Investing requires two skills: evaluating good business opportunities and determining a good price to pay. When it comes to restaurant technology company Toast (NYSE: TOST), allow me to start with the price to pay, otherwise known as the valuation.

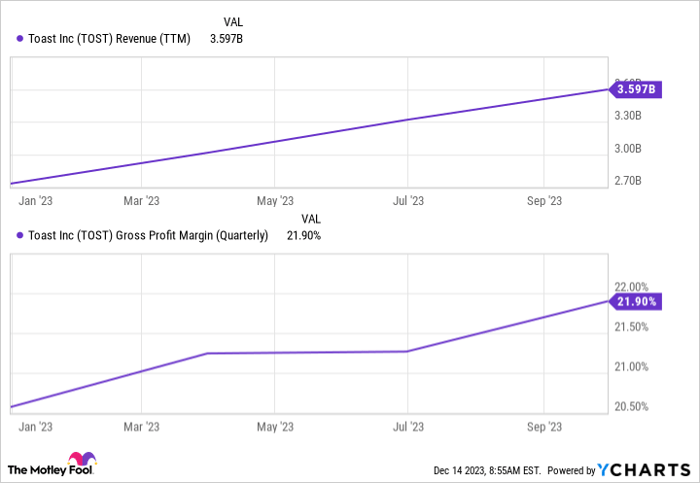

At $19 per share, Toast would have a market capitalization of about $10 billion. The company has generated almost $3.6 billion in trailing-12-month revenue. Therefore, trading at $19 per share or lower, Toast stock has a price-to-sales (P/S) valuation of less than 3.

In isolation, Toast's valuation is quite reasonable, which might motivate investors to buy shares while they're still below $19 -- they trade at $17.24 as of this writing. But to determine whether or not Toast stock is a good buy, investors must solve for the other half of the equation and evaluate whether this is a good business opportunity.

Spoiler alert: Toast is promising.

Why Toast is a promising business

Toast generates revenue by selling hardware for processing payments at restaurants as well as by providing professional services to get everything set up. These two business segments (hardware and professional services) have negative gross profit margins.

Once up and running, Toast also generates revenue by taking a small cut of each transaction and by selling subscription software modules to its restaurant customers. Of these two revenue generators, transactional revenue is less profitable with a 22% gross margin through the first three quarters of 2023.

However, Toast's subscription revenue boasted a 67% gross margin over the same period, up from 65% last year. Moreover, the company's subscription revenue is growing fast, up 56% year over year so far in 2023.

As Toast's subscription revenue grows, its overall gross margin gets a boost. That's what's been happening over the past year, as seen in the chart below.

Data by YCharts.

Higher gross profit points to Toast's potential when it comes to future operating profits. To be clear, the company reported an operating loss of $231 million through the first three quarters of 2023, which is substantial. But that figure is improving, and if its gross profit can keep trending higher, then its operating profits should follow suit.

Toast's largest operating expense is sales and marketing, which makes sense. The company targets many smaller restaurant companies in contrast to competitor Olo, which has secured business from many larger restaurant players. It takes a little more effort from the sales team to target these players.

Even though Toast is spending a lot on sales and marketing, at least it's getting results. As of the third quarter, 99,000 restaurant locations were using the company's products. That's up 34% year over year and 6% quarter over quarter.

What could go wrong

Earlier this year, Toast rolled out a fee on all orders that wasn't well received by its customers. Management quickly eliminated the fee and apologized, but it's unclear how much brand damage was done. In short, investors are about to find out how sticky this business is and whether restaurants are willing to switch from one technology platform to another.

Some might point out that Toast still grew in Q3. However, there's a lag between what's happened and how customers may respond. When the company talks about risks, it says, "Because we recognize revenue from subscription contracts over the term of the relevant subscription period, downturns or upturns in sales are not immediately reflected in full in our results of operations."

In other words, investors need to keep an eye on Toast's customer count and its average spending per customer over the coming year -- contracts with customers are generally between one and three years in length.

Assuming Toast does retain its customers in spite of its unforced error, that would be a massively bullish signal for long-term investors. It would mean that its business is indeed sticky, and customers are reluctant to switch even when frustrated.

It would also suggest that Toast can pull back on sales and marketing expenses someday, gaining operating leverage with scale.

On top of winning new customers, Toast can upsell its existing customers with additional subscription software modules -- most customers use only a fraction of the tools available. This would continue to boost its subscription revenue, sending its gross profit higher.

With that in mind, Toast is a promising company trading at a reasonable valuation, which is why some investors may want to pick up some shares today while they still trade below $19. This may also be a good candidate for dollar-cost averaging. Investors can buy some shares today but also add to their positions as the platform's stickiness is made evident in future financial results.

Should you invest $1,000 in Toast right now?

Before you buy stock in Toast, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now... and Toast wasn't one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of December 11, 2023

Jon Quast has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Olo. The Motley Fool recommends Toast. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.