's a helpful side effect of a squeaky-clean balance sheet with zero debt and $3.9 billion in cash and short-term investments:

A solid history of setting reachable targets

This was the seventh Snowflake quarter in a row with substantial surprises across the board. By that, I mean revenue beating Wall Street's guidance-based estimates by at least 2.3% while earnings came in more than 160% above expectations.

I mean, the pattern has become pretty predictable in recent quarters:

- Snowflake reports results well above management's guidance and analysts' estimates.

- Guidance points to slower growth in the next period, based on economic instability and unpredictable order flows.

- Wall Street grumbles in unison, setting lower price targets and driving the current stock price lower.

- Three months later, it's time to do the same dance again.

Between the guidance-inspired price drops, Snowflake continues to run its data management business with innovative precision. And right now, that means making a hard turn into the heart of the AI market.

How Snowflake is doubling down on AI

Snowflake is really putting its back into the AI opportunity. As CEO Frank Slootman put it on the earnings call, "Generative AI, with its text style of interaction, has captured the imagination of society at large." Snowflake clearly sees AI as more than just a trend -- it's the future.

The sea change is already underway. In the first quarter, over 1,500 customers used Snowflake for AI, machine learning, or data science workloads. That's a 91% increase in AI-related activity on a year-over-year basis.

Furthermore, the company just acquired the Neeva search engine -- an innovative player in data search that applies ChatGPT-like generative AI tools to the task of finding the right data in large data pools. This isn't just a strategic move; it's a potential game changer. With Neeva's technology, Snowflake users and developers can build rich, search-enabled, and conversational experiences. It's like having a friendly chat with your data warehouse. Anything that makes the right data more accessible looks like a strong selling point for Snowflake's products and services.

As Slootman put it, "Our goal is for all the world's data to find its way to Snowflake and not encounter any limitations in terms of use and purpose." It's a bold vision and one that Snowflake is well on its way to achieving.

If you're looking for a company with obvious ties to the AI revolution, Snowflake is worth a closer look. With its predictably strong financial performance and a sharp strategic focus on AI, this is a compelling investment opportunity in today's data-driven economy.

10 stocks we like better than Snowflake

When our analyst team has a stock tip, it can pay to listen. After all, the newsletter they have run for over a decade, Motley Fool Stock Advisor, has tripled the market.*

They just revealed what they believe are the ten best stocks for investors to buy right now… and Snowflake wasn't one of them! That's right -- they think these 10 stocks are even better buys.

*Stock Advisor returns as of May 22, 2023

Anders Bylund has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Snowflake. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.