I shared this last month, but the topic of this recent interview with Lead Lag gets more pertinent by the day.

Click the above image to play video

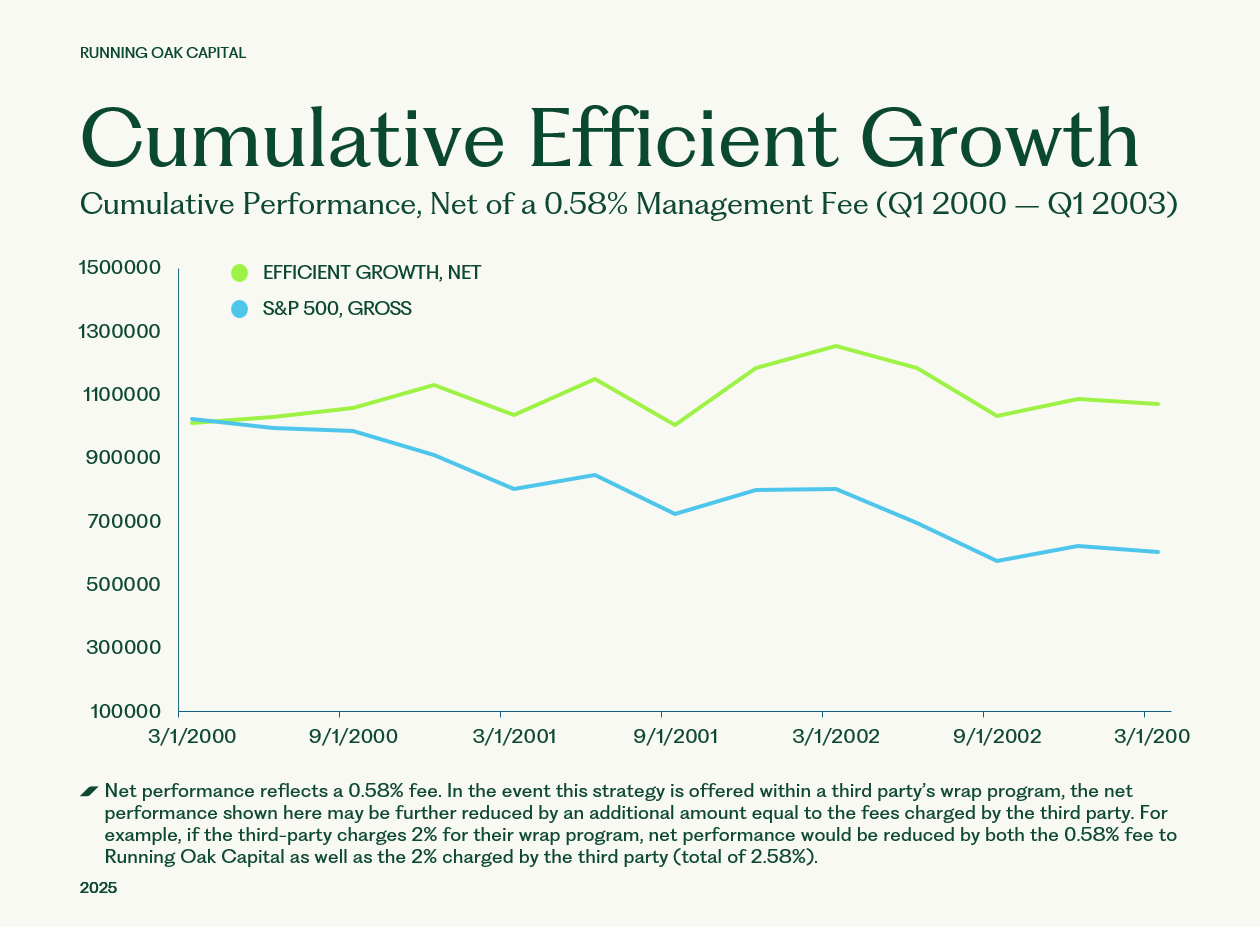

Please find Running Oak's most recent performance and note below. Running Oak's Efficient Growth strategy is an excellent complement to the most popular, most overcrowded, most over-owned, high-flying holdings: S&P 500, QQQ, Mag7, unprofitable/innovative Tech, AI companies that burn cash with no path to profitability, Large Cap Growth, etc. It can be a thankless job, but we welcome the opportunity to be your clients' portfolio designated driver.

“You don’t work in the rain? You’re a mailman! Neither rain, nor sleet,… It’s the first one!” - George Costanza

Efficient Growth appears imminently likely to provide more value than any time since 1999, BECAUSE it's built for the rain. By value, I don’t mean absolute return but outperformance and, most importantly, lower downside. If I am correct (Note: that’s a big if – I’m not ALWAYS correct), here is what that looked like over the 3-year period following 2000:

"Giddy up!" - Kramer

Why NOW appears to be the best time in 26 years:

Starting Point – First, it’s generally been an excellent time, regardless of the time.

On Sale Now! - Everyone knows that chasing returns is a bad idea. But wouldn’t the opposite of a bad idea be a good idea - as opposed to chasing, buying at a discount? Investors are comfortable with and drawn to doing that which hurts them (chasing), but reluctant to do the opposite. What is the opposite of financial pain and underperformance?

Over the last 8 months, High Volatility (proven to destroy value), Meme stocks (YOLO Reddit posts), and Momentum (buying, buying more because others bought, buying even more because others bought even more) have performed better than any other factors. Meanwhile, Low Volatility (proven to provide value), Quality (companies generating earnings that are unlikely to go bankrupt), Profitability (making money), and Forward PEs (companies thar are expected to perform best in the real world) performed the worst.

Buying companies simply because they were pumped on a post? Dumb. Buying excellent companies that make money and are expected to perform well in the next year AT A DISCOUNT? Genius.

“No boxers. No jockeys. The only thing between him and us is a thin layer of gabardine.” - Jerry Seinfeld

Efficient Growth doesn’t have to be THE bet, simply A bet. A diversified portfolio is an aggregate of multiple bets. If built properly, when one bet loses (because investing, like life, is unpredictable) another bet wins.

The typical client portfolio is all-in on 1 outcome: that AI isn’t a bubble.

- 41% of the S&P 500 is invested in a small number of companies.

- Individual investors own the EXACT SAME companies.

- Active Growth managers own the EXACT SAME companies.

The Mag7, S&P 500, Large Cap Growth, QQQ, Russell 1000, etc. is a theater at 1000x max capacity with one exit.

Jerry: “You don’t even know what a [AI] is.”

Kramer: “Yeah, but they do, and they’re the ones [AI’ing]!“

What if AI is a bubble? What if every portfolio is positioned for the market to go straight up…, but it goes straight down? (That’s what happens when bubbles pop.) Every market professional I have spoken to (but two) has candidly stated behind closed doors that we are clearly in a bubble.

Howard Marks’ most recent letter was excellent and informative. Therefore, I share excerpts below. I highly recommend the letter in its entirety.

“Here’s some historical perspective from a recent article in Wired:

AI’s closest historical analogue here may be not electric lighting but radio. When RCA started broadcasting in 1919, it was immediately clear that it had a powerful information technology on its hands. But less clear was how that would translate into business. “Would radio be loss-leading marketing for department stores? A public service for broadcasting Sunday sermons? An ad-supported medium for entertainment?” [Brent Goldfarb and David A. Kirsch of the University of Maryland] write. “All were possible. All were subjects of technological narratives.” As a result, radio turned into one of the biggest bubbles in history – peaking in 1929, before losing 97 percent of its value in the crash. This wasn’t an incidental sector; RCA was, along with Ford Motor Company, the most high-traded stock on the market. It was, as The New Yorker recently wrote, “the Nvidia of its day.” . . .

In 1927, Charles Lindbergh flew the first solo nonstop transatlantic flight from New York to Paris... It was the biggest tech demo of the day, and it became an enormous, ChatGPT-launch-level coordinating event – a signal to investors to pour money into the industry.

“Expert investors appreciated correctly the importance of airplanes and air travel,” Goldfarb and Kirsch write, but “the narrative of inevitability largely drowned out their caution. Technological uncertainty was framed as opportunity, not risk. The market overestimated how quickly the industry would achieve technological viability and profitability.”

As a result, the bubble burst in 1929 – from its peak in May, aviation stocks dropped 96 percent by May 1932...”

(Note that both radio and air travel have continued to play significant roles in society. They still dropped 97 and 96%, respectively. More from Howard Marks:)

“It’s worth reiterating that two of the closest analogs AI seems to have in tech bubble history are aviation and broadcast radio. Both were wrapped in high degrees of uncertainty and both were hyped with incredibly powerful coordinating narratives. Both were seized on by pure play companies seeking to capitalize on the new game-changing tech, and both were accessible to the retail investors of the day. Both helped inflate a bubble so big that when it burst, in 1929, it left us with the Great Depression. (“AI Is the Bubble to Burst Them All,” Brian Merchant, Wired, October 27 – emphasis added. N.b., the Depression had many causes beyond the bursting of the radio/aviation bubble.)

Here’s my [Howard Marks’] actual bottom line:

- There’s a consistent history of transformational technologies generating excessive enthusiasm and investment, resulting in more infrastructure than is needed and asset prices that prove to have been too high. The excesses accelerate the adoption of the technology in a way that wouldn’t occur in their absence. The common word for these excesses is “bubbles.”

- AI has the potential to be one of the greatest transformational technologies of all time.

- … AI is currently the subject of great enthusiasm. If that enthusiasm doesn’t produce a bubble conforming to the historical pattern, that will be a first.

- Bubbles created in this process usually end in losses for those who fuel them.

- The losses stem largely from the fact that the technology’s newness renders the extent and timing of its impact unpredictable. This in turn makes it easy to judge companies too positively amid all the enthusiasm and difficult to know which will emerge as winners when the dust settles.

- There can be no way to participate fully in the potential benefits from the new technology without being exposed to the losses that will arise if the enthusiasm and thus investors’ behavior prove to have been excessive.

- The use of debt in this process – which the high level of uncertainty usually precluded in past technological revolutions – has the potential to magnify all of the above this time.

Since no one can say definitively whether this is a bubble, I’d advise that no one should go all-in without acknowledging that they face the risk of ruin if things go badly. But by the same token, no one should stay all-out and risk missing out on one of the great technological steps forward. A moderate position, applied with selectivity and prudence, seems like the best approach.”

Therefore, invest in the Mag7. Invest in the S&P 500, QQQ, Large Cap Growth strategies, Nvidia, Alphabet, Microsoft, etc. But don’t invest too much, and complement with uncorrelated investments, like Efficient Growth. With an active share of 97%, Efficient Growth provides very different exposure to that which most currently own far too much of. Don’t flirt with financial disaster. You know what happens when you tempt financial disaster? It tends to eventually happen.

Here is why this all matters RIGHT NOW.

"You know what they say: You don't sell the steak; you sell the sizzle." - Kramer

All of the above depends upon one thing: Nvidia. Nvidia is THE lynchpin, the sizzle, in the argument for why we’re currently not in a bubble.

According to some sources, 83% of the chips sold by Nvidia last year are currently not in use. $140,000,000,000 worth of chips sold just last year are sitting around, collecting dust. Meanwhile, Nvidia just announced they are releasing their new chip, Rubin. Thus, 140 billion dollars of chips sold in the last several months - that aren't being used yet - are soon to be NOT state of the art.

The argument that we’re not in a bubble is Nvidia’s forward PE of 24. Its current PE is 46, meaning Nvidia is expected to roughly double earnings this year. That also means almost 250% the dollar amount of chips that have yet to be used from just last year, that are sitting around collecting dust, that will be NOT cutting edge shortly are going to be bought within the next 12 months… for what exactly? To not be used also? 83% of the chips bought last year aren’t being used. 250% that amount are going to be bought this year?

Chips require data centers. Data centers are seemingly announced by the day AND delayed by the day. In fact, Bernie Sanders and Ron DeSantis are now in perfect agreement on something: that data centers are problematic. Are people all over the country going to be fine as electricity costs double and their taps run dry? If they aren’t, if Ron DeSantis, Bernie Sanders and everyone in between agree, it’s going to be a much longer road for data center builds, meaning a much longer road for Nvidia to sell 250% the chips that have yet to be used from last year.

Let’s say Nvidia sells an obscene amount of chips, $100B in chips. That would make Nvidia’s PE roughly 80. Despite negative growth, were Nvidia to trade at 2x the long term PE of the market (32), that would entail a 60% decline. As George might explain such shrinkage, "I WAS IN THE POOL! I WAS IN THE POOL!" What if Nvidia sells 3x the chips that it sold last year that are currently actually being used? That would make Nvidia’s PE... 80. There’s that 80, again.

"I don't have a square to spare. I can't spare a square!" - Elaine

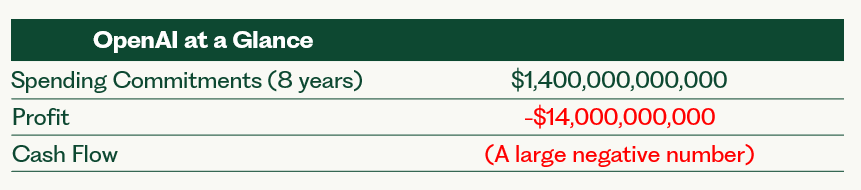

At the heart of the AI hypefest is OpenAI.

OpenAI has committed to spend 1.4 TRILLION dollars over the next 8 years when... ummm… OpenAI doesn’t make money. Actually, it loses money - a lot of money. How does a company that loses money day in and day out spend more money than pretty much any company in the history of the world has ever spent?

OpenAI is growing revenue at a high rate. Maybe OpenAI manages to grow to profitability, despite currently having negative gross margins (it loses more money the more revenue it generates). But what if it doesn't? What if Nvidia customers decide that ever-growing large piles of wildly expensive chips sitting around collecting dust doesn't make financial sense? In speculative bubbles, investors lose sight of the "what if's"; I'm attempting to combat that.

AI is real. AI will be transformative. But will it deliver on the prophecies of Elon Musk - the end of poverty, living on Mars, flying cars - in time for investors? Well, he said the last two would happen in... [checks the records]... [does a quick double-check]... 2026. Oof, we had better get on it. We don't have to go too far back for an analog. Only a few years ago, Meta invested heavily but didn't see a return on that investment soon enough for the market. Here's how that played out:

And now... "The tradition of Festivus begins with the Airing of Grievances. I got a lot of problems with you people! And now you're gonna hear about it!" - Frank

"Another Festivus Miracle!"

"I find tinsel distracting." - Note that gold and silver (#11) are up massively. Historically, when gold flies, it ain't good.

"You dipped the chip. You took a bite. And you dipped again. That's like putting your whole mouth right in the dip!" - Timmy

“When people panic, they make mistakes. They override systems. They disregard procedures, ignore rules. They deviate from the plan.” - The Obstacle Is the Way

I admit this begrudgingly: a financial plan is more important than investments; always begin with the end in mind. Did the financial plan assume almost an 18% return in the S&P 500 since 2019? Or did it assume a typical 10% return? If 10%, what is the plan for the extra 100%? To let it ride, risking it at 4x the risk of peak of the Tech Bubble, or to take it off the table, investing it in a conservative alternative, because the client is far ahead of the plan? If it's still riding at historically obscene risk, don't panic due to FOMO. Don't make mistakes. Don't override the system. Don't disregard procedures, ignore rules. Don't deviate from your well-thought out plan.

Why Invest in Efficient Growth:

- Opportune: A little known - yet very large - hole exists in the typical equity portfolio, precisely where the most attractive risk/reward asymmetry currently lies. Efficient Growth fills that hole - and opportunity - like few portfolios do.

- 5 Stars: Efficient Growth has a 5-Star Morningstar rating.

- Since inception, Efficient Growth has provided 14% more return than the S&P 500 Equal Weight Index, given the same level of downside risk, gross of fees. (Ulcer Performance Index)*

Differentiated Approach and Construction

- Mid Cap stocks are at their cheapest in 25 years relative to Large. Efficient Growth provides significant Mid Cap exposure.

- Efficient Growth is built upon 3 longstanding, common sense principles: maximize earnings growth, strictly avoid inflated valuations, protect to the downside.

- Running Oak utilizes a highly disciplined, rules-based process, resulting in a portfolio that is reliable, repeatable, and unemotional.

How to Invest

- Efficient Growth is currently available as an SMA and ETF. (ETF specifics and SMA historical performance can't be shared in the same letter - sorry, it's annoying, I know. Please inquire for the ticker or more information.)

- In just over 2 years, The ETF Which Shall Not Be Named has grown almost 20,000% since launch - from 2 to 390mm.

Performance Update

- Running Oak’s Efficient Growth portfolio was up 2.83%, gross of fees (2.31%, net), in 2025.*

Quick hitters:

Consistently Not Stupid - Running Oak in 3 Words

Invest Where Others Aren't (MARGE - Upper Mid/Lower Large Cap)

- Investing where everyone else is investing means higher prices, higher valuations, lower implied returns, higher implied downside.

- Investing where others aren't means lower prices, lower valuations, higher implied returns, lower implied downside and a margin of error.

- Investing where others aren't also provides valuable diversification.

- If the market goes up, others are likely to follow, propelling prices.

- If the market goes down, others can't sell what they don't own, meaning less selling and downside pressure.

It's win/win.

Running Oak's goal is to maximize the exponential growth of clients' portfolios, while subjecting them to far less risk of loss. In other words, we aim to help your clients realize their dreams and avoid their nightmares.

If you appreciate critical thinking, math, common sense, and occasional sarcasm, we would love to speak with you. Please feel free to set up a time here: Schedule a call.

Happy Festivus for the rest of us!

Seth L. Cogswell

Founder and Managing Partner

Edina, MN 55424

P +1 919.656.3712

For additional data and context regarding the claims made within this letter, please refer to the Disclosures and Additional Data document located here.

Investment Advisory Services are offered through Running Oak Capital, a registered investment adviser.

The opinions voiced in this material are those of Running Oak Capital’s, do not constitute investment advice, and are not intended as recommendations for any individual. To determine which investments and strategies may be appropriate for you, consult with us at Running Oak Capital or another trusted investment adviser.

*Past performance is no guarantee of future results. Performance expectations are no guarantee of future results; they reflect educated guesses that may or may not come to fruition. All indices are unmanaged and may not be invested into directly.

*Returns prior to September of 2013, while unaudited, were documented and generated on a real-time (not back-tested) basis. Such results are from accounts managed at other entities prior to the formation of Running Oak Capital. It reflects the strategy’s performance since the beginning of 1989. Downside risk is calculated by dividing the average drawdown of the strategy, observed on a quarterly basis, by the average drawdown of the S&P 500 index since 1989.

*Statements regarding the large gap in the middle of the typical equity allocation reflect the opinion of Running Oak Capital This is based on informal feedback and experience from interactions with investors and other financial professionals. Further, statements on where the most attractive risk/reward asymmetry lie, although based on observable data, reflect the opinion of Running Oak Capital.

*Statement regarding Mid Cap stocks outperforming Large is reflective of historical performance of the Russel Midcap Index vs Russell 1000 Index.

*Source of Mid Cap undervaluation & Large Cap overvaluation: Bloomberg

Latest articles

This data feed is not available at this time.

Data is currently not available