PayPal Holdings PYPL’s Buy Now, Pay Later (BNPL) offering continues to stand out as a key growth driver within its branded checkout ecosystem. In the second quarter of 2025, BNPL total payment volume rose more than 20% year over year, while monthly active accounts expanded 18%. The solution is now available in nine global markets and is automatically integrated wherever PayPal is accepted, providing unmatched distribution without additional merchant integration costs. This scale advantage positions PayPal as the most broadly available BNPL provider in its largest markets.

The economics of BNPL are also attractive. PayPal disclosed that transactions completed with BNPL result in average order values more than 80% higher than standard branded checkout. This lifts merchant sales and creates incremental revenue opportunities. Retailers who highlight BNPL at the product page level, such as Ace Hardware, have reported a 35% increase in PayPal sales and a sevenfold increase in order size, demonstrating the strong conversion potential of the product.

Beyond e-commerce, PayPal is extending BNPL into omnichannel. Its “Pay Later To Go” product, launched in Germany, enables installment payments in physical stores across multiple durations. This expansion reinforces PayPal’s ambition to capture everyday spending, not just online discretionary purchases, and adds a competitive edge as BNPL moves closer to mainstream credit alternatives.

Still, risks remain. Standalone BNPL providers are innovating aggressively, while Apple’s entry raises competitive intensity. Additionally, a weaker consumer backdrop could weigh on repayment trends and dampen growth.

PayPal’s BNPL strategy offers meaningful upside through scale, integration, and merchant value creation, but competition and credit risks warrant ongoing investor attention.

How Are Block and Affirm Doing in the BNPL Space?

Block XYZ continues expanding its BNPL capabilities via Afterpay, integrating installment options directly into Cash App and retroactively for past purchases. In second-quarter 2025, its BNPL Gross Merchandise Value (GMV) grew 17% year over year to $9.11 billion, while Cash App’s gross profit per active user rose 15%. Notably, 96% of installments were paid on time, and 98% incurred no late fees. Moreover, more than 95% of Afterpay GMV came from returning customers.

Affirm Holdings, Inc. AFRM noted that in the last reported quarter, most of the transactions came from repeat transactions. It showcases the trust and loyalty of its customers. In the third quarter of fiscal 2025, total transactions rose 45.6% year over year to 31.3 million on the back of a 94% repeat rate. It has recently expanded its partnership with Stripe to become the first BNPL provider to be directly integrated into Stripe Terminal, the point-of-sale (POS) system used by more than a million in-store locations across the United States and Canada. This means shoppers paying in physical stores through Stripe’s POS devices can now choose Affirm at checkout.

PYPL’s Price Performance, Valuation and Estimates

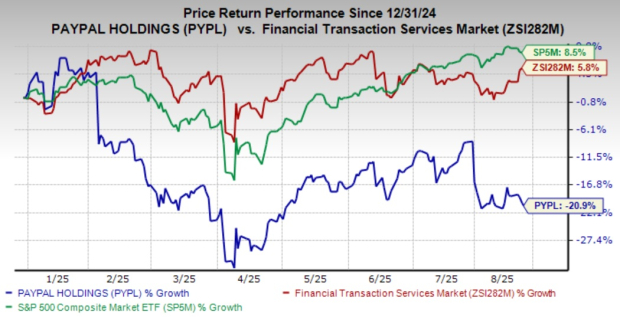

Shares of PayPal have plunged 20.9% year to date, underperforming both the broader industry and the S&P 500 Index.

Image Source: Zacks Investment Research

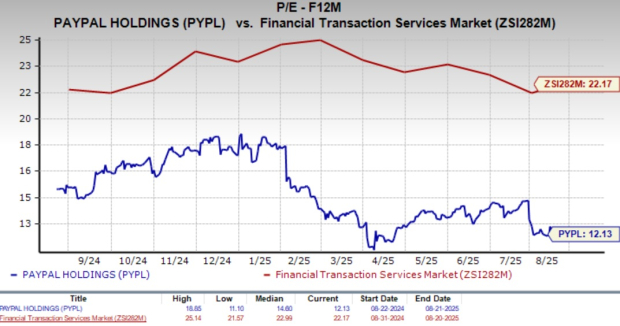

From a valuation standpoint, PayPal shares are trading cheap, as suggested by the Value Score of A. In terms of forward 12-month P/E, PYPL stock is trading at 12.13X compared with the Zacks Financial Transaction Services industry’s 22.17X.

Image Source: Zacks Investment Research

PayPal’s estimate revisions reflect a positive trend. The Zacks Consensus Estimate for 2025 earnings is pegged at $5.22 per share, suggesting 12.3% growth over 2024, while the same for 2026 stands at $5.77, calling for 10.5% growth year over year.

Image Source: Zacks Investment Research

At present, PayPal carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpPayPal Holdings, Inc. (PYPL) : Free Stock Analysis Report

Affirm Holdings, Inc. (AFRM) : Free Stock Analysis Report

Block, Inc. (XYZ) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.