Key Points

ServiceNow stock is plummeting as growth investors rotate capital away from legacy SaaS names.

ServiceNow's revenue has been decelerating for years, and the company's gross margin profile is eroding.

Traditional SaaS platforms are increasingly facing competition from AI agents developed by Anthropic and OpenAI.

- 10 stocks we like better than ServiceNow ›

Over the last couple of months, some growth investors have rotated away from SaaS stocks over fears that agentic AI toolkits from OpenAI and Anthropic could render traditional software platforms obsolete. With shares down over 38% on the year, ServiceNow (NYSE: NOW) has been one of the largest casualties of the so-called SaaSpocalypse.

In my view, the AI obsolescence narrative is overblown. However, ServiceNow's revenue growth and gross margins reveal deeper, longer-standing issues. What looks like modest deterioration is masking a small but persistent drag that raises real questions about whether ServiceNow still qualifies as a high-growth SaaS machine.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Image source: The Motley Fool.

ServiceNow was weakening before AI agents burst onto the scene

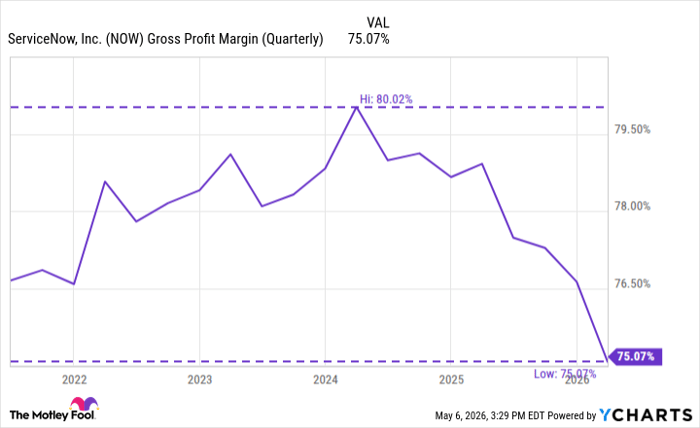

ServiceNow's gross margin has slipped from about 80% in fiscal year 2024 to 75% as of the end of the first quarter this year. While subscription margins appear relatively strong in the mid-70% range, this profile is about 400 basis points lower than the same period one year ago.

Data by YCharts.

Erosion in a historically high-margin business is concerning enough on its own. The real culprit, though, is a volatile performance from Professional Services. This segment's margin profile has swung materially and is generally negative. Even though this division only accounts for about 3% of revenue, its worsening profitability is now visibly dragging ServiceNow's blended margin lower.

Why was ServiceNow's deceleration overlooked?

Due to their labor-intensive nature, professional services tend to carry lower margins for enterprise software businesses. Companies eat these losses in exchange for accelerating platform adoption and hopefully locking in larger, higher-margin recurring revenue later. Unfortunately, ServiceNow's mix hasn't fundamentally changed for the better.

For a while, investors merely shrugged off these dynamics. Explosive revenue growth outweighed the blended-margin discussion, making the stock priced for hyper-growth fueled by AI tailwinds. Now, revenue expansion is moderating as competition from AI agents looms.

ServiceNow's revenue trajectory since 2020 depicts a classic maturation story -- one that is now testing the limits of what investors will pay for.

| Period | Total Revenue | % Growth (YOY) |

|---|---|---|

| Fiscal 2020 | $4.5 billion | 31% |

| Fiscal 2021 | $5.9 billion | 30% |

| Fiscal 2022 | $7.2 billion | 23% |

| Fiscal 2023 | $8.9 billion | 24% |

| Fiscal 2024 | $10.9 billion | 22% |

| Fiscal 2025 | $13.3 billion | 21% |

| Q1 2026 | $3.8 billion | 22% |

Data source: Investor Relations. YOY = Year over year.

Growth has decelerated from the 30% range to the low 20s as ServiceNow's run-rate sales approach about $16 billion. While this slowdown is not catastrophic, it signals a company that seems to be transitioning from high-growth to steady compounder -- hardly the profile that commands a premium valuation.

The verdict: Proceed with caution

All told, ServiceNow isn't collapsing or at risk of going belly-up. But the combination of slowly eroding subscription margins, a worsening services business, and steadily decelerating top-line growth paints a picture of a business that no longer fits a growth-company mold.

Given the analysis above, it's clear that ServiceNow was facing pressures long before the latest AI hype. However, these issues seem to matter more now that the growth story has shifted.

Investors chasing a quick rebound may be disappointed in ServiceNow stock. In a market that rewards genuine growth and durable profitability, ServiceNow looks increasingly like one company to avoid -- or at least approach with healthy caution -- rather than a dip worth buying.

Should you buy stock in ServiceNow right now?

Before you buy stock in ServiceNow, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and ServiceNow wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $475,926!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,296,608!*

Now, it’s worth noting Stock Advisor’s total average return is 981% — a market-crushing outperformance compared to 205% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of May 8, 2026.

Adam Spatacco has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends ServiceNow. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.