The advancement in mobile technology, such as 4G and 5G networks, and the proliferation of bandwidth-intensive applications have driven growth in mobile data usage globally. Also, the rampant usage of network-intensive applications for video conferencing and cloud services has fueled the rise. This has led to greater capital spending by wireless carriers to meet this incremental demand, aiding the demand for tower REITs like SBA Communications’ SBAC wireless communication infrastructure.

The company has a resilient and stable site-leasing business model as it generates most of its revenues from long-term (typically five to 10 years) tower leases with built-in rent escalators. This assures stable site-leasing revenues for SBA Communication. In the second quarter of 2023, 89% of the total incremental domestic leasing revenues came from the big four carriers — AT&T, Inc. T, T-Mobile TMUS, Verizon VZ and Dish.

Moreover, in late July 2023, SBAC signed a new five-year master lease agreement with AT&T. The deal will help AT&T deploy 5G and other advanced technologies by leveraging SBA Communications’ vast U.S. tower portfolio, benefiting both companies. We expect 2023 site-leasing revenues to increase 7.1% year over year.

SBA Communications’ portfolio expansion efforts into select international markets with high growth characteristics position it well to take advantage of secular trends in mobile data usage and wireless spending growth worldwide. In the second quarter of 2023, the company acquired nine communication sites for a total cash consideration of $7.2 million. It also built 64 towers during this period.

Subsequent to the end of the second quarter, SBAC purchased or is under contract to buy 134 communication sites for a total consideration of $72.9 million in cash. It expects to conclude these buyouts by the end of this year.

On the balance sheet front, SBA Communications exited second-quarter 2023 with $273.6 million of cash and cash equivalents, short-term restricted cash and short-term investments. Also, in the second quarter, its net debt-to-annualized adjusted EBITDA improved sequentially to 6.6X from 6.9X.

With ample financial flexibility, SBAC is well-poised to capitalize on future growth opportunities. Also, the company’s current cash flow growth is projected at 14.77% compared with the industry’s average of 9.37%.

Solid dividend payouts are arguably the biggest enticements for REIT shareholders, and SBA Communications has remained committed to that. Moreover, it has increased its dividend four times in the last five years, and the five-year annualized dividend growth rate is 24.19%. Such efforts enhance shareholders’ wealth and boost investors’ confidence in the stock. Check SBA Communications’ dividend history here.

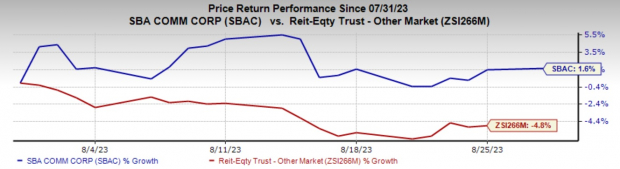

This Zacks Rank #3 (Hold) stock has risen 1.6% in the past month against the industry’s decline of 4.8%. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Image Source: Zacks Investment Research

However, the company has a high customer concentration, and in the second quarter of 2023, T-Mobile, AT&T and Verizon accounted for 40.7%, 28.0% and 19.9%, respectively, of SBAC’s domestic site-leasing revenues. A loss of any of these customers or consolidation among them or a reduction in network spending will lead to a significant material impact on the company’s top line.

For 2023, management expects the churn arising from the Sprint-related decommissioning on the domestic front to be at the high end of its projected range of $25-$30 million. Moreover, the Sprint-related churn is estimated between $20 million and $30 million in 2024, and $35 million and $45 million in 2025. Further, it anticipates the international churn to remain elevated, in line with its expectations and the outlook stated earlier. Amid this, we estimate total revenues to exhibit modest year-over-year growth of 3.1% in 2023.

SBA Communications has a substantially leveraged balance sheet, with $12.7 billion of total debt and net debt to the annualized adjusted EBITDA leverage of 6.6X as of the end of the second quarter of 2023. Further, a high-interest-rate environment is likely to result in high borrowing costs for the company, affecting its ability to purchase or develop real estate.

For 2023, our estimate for interest expenses indicates a rise of 12.5% year over year. Further, with high interest rates, the dividend payout might become less attractive than the yields on fixed-income and money-market accounts.

Note: Anything related to earnings presented in this write-up represent funds from operations (FFO) — a widely used metric to gauge the performance of REITs.

Zacks Names #1 Semiconductor Stock

It's only 1/9,000th the size of NVIDIA which skyrocketed more than +800% since we recommended it. NVIDIA is still strong, but our new top chip stock has much more room to boom.

With strong earnings growth and an expanding customer base, it's positioned to feed the rampant demand for Artificial Intelligence, Machine Learning, and Internet of Things. Global semiconductor manufacturing is projected to explode from $452 billion in 2021 to $803 billion by 2028.

See This Stock Now for Free >>AT&T Inc. (T) : Free Stock Analysis Report

Verizon Communications Inc. (VZ) : Free Stock Analysis Report

SBA Communications Corporation (SBAC) : Free Stock Analysis Report

T-Mobile US, Inc. (TMUS) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.