Credit: Shutterstock photo

Credit: Shutterstock photoBy Christopher Lackey :

Any Canadian knows about the Tim Hortons brand, because there are a lot of them up here (nearly 3,700), and the chain is treated, for better or worse, something akin to a national religion. The corporate history is perhaps not as well known to the average Canadian. It is worth going over briefly here because the entity Tim is currently listed under (Restaurant Brands International ( QSR )) is a relatively recent creation, so we will partly use its history to establish our thesis.

With the Tim Hortons brand's enormous goodwill and clout that it had built up in Canada since being established in 1966, it was a ripe target for a takeover by a bigger American company (Wendy's ( WEN )), as Canadian companies often are, in 1995. The merger did not last, Tim Hortons' first foray into the US in the early 2000s was unsuccessful and Wendy's spun off the company, making it private again in 2005. Fast forward to 2008 and Tim prepared a new Canadian IPO valued at roughly $25-27 per share. By 2011-2012, the stock had performed well, meandering by then in the $41-52 range, but making the long-term bet on Canada's Tim's habit look like a textbook case for a "KISS" or "Keep it Simple Stupid" investing style. Who couldn't understand the business that everyone and their brother frequented for a daily caffeine/sugar fix?

Things were just getting started for this round of Tim's investors. A Brazilian hedge fund named 3G Capital, notable for partnering with Warren Buffett on deals among other things, had taken over Burger King in the US and made it more profitable by running it with tactics, for which 3G was well known. These included wringing out efficiencies, closing underperforming locations, and relentless cost cutting. In 2014, it completed the buyout of Tim's Canadian listing at over $90 a share, creating a new fast food superpower called Restaurant Brands International. The deal was highly leveraged (which explains the new entity's substantial $10B debt load), and was also a "tax inversion", meaning it figured out that Burger King could pay less tax by moving to Tim Hortons' Oakville, Ontario, corporate office than by being based in the US.

Unlike the old Tim's stock which no longer trades, there is no need to verbally rehash the tale of the tape for QSR's Canadian listing since the IPO approximately 15 months ago as this is public information and is presented right here.

Source: Google Finance

I will note however that this corporate structure is, quite literally, not your grandfather's Tim Hortons and the playbook of the enterprising folks at 3G is well known. The company has a ridiculous book value (-11) and debt load (almost $12B), and has only reported negative earnings while it pays down the debt it took on to fund this merger. Let's not forget the intangible but significant value of the brands (listed at nearly $13B on the balance sheet) is not included in that book value equation. But cash flow almost doubled in the last two quarters, from $508 million to $950 million (Source: Google Finance) . It takes time for 3G's cuts and synergies to work their way through the business, and as this happens, you can see the projected runway the next several years as the debt is paid down, leverage decreases, and cash flow frees up for dividends and buybacks (even the first year saw a dividend increase every quarter). This is the cornerstone of most long theses I have read.

Is QSR a good long-term investment? I have no idea. Yes, Bill Ackman and Warren Buffett are investors, but don't think it's a slam dunk based on that. Just look at Ackman's bets on Herbalife ( HLF ) and Valeant ( VRX ) in the past year or the recent performance of famed Buffett stocks like American Express ( AXP ) and IBM (IBM). That's not to say these guys don't have stellar track records just don't let their names blind you to the risk in this name. They could be right about QSR's long-term shareholder value creation strategy, but it means pulling off growing sales of whoppers, iced caps, and medium double doubles around the world. Not familiar with those terms? Even if you are, many people in the world are not, and suddenly, we have a way more dicey long thesis predicated on a nebulous "growth" strategy that will have to be well executed to translate into gains for investors.

But here in the short term, going into February 15th's earnings announcement for Q4 and annual 2015, we have an interesting setup. QSR is a constituent of the declining TSX Composite's (-5.31% - last three months) worst performing sector over the past three months (consumer discretionary, down 16%). Yes, even worse than energy. On a day the market is gyrating with the Dow down 2.44% as I write this and the TSX down over 200 points, QSR has lost more than 4.5%. American investors can of course trade the same stock with the same ticker on the NYSE, which is testing support at around $30 USD while the Canadian touches $42; they will just note the values are lower adjusting for US dollars.

Technical traders would confirm here that the stock has just broken through its floor of support, trading at a level not seen...not seen in fact since the IPO (44.56 was the lowest it traded in the past year, before today), and might try to ride that trend further down. However, after looking at the chart, I would go long for two reasons. First, bears have not been able to stay in control of this stock for extended periods of time, I suspect because there is too much institutional money/individual Buffett followers buying into the long-term growth story (this is an extremely well-covered and visible stock). It is likely institutional/long-term investors will be averaging down if they can or buying as soon as this thing gets a modicum of upward momentum. And second, earnings on February 15th. The company has posted earning four times since the IPO, and the stock is 4/4 to the upside in the 1-2 weeks after earnings, usually gaining around 10%, if you look at the chart following previous earnings releases which are Feb. 17, 2015, April 27, 2015, July 27, 2015, and October 27, 2015.

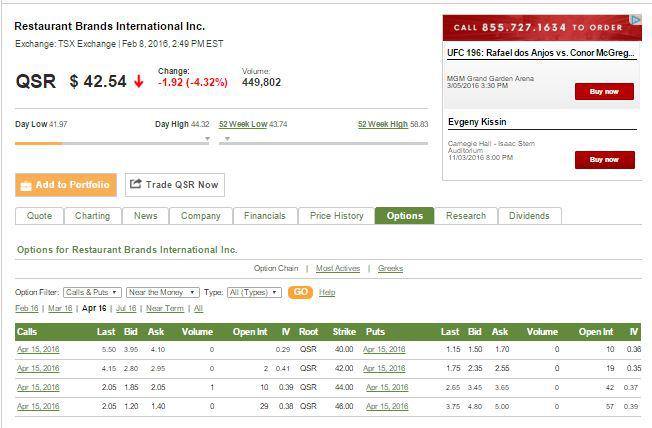

I have been long QSR in the past between $52 and $57. This opportunity came up, because today I noticed the March and April 44 calls losing a ton of value. QSR Canadian options trade in $2 increments. I initiated a position on the April 44 call at $2.05 as the 42s were very expensive now that they are in the money. This 44 call is mostly time value as it is out of the money (since this morning) and has lost over 50% of its last closing price.

Prices as of Feb 8:

Source: Tmxmoney.com

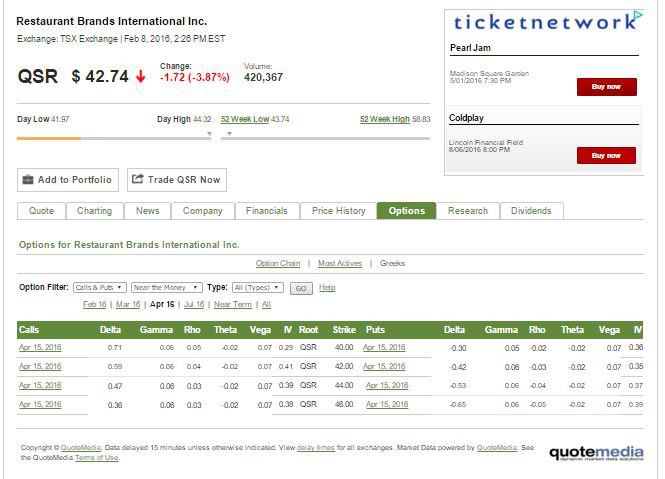

The risk/reward ratio of the trade is attractive. The delta was fluctuating between 48 and 55 today, meaning you have about a 50% chance of the stock hitting $44 in the next 67 days. I'm willing to bet that the chances are actually a lot higher than that because today is the first day the stock has traded under $44 since 2014. A gamma of 6 means delta will increase about 13.6% for every dollar increase in QSR, and a high but not outrageous implied volatility of 39.

Greeks as of Feb 8:

Source: Tmxmoney.com

The inherent risk here is that a 1% drop in implied volatility, with a vega of 0.07, will reduce our option price by 3.5%. We are also currently losing about 2 cents a day right now in theta decay. But the strategy is simple here. If the stock can break over $45 in the next 2-3 weeks, we will gain at least $1 of intrinsic value. I would put in a trailing stop at that price and would be happy to get out at it to capture the remaining time value and mitigate drops in the IV. A 42 March or April put could hedge this position further although it would eat into your cost to establish it, but I would wait until the next big up day in the market to buy it, as the puts have all increased considerably today following the momentous decline alongside the broader market. If I do not get the chance to enter the put as a hedge this week, I am comfortable with the risk as it is limited to what it cost me to enter the position, and I have 67 days for the stock to hit $46 to break even at expiration, which is right around where its long-term moving average is. If it breaks to the upside before, then this hopefully will have been a worthwhile undertaking.

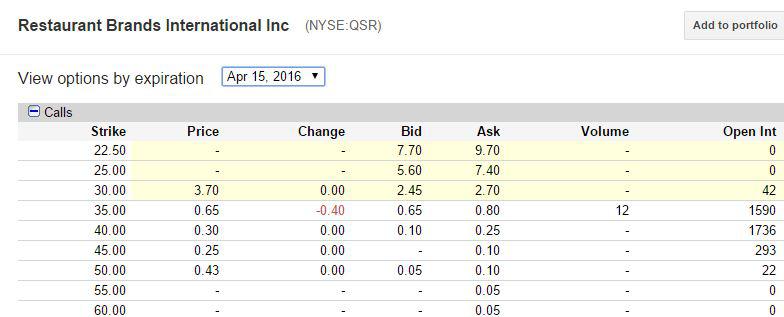

The American option chain is not as attractive going out to April 15 because the options trade in $5 rather than $2 strike increments, which means, as of close today, you would either need to buy a $3.70 $30 call (slightly in the money with the majority of the price being time value and IV) or the out-of-the-money $35 call, which is only $0.65 USD, but requires a 13.8% upside move to be at the money versus only 2.7% in the Canadian example I gave.

Bottom line is, in the near term, I think QSR is oversold after today's decline and represents a short/medium term opportunity, due to the history of positive trending after earnings and likely reversion to the mean. Longer term, I am a bit uncomfortable with the valuation, the leverage, and the hinging of the stock price on future international expansion/growth. I don't doubt Tim's ability to maintain a dominant market position in Canada, but the company's corporate bosses have much more ambitious international, and therefore riskier, designs in mind.

See also Alliqua Biomedical's (ALQA) CEO Dave Johnson on Q4 2015 Results - Earnings Call Transcript on seekingalpha.com

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

{kind=link}

{kind=link}

{kind=link}

{kind=link}