Carnival Corporation & plc’s CCL latestearnings callhighlights a potential inflection point in its long-term profitability. Management reported return on invested capital (“ROIC”) above 13% in fiscal 2025, the highest level in nearly two decades, reflecting not just a cyclical recovery, but structural improvements across the business.

The ROIC expansion has been driven by a powerful mix of pricing discipline and cost control. Yields rose more than 5.5% year over year in 2025, supported by strong close-in demand and higher onboard spending. At the same time, unit costs increased at a slower pace than expected, despite inflation, dry-dock expenses and investments in new destinations. This operating leverage pushed margins sharply higher, lifting operating income per berth to its strongest level in almost 20 years.

Balance sheet repair is another key pillar of the improved return profile. Carnival reduced debt by more than $10 billion from peak levels, achieved an investment-grade leverage ratio and materially lowered interest expense. These steps enhance ROIC by reducing the capital base while increasing net operating profit, a dynamic that is expected to persist into 2026 as refinancing benefits are realized.

Looking ahead, management expects continued same-ship yield growth, stable demand across geographies and disciplined capital allocation, including dividends and selective reinvestment. While macro risks and capacity growth remain watch points, the combination of stronger pricing power, tighter cost management and a healthier balance sheet suggests Carnival may indeed be entering a more durable profitability cycle, one defined less by recovery and more by returns.

How Do CCL’s Peers Compare on Returns and Profitability Momentum?

Among Carnival’s closest competitors, Royal Caribbean Cruises Ltd. RCL stands out for its strong post-pandemic profitability rebound. Royal Caribbean has delivered industry-leading margins, supported by a more premium fleet mix, newer ships and higher onboard revenue per passenger. Its ROIC has improved meaningfully as well, aided by disciplined capacity growth and a focus on yield optimization. However, its capital intensity remains elevated given ongoing newbuild deliveries, which can temper near-term return expansion.

Meanwhile, Norwegian Cruise Line Holdings Ltd. NCLH is earlier in its ROIC recovery curve. While Norwegian has made progress on pricing and cost efficiency, leverage remains higher relative to peers and interest expense continues to weigh on net returns. That contrasts with Carnival’s sharper deleveraging over the past two years.

In this context, Carnival’s 19-year-high ROIC is notable. Unlike peers leaning heavily on new capacity or premium pricing alone, CCL’s improvement reflects a balanced mix of yield growth, cost discipline and balance-sheet repair, key ingredients for a more sustainable profitability cycle.

CCL’s Price Performance, Valuation and Estimates

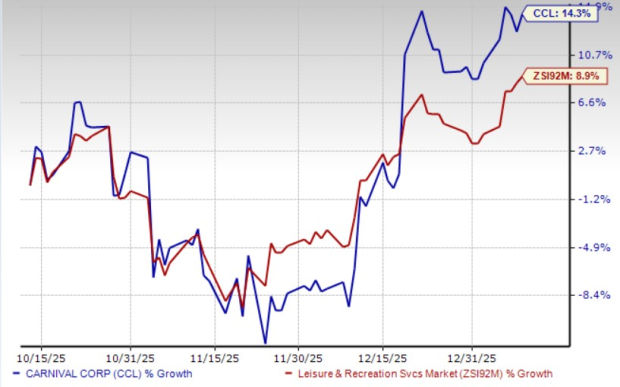

Shares of Carnival have gained 14.3% in the past three months compared with the industry’s rise of 8.9%.

Price Performance

Image Source: Zacks Investment Research

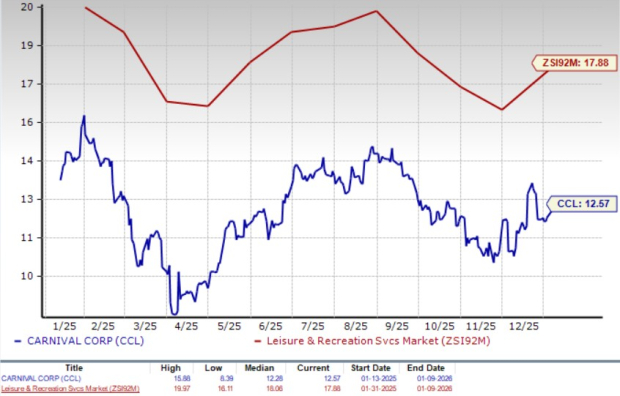

From a valuation standpoint, CCL trades at a forward price-to-earnings ratio of 12.57X, significantly below the industry average of 17.88X.

P/E (F12M)

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for CCL’s 2025 and 2026 earnings implies a year-over-year uptick of 12.4% and 9.1%, respectively. EPS estimates for fiscal 2025 have increased in the past 30 days.

Image Source: Zacks Investment Research

CCL currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the favorite stock to gain +100% or more in the months ahead. They include

Stock #1: A Disruptive Force with Notable Growth and Resilience

Stock #2: Bullish Signs Signaling to Buy the Dip

Stock #3: One of the Most Compelling Investments in the Market

Stock #4: Leader In a Red-Hot Industry Poised for Growth

Stock #5: Modern Omni-Channel Platform Coiled to Spring

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor. While not all picks can be winners, previous recommendations have soared +171%, +209% and +232%.

Download Atomic Opportunity: Nuclear Energy's Comeback free today.Carnival Corporation (CCL) : Free Stock Analysis Report

Royal Caribbean Cruises Ltd. (RCL) : Free Stock Analysis Report

Norwegian Cruise Line Holdings Ltd. (NCLH) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.