Rockwell Automation Inc. ROK is expected to witness declines in both revenues and earnings when it reports third-quarter fiscal 2024 results on Aug 7, before the opening bell.

The Zacks Consensus Estimate for earnings has been unchanged over the past 30 days at $2.11 per share. The consensus mark implies a 30% plunge from the year-ago actual. The consensus estimate for revenues is pegged at $2.02 billion, indicating a 10% year-over-year decline.

Image Source: Zacks Investment Research

Image Source: Zacks Investment Research

Mixed Earnings Surprise History

ROK’s earnings surpassed estimates twice in the trailing four quarters and missed on the remaining two occasions, the average surprise being a negative 1.80%. This is depicted in the following chart.

Image Source: Zacks Investment Research

Factors to Note

The Institute for Supply Management’s manufacturing index registered 48.5% in June 2024, which not only marked a deceleration from 48.7% in May and 49.2% in April, but it also remained below 50%, which indicates contraction. Demand remained subdued as companies refrained from making capital investments. This was evident from the New Orders Index, which also remained below 50 through April-June.

In the fiscal second quarter, the company reported negative 8.1% organic growth. It noted that there had been a buildup of excess inventory among customers, particularly machine builders. It stated that it did not expect a significant acceleration in order levels this fiscal year.

This decrease in order levels is likely to have reflected in Rockwell Automation’s third-quarter top-line performance. This downside is expected to have been offset by favorable pricing. Our model predicts an organic sales decline of 11.8%. This will be offset by a 1.5% contribution from acquisitions and a 0.4% gain from favorable currency impact.

Rockwell Automation has been experiencing increased logistics prices due to higher energy costs and constrained air freight lanes. Also, an increase in spending on talent and growth, unfavorable mix, and currency are expected to have impacted margins.

Segment Expectations

We expect the Intelligent Devices segment’s fiscal third-quarter revenues to be down 1.6% year over year to $953 million. Our prediction for the segment’s operating profit is pinned at $161 million, indicating a year-over-year decrease of 2%.

Our model predicts the Software & Control segment’s sales to be $503 million, suggesting a 33% decline from the prior year’s actual. The segment’s operating profit, which is pinned at $126 million, indicates a 52% plunge from the year-ago quarter’s reported figure.

We expect the Lifecycle Services segment’s sales to be $559 million, implying 7.5% growth from the prior-year period’s actual. The estimate for the segment’s operating profit is $93 million. The figure indicates a 92% surge from the year-ago quarter’s reported figure.

What the Zacks Model Indicates

Our proven model does not conclusively predict an earnings beat for Rockwell Automation this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the chances of an earnings beat.

Earnings ESP: Rockwell Automation has an Earnings ESP of -2.67%. You can uncover the best stocks before they’re reported with our Earnings ESP Filter.

Zacks Rank: The company currently carries a Zacks Rank of 3.

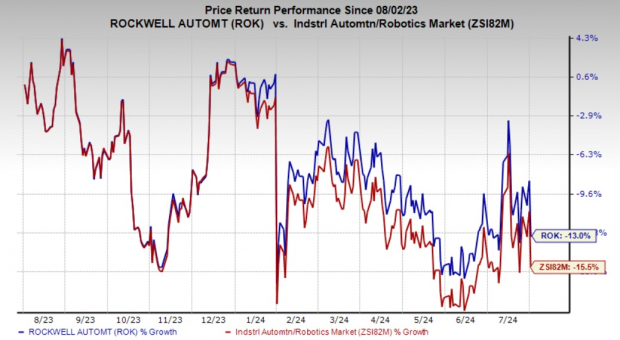

Price Performance

In the past year, Rockwell Automation’s shares have lost 13% compared with the industry’s 15.5% decline.

Image Source: Zacks Investment Research

Stocks to Consider

Here are some companies with the right combination of elements to post an earnings beat in their upcoming releases.

Emerson Electric Co. EMR is scheduled to release its fiscal third-quarter results on Aug 7. It has an Earnings ESP of +0.14% and a Zacks Rank of 2 at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for EMR’s earnings is pegged at $1.42 per share, indicating year-over-year growth of 10.1%. It has a trailing four-quarter average earnings surprise of 10.7%.

Atkore Inc. ATKR is scheduled to release its fiscal third-quarter fiscal results on Aug 6. It has an Earnings ESP of +0.62% and a Zacks Rank of 3 at present.

The Zacks Consensus Estimate for ATKR’s earnings is pegged at $4.03 per share, indicating a year-over-year fall of 29.6%. It has a trailing four-quarter average earnings surprise of 15.4%.

Plug Power PLUG, scheduled to release its second-quarter results on Aug 8, has an Earnings ESP of +1.67% and a Zacks Rank of 3.

The Zacks Consensus Estimate for Plug Power’s earnings is currently pegged at a loss of 30 cents per share, indicating an improvement from the loss of 35 cents per share reported in the year-ago quarter.

Stay on top of upcoming earnings announcements with the Zacks Earnings Calendar.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpEmerson Electric Co. (EMR) : Free Stock Analysis Report

Rockwell Automation, Inc. (ROK) : Free Stock Analysis Report

Plug Power, Inc. (PLUG) : Free Stock Analysis Report

Atkore Inc. (ATKR) : Free Stock Analysis Report

To read this article on Zacks.com click here.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.