Credit: Shutterstock photo

Credit: Shutterstock photoBy Chris DeMuth Jr. :

Summary

Our top pick for 2018 is Reading International ( RDI ). At a high level, we believe investors in Reading at today's prices are paying a significant discount to Reading's intrinsic value as a standalone company, and that a unique combination of value enhancing investments, industry consolidation, a hostile takeover offer, and litigation among the controlling shareholders will unlock significant value in 2018. In a standalone scenario, we think Reading's shares are worth at least $20/share in 2018, and in a scenario where each of the company's parts are auctioned off to the highest strategic bidder, we believe the company would be worth at least $25/share and potentially over $30/share.

Overview

Reading is a holding company formed in 1999; however, its predecessor companies can trace their roots all the way back to the Reading Railroad (made famous by the Monopoly board game) in the pre-Civil War era. In its current form, the company was started when James Cotter Sr. took control of the Reading Railroad in the early 1980s. In 2001, he merged Reading with two of his other holding companies (Craig and Citadel). The merger transformed Reading into what it is today- an international business with major cinema (movie theaters) and real estate holdings in the U.S., New Zealand, and Australia.

Reading's strategy has been to use its two core segments (cinemas and real estate) to complement each other in a variety of ways.

- Cinemas can be used as anchors for large retail developments, so Reading can use their cinemas to jump start real estate projects.

- Real estate development is often expensive, and the steady cash flows from the cinemas can be used to fund real estate developments.

- Having a background in real estate gives Reading flexibility to convert cinemas into other projects when a movie theater is no longer the best use for a space (flexibility a pure play movie theater company may lack).

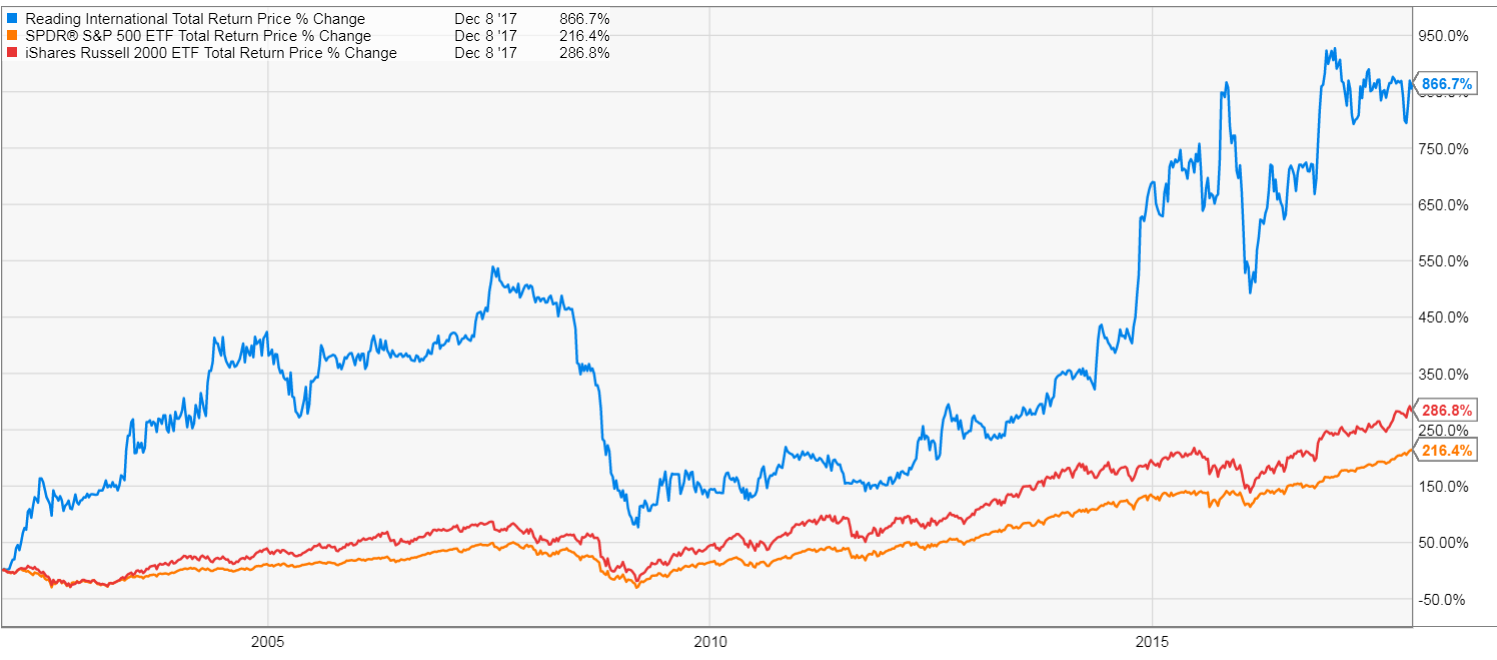

Reading's shareholders have been well rewarded by this strategy. Since the Reading / Craig / Citadel merger, shares have substantially outperformed their relevant benchmarks.

Despite the strong historical performance, we believe Reading continues to trade well below the sum of its part (SOTP), and that several events in 2018 will help to bridge the disconnect between Reading's stock price and its underlying value.

Before we dive into how we arrive at a value for Reading's parts, we want to quickly highlight why we think this opportunity exists. We believe there are several reasons for the discount: the company is controlled by the elder Cotter's children, the company's stock is smaller and more illiquid than many investors are willing to look at, significant international assets expose the company to foreign currency swings, and some one-time extraordinary expenses mask some of the company's profitability on a trailing basis. However, the key reason we think Reading is undervalued is that each of its three key value sources (cinemas, income producing properties, and investment / development properties) have wildly different economics and require significantly different valuation methodologies. In addition, each segment derives value from three different countries (U.S., Australia, and New Zealand), further increasing the complexity of analyzing the company. We think the complexity required to value each of these different parts has created an opportunity for investors willing to dive into Reading's financials.

With that out of the way, let's dive into each of Reading's key three parts: Cinemas, Income Producing / Operating Real Estate, and Investment and Development Real Estate.

Cinema Segment Overview

Reading operates cinemas in three different countries. They are the 10 th largest exhibitor in the U.S., the 4 th largest in Australia, and the 3 rd largest in New Zealand.

The cinema business is generally a pretty simple one so we won't dive too far into it here, but we will give a brief overview. A movie theater "rents" a film (i.e. Star Wars) from a studio (i.e. Disney / LucasFilm) and agrees to pay the studio a certain percentage of the admissions revenue (generally a bit over 50%, though tent pole films like Star Wars can command a premium ) in exchange for letting them use the film. The theater then tries to sell as many tickets as possible in order to drive their real profit source: high margin concessions (snacks, popcorn, drinks, etc.).

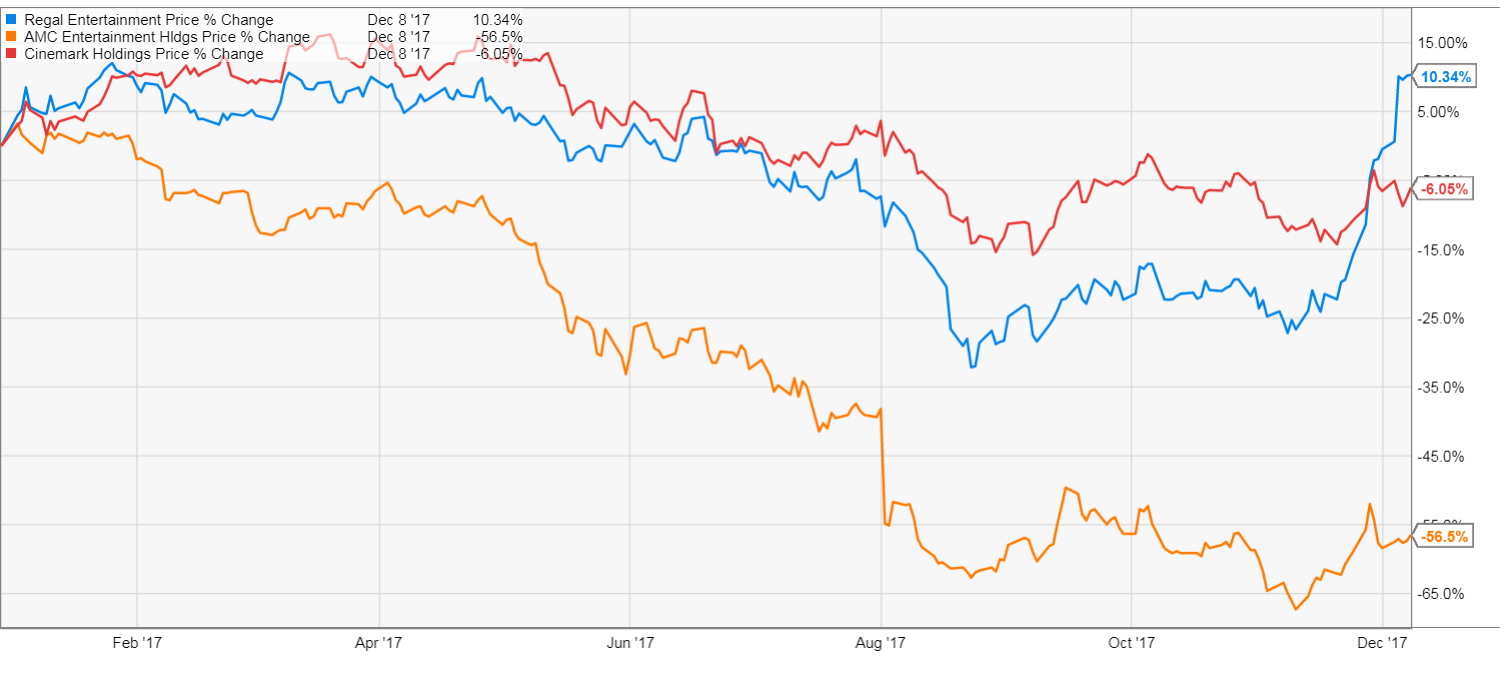

We think now is an ideal time to be looking to invest in movie theaters. 2017 has not been a great year for movie theaters, driven by an awful summer box office and investor worries that Hollywood studios will explore plans to shorten the film exclusivity window (the amount of time between a film being released in theaters and a film going into video on demand). You can see that fear reflected in the stock charts of Reading's major peers: AMC (the largest cinema chain in the world) has seen its stock more than cut in half in the past year, while Cinemark's stock is down as well and Regal's stock is only up 10% despite a buyout at a significant premium.

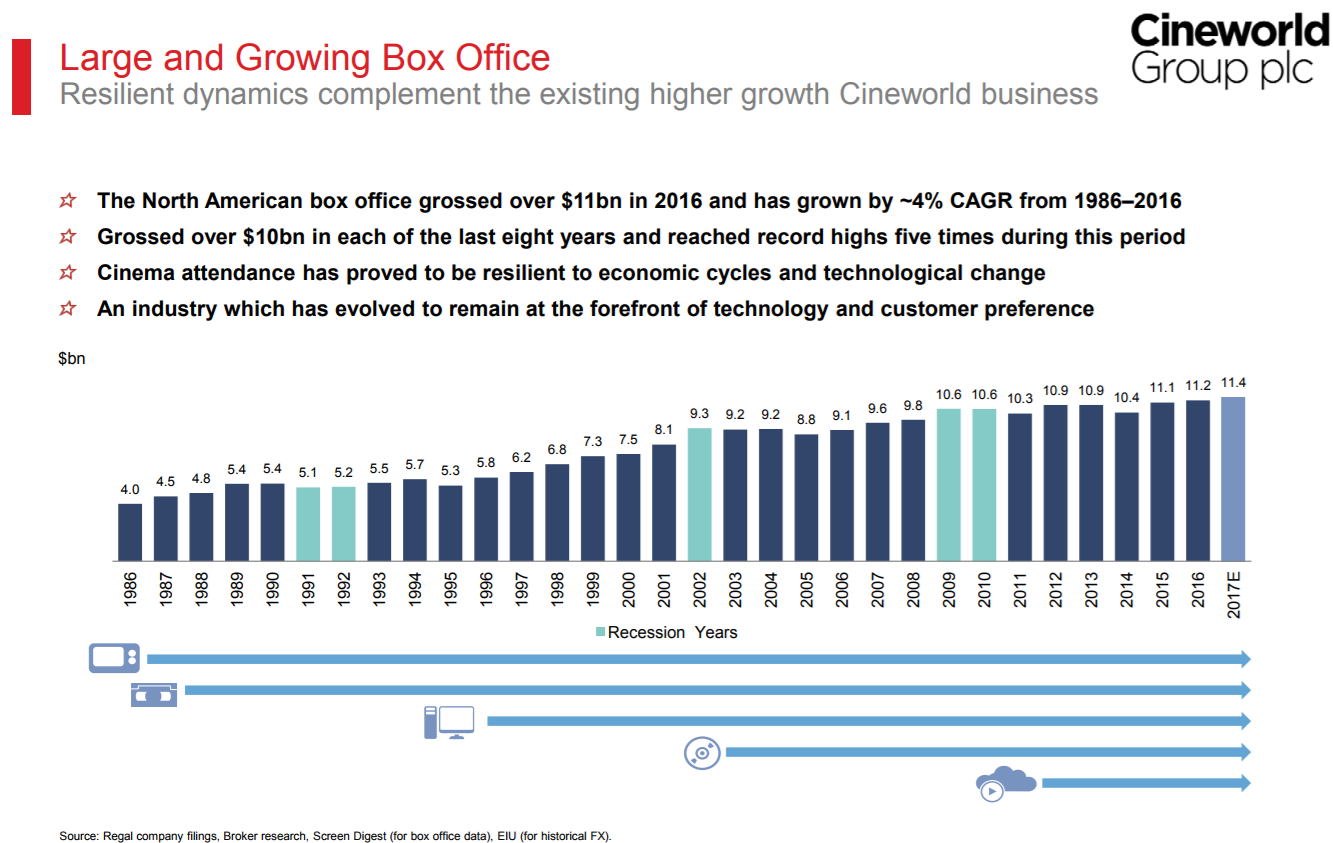

While we certainly acknowledge the risk from window shortening, we think the risk is a bit overblown. Pundits have been calling for the death of movie theaters for decades: in 2009, people thought the DVD would kill theaters, and before that people thought VHS or cable television would kill them. With the passage of time, each of those calls has proven wrong, and we believe that movie theaters will similarly survive the threat from streaming / window shortening. Why? Because going to a movie theater represents an activity / a chance to get out of the house, and as our world and lives become more connected to and focused on the internet, the value of events and experiences that take consumers out of their house will continue to increase. The domestic box office set a record high in 2016 and will be right around that high in 2017; we'd expect the box office to continue to grow slowly over time.

If we're right that the "death of the movie theater" will again prove overblown, then now should be an ideal time to be looking at investing in movie theaters. Trailing earnings and trading multiples for movie theater stocks are depressed, and both should recover as we move into 2018 (which is shaping up to have a strong box office driven by The Avengers: Infinity War, Deadpool 2, Fantastic Beasts 2, and plenty of others). In other words, investors in movie theater stocks in 2018 could get a "double whammy" of improving earnings driven by a better box office combined with an expanding multiple as fears of movie theater "death" prove unfounded.

For our base case, we conservatively value Reading's cinema segment at 8x LTM EBITDA, a slight discount to their larger peers (AMC, CNK, RGC), which gives us a total value of ~$370m. We think this multiple is conservative for a host of reasons:

- As mentioned above, we think both trailing earnings and current multiples for movie theater stocks are depressed and will expand as we enter 2018.

- The majority of Reading's profits on the Cinema side come from their Australia and New Zealand chains, not their U.S. chain. Their international theaters have higher margins and better growth profiles than the U.S. segment, and both those economics and the few mergers we've seen in those geographies suggest that the international side should command a multiple premium to the U.S. side

- Regal just entered into an agreement to be acquired by a foreign chain in a deal that valued Regal at ~10x LTM EBITDA. The synergies from a large domestic player buying Reading would be substantially higher than a foreign chain buying Regal, and that higher synergy level would likely merit a higher multiple for Reading.

- Reading is substantially behind U.S. peers in converting their cinemas to luxury recliner seating. As of their November 2017 Investor presentation (See slides 17 and 18 ), less than 15% of their theaters had been converted, which pales in comparison to ~ 40% at AMC and 25% at Regal . Seat conversions have been described as "moderate investments with high return" (peers have estimated >25% returns on their recent conversions). RDI is estimating they'll have recliners in ~half of their U.S. theaters and ~25% of their Australia / New Zealand theaters by the end of 2018. In total, Reading is forecasting investing >$50m into their theaters over the next two years as they install recliners. If Reading can match their peers "high returns" from those investments, it should drive earnings growth for several years going forward.

Operating Real Estate Overview

Reading's operating real estate segment consists of properties that are already up and running / producing income. Including long term leases that are effectively real estate investments, the segment consists of just under 1m square feet of properties in the U.S., Australia, and New Zealand. Most, but not all, of the properties are anchored by a Reading movie theater.

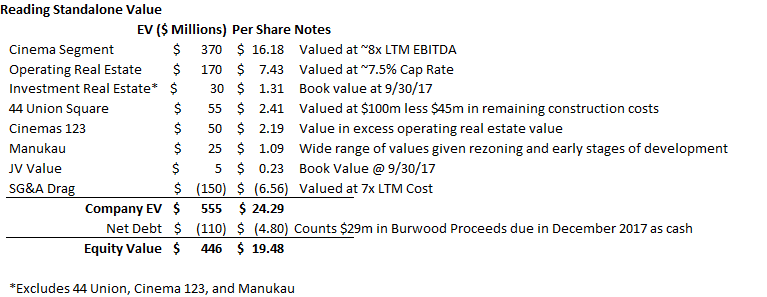

We estimate Reading's operating properties are worth ~$170m. We base this estimate on two different valuation methods.

- Real estate is most commonly valued using what is known as a capitalization rate (cap rate for short). In essence, you take the real estate's net operating income (aka NOI; revenue less operating expenses), decide what yield the property should give you, and divide the net operating income by that yield to come up with a market value. So if a building generates $1m in NOI and you apply a 10% cap rate to it, that building would be worth $10m. Reading doesn't disclose a pure NOI figure for their operating real estate, but we estimate the segment did ~$13m in NOI in the trailing twelve months (based on LTM segment EBITDA of $11.3m and adding back ~75% of segment SG&A). Both publicly traded companies and private assets with similar operating / risk profiles to Reading's operating real estate generally trade for below 7% cap rates in the U.S., and we believe Reading's Australia and New Zealand assets would get a similar cap rate (in fact, some recent salesmake us think they may get an even lower cap rate if placed on the open market). We conservatively apply a 7.5% cap rate to adjust a bit for Reading's complexity (selling assets located across three countries is a bit more involved then selling them in one market); applying that 7.5% rate to Reading's LTM estimated NOI of $13m results in a value of ~$170m.

- To back up that value, we look to the real estate's book value. Reading's 2016 10-k discloses combined net book value of their operating real estate and long-term leasehold properties of $153m ( see p. 26 ). Given the capex in their operating real estate segment so far this year, we estimate that the number will be over $160m when they file their next annual report. Given how long held some of these properties are, we feel valuing them slightly above book is likely very conservative.

Investment and Development Property Overview

We turn now to the piece of Reading with the biggest upside: Investment and Development property. While several of these properties have significant upside, our main focus here is on their one large new Zealand property (Manukau) and two NYC properties (Union Square Theater / 44 Union Square and Cinemas 1,2,3), as we believe all three of these properties could have "hidden" upside to Reading of >$50m. We value all other investment properties at book value of ~$30m (as of 9/30/17); this will likely prove conservative

The first big property is 44 Union Square. Reading purchased this building in February 2001 for $7.7m. This building was once known as Tammany Hall and was designated an official landmark in 2013 . After a long fight, Reading won the rights to redevelop the entire of the building. Those rights, combined with the revitalization of the whole Union Square area, have resulted in a substantial uplift in value for 44 Union Square. Reading is capitalizing on this by investing >$70m ( mostly funded by $57.5m in debt ) into turning 44 Union Square into a modern office and retail complex.

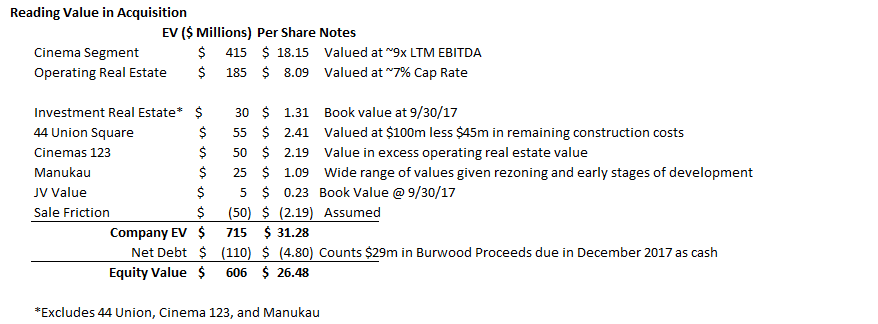

44 Union Square currently sits on Reading's balance sheet for ~$32m and will cost another ~$45m to build out. The property should be completed in the back half of 2018, and we would expect Reading to have the building substantially rented out well before then (leasing for the office space launched in Q3'17, and the company is already in talks to lease 100% of the retail space). The building's ultimate valuation is highly sensitive to both the rents they get for the office and retail space (retail consists of ~40% of the space but commands substantially higher rental rates) and the cap rates applied to the building. Our work indicates the building will likely be worth over $125m once completed (with the potential to be worth substantial more; again, a lot depends on how much the retail space goes for). To account for the wide range of potential outcomes, we value Union Square at the absolute lowest range of our models: $100m. We think this is extremely conservative given the company is investing ~$70m into a huge redevelopment, so we're giving them basically no credit for value enhancement, but we prefer to be conservative given the wide range of outcomes. Valuing the building at $100m less the $45m in remaining build out costs gives us a net equity value for 44 Union Square of $55m.

The next asset of note for Reading is their 75% ownership of Cinema 1,2,3. Cinema 1,2,3 is currently an operating property with a book value of $24.4m (as of 12/31/16); however, Cinema 1,2,3 is a prime location across the street from Bloomingdales on 3 rd Avenue in NYC. In June 2017, Reading reached an agreement with their neighboring property to "work together on a comprehensive mixed-use plan to co-develop the properties located on 3rd Avenue" ( see p. 26 ). This agreement is potentially huge- Reading noted in 2012 that they had received offers of $40-45m for the Cinema 1,2,3 property. One of the reasons Reading rejected the offers is they thought a combination with the neighboring property would result in a $200m development. While nothing is guaranteed, if this partnership works out the upside to Reading could be massive. We value Cinema 1,2,3 at $100m, which works out to $75m for Reading's 75% stake. We base this value on a wide range of scenarios, with a heavy emphasis placed on the downside represented by the $40-45m bids received in 2012 (when real estate values were much lower and before the redevelopment agreement had been reached). This $75m value results in a ~$50m NAV boost after backing out the $24m of value already captured from Cinema 1,2,3's operating property value.

The last asset of note in the investment properties is >70 acres of land in Manukau, New Zealand. This land is on Reading's books for $12m. The potential upside here is massive- this land is close to the Auckland airport, and Reading managed to get 64 of the acres rezoned from agricultural to light industrial in late 2016 (the other 6.4 acres were already zoned heavy industrial). Given this massive rezoning, the land is likely worth significantly more than what Reading carries it for on their books (management suggested on their Q1'17 call that the land was worth double book value, and in their Q3'17 call management suggested they had multiple offers to sell the land for a "nice profit"). The company is exploring options to develop the land, and any potential partnership or announcement will likely reveal a value significantly in excess of the company's carrying value. We value the land at double where Reading carries it at, or $25m, but given the lack of information and early stages of development, the value will ultimately depend on how the development goes. The land could end up being worth significantly more than this valuation.

Corporate overhead

The last thing we need to do before we can value Reading is deduct a value for their corporate G&A. Corporate G&A is a tough thing to value, as it's obviously necessary for the company to continue operating as a standalone business, but if the company were to be sold virtually 100% of it would disappear as a synergy for a strategic buyer. Corporate SG&A has run ~$22m over the last twelve months, though this number is slightly inflated due to an ongoing legal battle over the company's ownership we will discuss later. We value SG&A as a value drag at 7x LTM expenses, or ~$150m. With corporate overhead accounted for, we're now ready to put all of Reading's pieces together and come up with an estimated value,

Putting it all together: Reading's Sum of the Parts (SOTP)

The table below sums up each of the valuations discussed above (it also values Reading's $5m of Joint Ventures at book value). After adding all of the parts up and subtracting $110m of net debt, we come up with an equity value per share of $446m, or $19.46/share. We'll also note that Reading has significant tax assets (~$40m in net tax assets before valuation allowances) which we have assigned no value to here.

It should be noted that the value above is how we value Reading as a standalone public company. If, however, the company were to be shopped, we think there would be significant strategic interest in all of Reading's assets. Not only would there be huge cost synergies between Reading and strategic acquirers, who could eliminate virtually all of Reading's substantial SG&A at both the corporate and segment level, but strategic acquirers would likely significantly enhance Reading's value as a strategic acquirer would generally carry a substantially lower cost of capital (helpful for funding the recliner seat roll out in the cinema segment and critical for funding the development of the investment properties) and generally trade for multiples well in excess of our individual Reading segment valuations.

When we value Reading as a strategic target, we make three big changes to our Reading standalone valuation model.

- We increase the Cinema Segment multiple from 8x LTM EBITDA to 9x. This multiple is still below the pre-synergy multiples we've seen in the two most recent acquisitions in the cinema space (both Regal's current acquisition and AMC's acquisition of Carmike last year were done at ~10x pre-synergy EBITDA).

- We reduce the cap rate for the Operating Real Estate segment from 7.5% to 7% given the operating synergies and lower cost of capital available to an acquirer.

- We eliminate the $150m SG&A drag from our base case as acquirers would likely eliminate all SG&A; however, we partially replace it with a $50m "sale friction" charge to account for the likely costs of a sales process. We think this is justified because Reading would likely need to sell their different pieces to multiple buyers to achieve a full price, and selling to multiple buyers generally incurs extra costs.

We leave all other assumptions from our base case the same in our sales case; this could be conservative as both Cinemas 1,2,3 and 44 Union Square would like attract significant interest if they were to be put up for sale. The end result is an "acquisition value" share price of $26.48.

Hopefully we've laid out a coherent case for why Reading is undervalued as a standalone company. That's great, but why did we chose Reading specifically our top pick for 2018?

The answer is that there are several company specific catalysts that could unlock Reading's value in 2018, including multiple catalysts that could result in the sale of the whole company (likely at a large premium to today's price).

The largest catalyst stems from Reading's ownership structure. Reading has two share classes: the more liquid but non-voting class A shares, and the less liquid but voting class B shares. Reading's Founder, James Cotter Sr, owned the majority (~2/3) of the Class B shares. When he died, he left the majority of his shares in a Trust for his grandchildren, while the rest of his shares remained in his estate with the intention that they would ultimately "pour over" into the Trust.

However, in the wake of his death, Cotter Sr.'s children have been involved in a " massive power grab " for control of the company, with his daughters pitted against his son. His daughters were ultimately successful in kicking the son out of the company and taking control, but their actions are now being contested in court. Of particular interest to us is that the court has appointed a temporary trustee ad litem who will have "the narrow and specific authority to obtain offers to purchase the Reading stock in the voting trust." Because the Trust controls ~41.4% of Reading's voting stock and the rest is spread among several investors (including the Cotter estate, Mark Cuban (owns ~12% of voting shares), and Mario Gabelli (owns ~5% of voting shares , this is a recent purchase as they just filed on RDI this week)), whoever controls the trust's shares will be in the driver's seat for determining the future of Reading.

Will the trustee force a sale of the voting stock? We think there is certainly a good chance it happens. The trustee ad litem's job is to do what is in the best interest of the trust's beneficiaries (in this case, the Cotter grandchildren), and there is a strong argument to be made that shopping the shares and taking an offer for them that represents a significant premium to not only the current share price but also any historical price the stock has ever traded at is, by far, the best option for the trust's beneficiaries. In addition, given that the Cotter siblings are fighting, it could be argued that some of the grandchildren would be disadvantaged if the trust continues to hold stock in the company that effectively provides one side of the family control of the company against the wishes of the other side (in other words, while trusts don't always need to consider diversification and could hold on to a concentrated position like Reading's voting stock, in this case we think the prudent person test would suggest the trustee should sell the stock to diversify).

If the trustee does decide to put the trust's shares up for sale, we're confident there would be significant interest in buying the shares and, as part of any deal, we would not be surprised to see the buyer try to take the whole company private or see the board recommend selling the whole company to prevent a buyer from taking control through a forced auction. We've already seen one strategic bidder for all of Reading: Paul Heth's Patton Vision teamed with TPG Capital to offer $18.50/share for Reading in December 2016, and a court filing in October 2017 confirmed Heth was still interested in buying the Class B voting stock in the Cotter Trust and had again contacted Reading about buying the whole company on an all cash basis in September 2017.

So our home run scenario would involve Reading running a full auction for the full company, either because their hand is forced by the trustee ad litem selling the trust's voting shares or because the board decides now is the right time to monetize Reading. However, even without a full sale of the company, we see multiple catalysts on the horizon to unlock value in Reading.

An obvious catalyst is earnings growth. Right now, a substantial part of Reading's asset base consists of the investment properties, which have substantial asset value but do not produce any earnings (in fact, due to SG&A costs, these are a slight earnings drag). Over the next few years a substantial amount of these properties will begin producing income / earnings as Reading completes their redevelopment. This earnings ramp will start once 44 Union Square's redevelopment is finished / fully leased out and then continue to ramp up as Cinemas 1,2,3 and Manuka are developed. In addition, earnings growth will be further boosted as Reading's cinema remodels and new theater openings begin to bear fruit. Combining those earnings growth streams with falling SG&A costs as Reading begins to put the Cotter estate litigation behind them (Reading has exhausted their corporate D&O insurance and is funding the litigation out of pocket, which is a serious earnings drag that has cost them $1.1m so far this year), we think Reading is set to substantially grow earnings over the next few years, and this earnings growth should help investors more easily see Reading's intrinsic value (and assign a share price commensurate to it).

Reading's capital allocation can also create value for shareholders. In the first three quarters of 2017, Reading repurchased just over 400k shares of stock, or just shy of 2% of shares outstanding. Given how far below intrinsic value Reading trades, these share repurchases are significantly accretive for remaining shareholders, and with the company having just received ~$ 28m in cash , there's reason to believe the company's share repurchases could accelerate as we head into 2018 (the company has >$18m of authorization on their current share repurchase plan, which would let them buy back ~5% of their shares at today's prices).

Speaking of share repurchases, on the Q3'17 call, management noted that they had paused share repurchases because of "an opportunity that arose for an alternative use of funds". While we struggle to see how anything could be as accretive to Reading's shareholders as buying back their shares at these prices, it's not hard to read between the lines and see they're likely talking about some M&A. Given the company's history of M&A and how accretive the purchase of smaller movie theaters has been, if the company does announce some type of acquisition it's likely to be one that benefits shareholders.

Conclusion

To wrap this up, Reading is our top pick for 2018. In an upside scenario, ongoing litigation could spur a sale of the company for a large premium to a strategic buyer. In a downside scenario, SG&A starts to drop as the litigation is resolved and earnings pick up substantially as the investments in new cinemas, recliners, and 44 Union Square start to flow through the income statement. Either way, we're confident that those catalysts will drive Reading's stock price much closer to its intrinsic value by the end of 2018.

See also General Electric: The Crazy Ex-Girlfriend I'm Now About To Marry on seekingalpha.com

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}