A mostly graphical daily curated roundup of the markets and the economy from Nasdaq's IR team.

"The Federal Reserve’s policies are threatening U.S. financial markets and the economy. They are in danger of a steep recession and the risk of a repeat of 1987’s Black Monday...key 10-year bond yield rose steeply from January onward (from 7% in January to 10% by Black Monday in October) and the money supply slowed sharply.

...between July 2022 and August 2023, the M2 supply contracted by 3.9%, the most extreme contraction since 1933."

-John Greenwood and Steve H. Hanke, Another Black Monday May Be Around the Corner

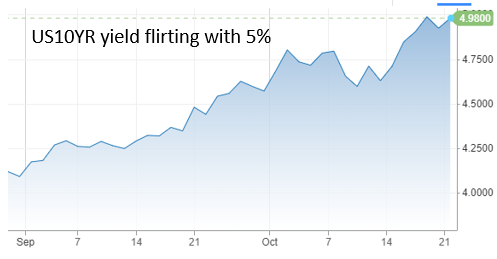

| Dow futures tumble 200 points on Monday as 10YR Treasury yield tops 5%, first time since 2007 -CNBC

* source: CNBC

| Busy week for earnings...39% of the SPX market cap reporting

"data show earnings up 2.2% from a year ago on back of revenue gains of 5.8%. This week another 169 firms are scheduled to report, with 159 the week following" -John Stolzfus, Oppenheimer AM

* source: Piper Sandler

* source: BofA

| Economy: soft-landing, hard-landing, or no-landing?

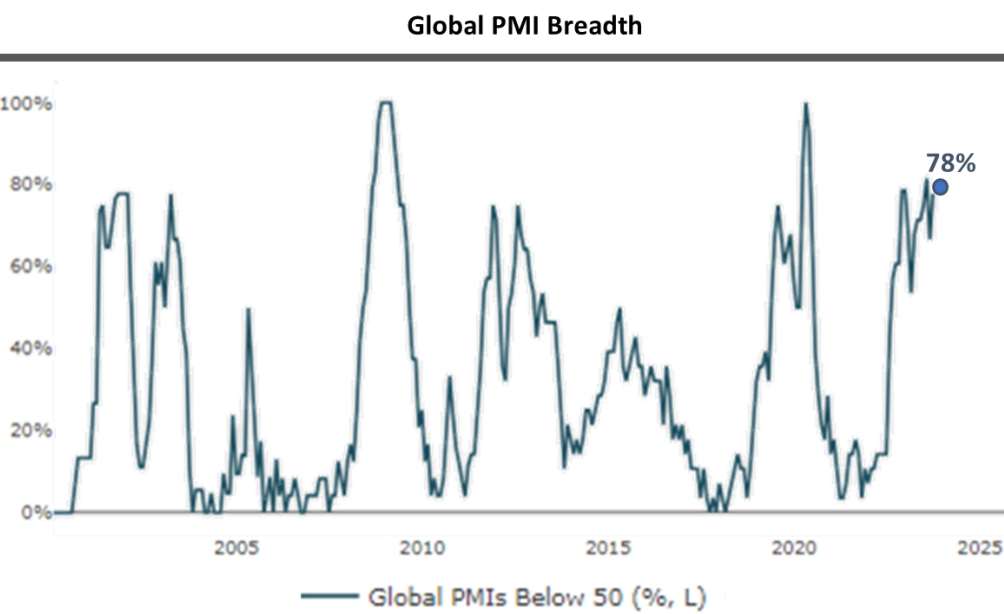

"Investor positioning recently would indicate potential weakness in these early reads on the economy...While the global economy continues to hum along, we continue to see the rate of change slow with 78% of PMIs around the world in contraction territory." -Piper Sandler

* source: Piper Sandler

1) KEY TAKEAWAYS

1) Equities + Dollar + Oil LOWER / TYields HIGHER

| Chevron to buy Hess Corp for $53 billion in second oil mega-merger in weeks

Private equity firms face worst year for exiting investments in a decade -FT

| Next week:

-global flash PMIs on Tuesday will be among the key highlights.

-preliminary US Q3 GDP report + personal income and spending data.

-ECB decision on Thursday

-corporate earnings: focus on Big Tech firms + major oil + healthcare companies.

DJ -0.5% S&P500 -0.5% Nasdaq -0.5% R2K -0.5% Cdn TSX -0.4%

Stoxx Europe 600 -0.5% APAC stocks LOWER, 10YR TYield = 4.974%

Dollar LOWER, Gold $1,973, WTI -1%, $87; Brent -1%, $91, Bitcoin $30,452

| THEMES: yields marching higher | stubborn moderate inflation a risk (CPI +PPI >expected) | where is oil going with geopolitical risks building? | Fedspeak turning dovish | Rising Federal Deficit | Optimism around upcoming Q3 earnings season | Q3 Bank earnings better than expected – will this earnings season be better than expected?

-by Shon Wilk, Nasdaq

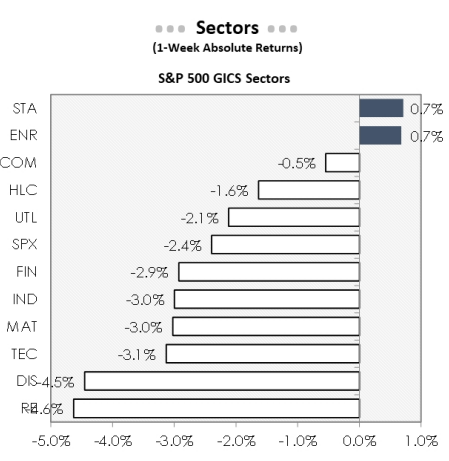

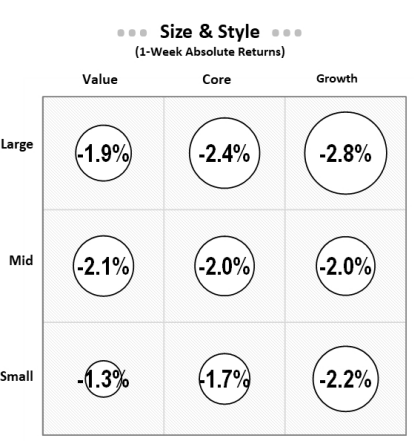

2) Last week: YTD outperformer consumer discretionary top underperformer last week

* source: Factset, produced by Gavin Zaentz

* source: Piper Sandler

3) This week:

-global flash PMIs on Tuesday will be among the key highlights.

-preliminary US Q3 GDP report + personal income and spending data.

-ECB decision on Thursday

-corporate earnings: focus on Big Tech firms + major oil + healthcare companies.

* source: Grindstone Intelligence

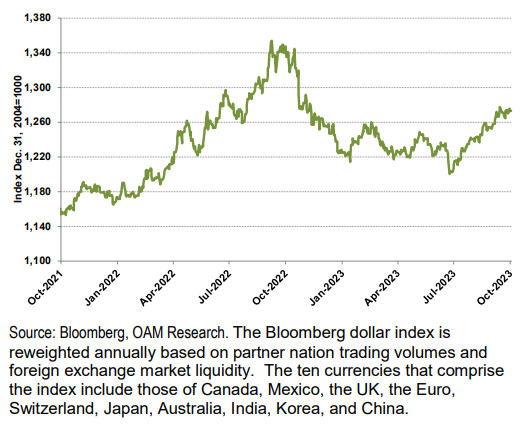

4) Bloomberg Dollar Index near Highs for 2023

* source: John Stolzfus, Oppenheimer AM

2) ESG, COMPILED BY NATHAN GREENE

Asset Managers Are Updating Bond Models to Capture a New Risk - BNN

-A growing number of asset managers are reassessing bond values tied to real assets, as a spike in the frequency of flash floods, fires and storms hits conventional pricing models.

-Mitch Reznick, head of sustainable fixed income at Federated Hermes, says climate risk is a key reason why the investment manager is now underweight real estate credit.

Companies need to integrate climate reporting across functions to comply with California’s new law - Reuters

-California’s new climate disclosure laws, coming into force in 2026, have put companies in the state under pressure to ensure they have clear accountability roles for climate reporting and create cross-functional teams within their finance, legal, and other units. Perhaps the greatest challenge will come in meeting Scope 3 reporting requirements, experts said.

About the author

Massud Ghaussy, CFA, is part of Nasdaq's IR Insights team and delivers daily insights that empowers readers to get a sense of the important issues impacting the day's trading.