Ross Stores, Inc. ROST is likely to post year-over-year growth in top and bottom lines when it reports first-quarter fiscal 2026 results on May 21, after market close. The Zacks Consensus Estimate for quarterly revenues is pegged at $5.5 billion, indicating a rise of 11.2% from the year-ago quarter’s figure.

The consensus estimate for earnings is pegged at $1.66 per share, up 12.9% from $1.47 earned in the year-earlier period. The consensus mark has increased by a penny in the past seven days.

Ross Stores, Inc. Price, Consensus and EPS Surprise

Ross Stores, Inc. price-consensus-eps-surprise-chart | Ross Stores, Inc. Quote

ROST has a trailing four-quarter earnings surprise of 6.2%, on average. In the last reported quarter, the company posted an earnings surprise of 6.4%.

Factors Likely to Influence ROST’s Q1 Results

Ross Stores’ first-quarter fiscal 2026 performance is expected to have been supported by continued strength in customer traffic, improved merchandise assortments and healthy execution across its stores and supply chain. The company entered the quarter with strong momentum following an impressive holiday season, as its off-price model continued to resonate with value-focused shoppers. Management also noted that better marketing campaigns and operational enhancements, including improved store recovery and faster checkout, have helped deepen customer engagement and support higher transaction volumes.

Several business drivers are likely to have supported first-quarter results. Ross Stores has benefited from broad-based strength across key merchandise categories, with continued momentum in Ladies, shoes, cosmetics and improving trends in home. Inventory levels remain well positioned, giving the company flexibility to chase demand and capitalize on favorable buying opportunities in the marketplace. Additionally, the success of recent marketing initiatives and strong new-store productivity should have contributed to higher traffic and market share gains as consumers increasingly shift spending toward off-price retailers.

On the last quarter’searnings call management cited macroeconomic uncertainties but emphasized that sales trends were broad-based across geographies and income cohorts, indicating steady engagement from its core low-to-moderate-income customer base despite external pressures.

As a result, ROST anticipated comparable sales (comps) growth of 7-8% for the first quarter of fiscal 2026. The company forecasts total sales to increase 10-12% year over year. Operating margin is expected to be 11.8-12.1%. Earnings per share are projected in the range of $1.60 to $1.67. The company plans to open 17 new stores during the quarter, including 13 Ross Dress for Less locations and four dd’s DISCOUNTS stores. Our model projects comps growth of 7% in the fiscal first quarter.

However, Ross Stores has remained cautious regarding the broader macroeconomic environment, noting that uncertainty around consumer spending and global trade conditions could create volatility in demand. Management highlighted that tariffs were a meaningful headwind during fiscal 2025, particularly in the home category, and noted that higher duties on China-sourced goods increased merchandise costs. While Ross Stores has made progress in recapturing some of these pressures through better buying and merchandising strategies, evolving trade policies and other macro uncertainties remain factors the company is monitoring closely.

What the Zacks Model Unveils for ROST Stock

Our proven model conclusively predicts an earnings beat for Ross Stores this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat, which is exactly the case here.

Ross Stores currently has an Earnings ESP of +4.17% and a Zacks Rank of 2. You can uncover the best stocks before they’re reported with our Earnings ESP Filter.

ROST’s Stock Price Performance & Valuation Picture

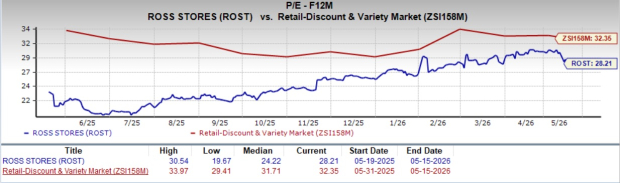

From a valuation perspective, Ross Stores is trading at a discount relative to industry benchmarks. The company has a forward 12-month price-to-earnings of 28.21X, lower than the Retail-Discount Stores industry’s average of 32.35X.

Image Source: Zacks Investment Research

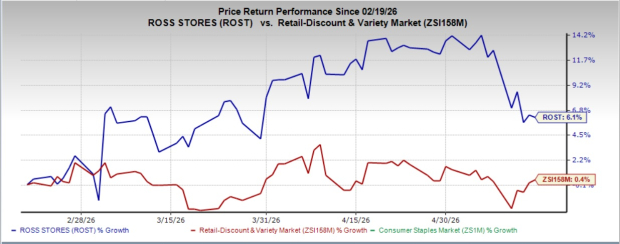

The recent market movements show that ROST’s shares have gained 6.1% in the past three months compared with the industry's 0.4% rise.

Image Source: Zacks Investment Research

Other Stocks With the Favorable Combination

Here are three other companies, which, according to our model, have the right combination of elements to post an earnings beat this season:

Casey's General Stores CASY currently has an Earnings ESP of +1.02% and a Zacks Rank of 2. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Casey's upcoming quarter’s EPS is pegged at $3.44, which implies 30.8% growth year over year. The consensus estimate for the quarterly revenues is pinned at $4.33 billion, which indicates 8.4% growth from the figure reported in the prior-year quarter. CASY delivered a trailing four-quarter earnings surprise of 20%, on average.

Lowe's Companies LOW currently has an Earnings ESP of +0.57% and a Zacks Rank #3. The consensus estimate for quarterly revenues is pegged at $22.91 billion, which indicates an increase of 9.5% from the figure reported in the prior-year quarter.

The Zacks Consensus Estimate for Lowe's Companies’ upcoming quarter’s earnings per share is pegged at $2.96, implying a 1.4% year-over-year decline. LOW delivered a trailing four-quarter earnings surprise of 2.1%, on average.

Costco Wholesale Corporation COST currently has an Earnings ESP of +0.82% and a Zacks Rank of 3. The Zacks Consensus Estimate for its upcoming quarter’s revenues is pegged at $69.36 billion, indicating a 9.7% rise from the figure reported in the prior-year quarter.

The consensus estimate for Costco’s earnings is pegged at $4.91 per share, implying 14.7% growth from the year-ago quarter. COST delivered a trailing four-quarter earnings surprise of 1.1%, on average.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.9% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>Lowe's Companies, Inc. (LOW) : Free Stock Analysis Report

Costco Wholesale Corporation (COST) : Free Stock Analysis Report

Ross Stores, Inc. (ROST) : Free Stock Analysis Report

Casey's General Stores, Inc. (CASY) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.