Sandisk SNDK has delivered a stunning run. SNDK shares have surged 206.1% over the past three months and 1,194.2% over the past year, significantly higher than gains in the broader Zacks Computer and Technology sector and the Zacks Computer-Storage Devices industry over the same periods.

Sandisk shares have also outperformed peers, including Western Digital WDC, Silicon Motion Technology SIMO and Seagate STX in the trailing 12-month period. Shares of Western Digital, Silicon Motion Technology and Seagate have returned 529.7%, 342% and 131.6%, respectively.

SNDK Stock’s Performance

Image Source: Zacks Investment Research

However, the ongoing acceleration in SNDK shares is forcing investors to rethink timing. When a stock moves this far this fast, the next question becomes less about whether the story is real and more about what is already priced in.

What keeps SNDK on the radar is that the operating backdrop is also shifting. AI-driven storage demand is pushing NAND market conditions in a direction that supports firmer pricing and a richer product mix.

SNDK Offers Positive Q3 Guidance

For the third quarter of fiscal 2026, Sandisk guides revenues between $4.4 billion and $4.8 billion. Management also expects the market to be more undersupplied than in the fiscal second quarter.

Profitability expectations are even more notable. Gross margin is projected at 65% to 67%, and non-GAAP operating expenses are expected to normalize between $450 million and $470 million. Non-GAAP earnings are expected between $12.00 and $14.00 per share.

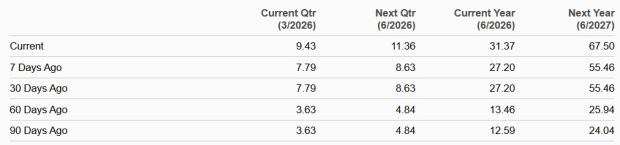

Consensus Estimate Trend

Image Source: Zacks Investment Research

The operational driver management emphasizes is the enterprise solid-state drive (SSD) ramp. Enterprise SSD revenue jumped 64% sequentially in the second quarter of fiscal 2026. Sandisk expects a substantial sequential step-up again in the third quarter, with further acceleration anticipated in the second half.

Sandisk’s Capital Discipline Bodes Well for Investors

Financial flexibility has improved alongside the operating results. Sandisk ended the fiscal second quarter with a cash balance of about $1.5 billion and delivered $843 million in adjusted free cash flow in the reported quarter. Operating cash flow was $1.019 billion.

Debt was reduced to roughly $603 million at the fiscal second quarter-end from about $2 billion previously, and management aims to continue deleveraging. That balance sheet progress matters because it supports reinvestment in the BiCS8 transition and an expanding enterprise solid-state drive portfolio.

Sandisk is also emphasizing disciplined supply and steady capital spending, anchored by mid- to high-teens annual bit growth through the BiCS8 transition. Early multiyear agreements with prepayments are part of the commercial model shift intended to improve planning visibility.

Sandisk Shares Are Overvalued

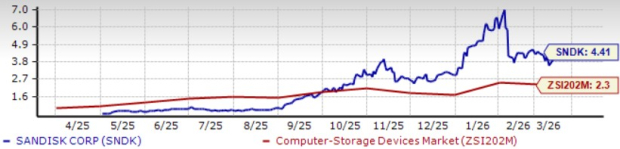

Valuation is the next pressure point after a run like this. Sandisk trades at about 4.41X forward 12-month sales versus 2.3X for the industry. The stock is overvalued, as suggested by a Value Score of F.

The practical takeaway is that the margin for error narrows when the multiple sits near the high end of the company’s one-year range. SNDK has traded as high as 7.04X and as low as 0.54X on forward sales, so execution timing and order flow can outweigh long-cycle potential in the near term.

SNDK’s Valuation

Image Source: Zacks Investment Research

Sandisk’s P/S multiple is lower than Western Digital’s 6.21X and Seagate’s 6.4X, but higher than Silicon Motion Technology’s multiple of 3.22.

Here’s Why SNDK is a Buy Now

The current framework is straightforward for investors scanning Sandisk. AI-led demand is supporting firmer pricing across segments, while the mix is shifting toward higher-margin data center solid-state drives. Management also expects demand to remain above supply beyond calendar 2026, pointing to a structurally stronger profitability profile over time.

With a Zacks Rank #1 and a Growth score of A, Sandisk has a favorable combination that implies a strong investment opportunity. You can see the complete list of today’s Zacks #1 Rank stocks here.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWestern Digital Corporation (WDC) : Free Stock Analysis Report

Seagate Technology Holdings PLC (STX) : Free Stock Analysis Report

Sandisk Corporation (SNDK) : Free Stock Analysis Report

Silicon Motion Technology Corporation (SIMO) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.