Making cars is tough, and it's even tougher if you start a new vehicle brand from scratch. The huge upfront investments required for production create a barrier to entry, so very few new automotive brands achieve sustainable success. Recent examples include Tesla and BYD, but there are dozens of failures for every successful car business.

Rivian Automotive (NASDAQ: RIVN) is trying to become the next sustainable automotive brand. By focusing on electric vehicles (EVs), premium vehicles, and outdoor enthusiasts, the brand has found a niche and is now delivering over 10,000 vehicles to customers every quarter. The stock is up close to double from April when it hit $8 a share, but it's still off 90% from highs set at its initial public offering (IPO).

This business is at a crossroads. After seeing its recent earnings report, here's my prediction for what's next for Rivian stock.

Stagnating deliveries, more profitable new models

Earlier this month, Rivian updated investors with its second-quarter financial results. The numbers were a mixed bag. On the one hand, deliveries for its initial products remain strong, posting 13,800 for the quarter and 56,900 over the past 12 months. That is up significantly from just 20,000 deliveries at the end of 2022.

On the other hand, deliveries have stagnated for a few quarters, and production is falling. Production was just 9,600 in the second quarter, down from a high of 17,500 at the end of 2023. Management claims this production slowdown is due to the company retooling its factories for new models. However, if you look at the quarters preceding this change, it is clear that production was outpacing deliveries to customers, indicating a quarterly demand ceiling for these first product models.

Updated EV models are vital for Rivian, not just to boost deliveries, but because they supposedly have better unit economics than the initial products. Shockingly, Rivian has negative gross margins -- significantly negative, in fact. Last quarter, gross margin was negative 39%, leading to a $1.375 billion operating loss on $1.158 billion in revenue. Not great. This needs to be addressed in the coming quarters and years.

Volkswagen joint venture

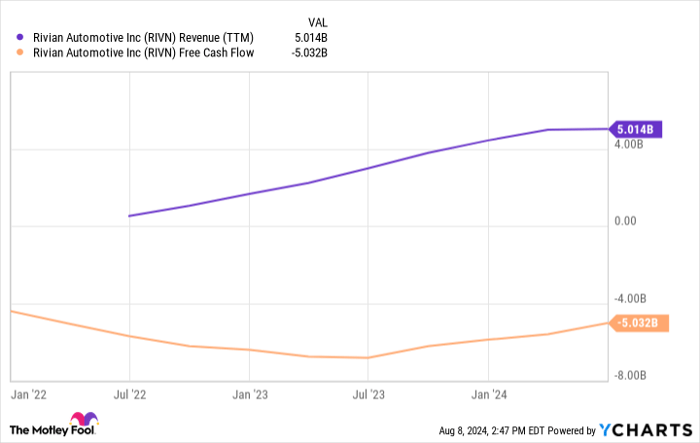

With bad profit margins, Rivian is currently burning a lot of cash. Over the last 12 months, the company has burned $5 billion in cash flow. With less than $10 billion in cash on the balance sheet, this cash burn will lead to a liquidity crisis within two years at its current burn level.

In order to extend its burn period before (hopefully) reaching scale, Rivian just announced a partnership with Volkswagen. The partnership involves a joint venture and planned total investment into Rivian of $5 billion by Volkswagen. As a part of the partnership, Rivian will be licensing its software and electronics systems for Volkswagen's new EV models. While this is many years in the future, this could lead to high margin revenue for Rivian and prove its technological capabilities.

Either way, the most important thing is cash infusion into the balance sheet.

RIVN Revenue (TTM) data by YCharts

Profitability is what matters (eventually)

Rivian management talks a lot about the future: Future products, future software deals, and future unit economics. The company continues to put up poor profit figures today, though. Gross margins are well in the negative, and operating margins are over negative 100%.

The stock may be up in the last few months, but what eventually matters over all else is profits. If Rivian can scale production to hundreds of thousands of vehicles a year and tens of billions in revenue (it generated $5 billion over the last 12 months), the company may hit positive profit margins and generate a few billion in earnings each year. This should also lead to positive free cash flow. At a market cap of just $15 billion today, the stock is likely higher in a few years under this scenario.

However, I don't think this scenario is likely. Rivian talks about profitability -- it just never shows it. Given the concern about oversupply in the EV sector and the historical track record, Rivian will not generate a profit anytime soon. For that reason, I think the stock will head lower and is one investors should avoid for the time being.

Should you invest $1,000 in Rivian Automotive right now?

Before you buy stock in Rivian Automotive, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Rivian Automotive wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $641,864!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of August 6, 2024

Brett Schafer has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends BYD Company, Tesla, and Volkswagen Ag. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.