Sandisk SNDK is gaining strong traction in the data center market, with growth increasingly driven by AI-related workloads and hyperscaler demand. As enterprises and hyperscalers expand AI systems, demand for high-performance, low-latency flash storage is rising. Sandisk's expanding presence in this segment, supported by next-generation PCIe Gen5 drives and the forthcoming BiCS8 QLC Stargate solution, is driving a clear shift in its revenue mix toward higher-value data center deployments. This signals a structural pivot beyond traditional end markets.

The importance of this ramp-up lies in the evolving nature of NAND demand, as AI workloads such as inference, KV cache and RAG are driving increasing requirements for high-performance, low-latency flash storage. The company stated that these workloads require systems to store context, intermediate data and large external datasets, positioning NAND as a critical component of AI infrastructure and supporting more durable demand trends.

Sandisk highlighted strong demand for its TLC-based enterprise SSD portfolio, which supports performance-intensive compute workloads, wherein speed and latency are critical. The company also said it expects to begin shipping its QLC “Stargate” solutions for revenues in the fiscal fourth quarter, expanding its portfolio with higher-density storage offerings aimed at AI infrastructure deployments.

It is noteworthy that TLC and QLC products serve complementary roles across AI workloads, enabling Sandisk to address high-performance and high-capacity storage requirements. The company further noted that expanding customer engagements and multi-year supply agreements are strengthening long-term relationships with hyperscalers and enterprise customers as AI infrastructure investments continue to accelerate.

The impact is visible in Sandisk’s fiscal third-quarter revenues of $5.95 billion, which surged 251% year over year and exceeded the company’s guidance, driven by higher pricing and a mix shift toward higher-value customers. Data center revenues soared 233% sequentially to $1.47 billion, supported by strong demand for TLC-based enterprise SSDs powering AI-driven workloads. It is noteworthy that inference, KV cache and RAG workloads are significantly increasing the need for high-performance NAND storage.

Sandisk also expects its QLC Stargate solutions to begin contributing revenues in the fiscal fourth quarter, adding another layer of growth. With AI infrastructure demand accelerating and customers entering multi-year supply agreements, backed by financial guarantees, management believes the business is becoming more predictable, structurally stronger and less cyclical.

SNDK Faces Stiff Competition

SNDK faces stiff competition as peers also target the AI-driven data center storage opportunity.

Seagate Technology STX remains heavily focused on the data-center market, which accounted for 88% of exabyte shipments and 80% of revenues in the third quarter of fiscal 2026, supported by strong cloud and AI demand. The company is benefiting from its HAMR-based Mozaic platform and high-capacity nearline drives, which improve cost-per-terabyte and power efficiency. Seagate also saw steady growth in the edge and IoT markets, which contributed about $612 million, or 20% of quarterly revenues.

Micron Technology MU presents another challenge, with a growing enterprise SSD portfolio and a diversified memory franchise, including HBM. The company benefits from additional AI infrastructure leverage, though its NAND segment is one part of a larger memory business, unlike SNDK's pure-play focus.

SNDK’s Share Price Performance, Valuation & Estimates

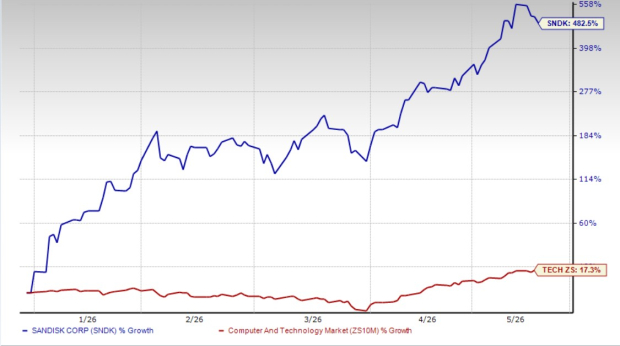

Sandisk’s shares have skyrocketed 482.5% in the year-to-date period, outperforming the broader Zacks Computer and Technology sector’s return of 17.3%.

SNDK Stock Outperforms Sector

Image Source: Zacks Investment Research

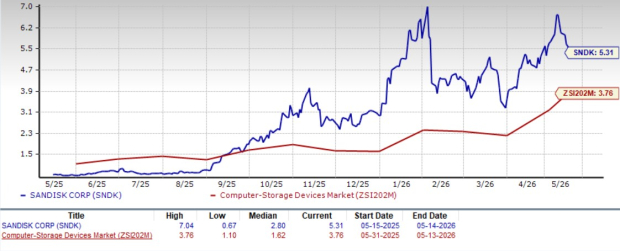

SNDK stock is trading at a forward 12-month price/sales of 5.31X compared with the Zacks Computer-Storage Devices’ 3.76X. Sandisk has a Value Score of F.

SNDK’s Valuation

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for fiscal 2026 earnings is pegged at $65.12 per share, up 56.5% over the past 30 days. Sandisk reported earnings of $2.99 per share in fiscal 2025.

Sandisk Corporation Price and Consensus

Sandisk Corporation price-consensus-chart | Sandisk Corporation Quote

Sandisk currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpSeagate Technology Holdings PLC (STX) : Free Stock Analysis Report

Micron Technology, Inc. (MU) : Free Stock Analysis Report

Sandisk Corporation (SNDK) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.