Key Points

Higher oil prices should fuel faster growth this year.

The company could finally find a partner to develop Lake Charles LNG.

It should start seeing some multiple expansion.

- 10 stocks we like better than Energy Transfer ›

Energy Transfer (NYSE: ET) has already soared more than 20% this year. That pushed the master limited partnership's (MLP) unit price up almost to $20.

I think the energy stock has a lot further to run. I believe that the market is massively underpricing the potential that oil prices will remain higher for longer, with the potential for a significant spike if the U.S. launches new attacks against Iran. Add in a couple of other catalysts, and I predict the MLP's unit price will hit $25 this year, a more than 25% increase from its current price.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Image source: The Motley Fool.

Oil-fueled upside potential

Energy Transfer doesn't produce any oil and has limited direct exposure to commodity prices. However, the pipeline company should still benefit from higher oil prices.

One way is through the roughly 10% of its earnings that have some commodity price exposure. The company's oil-linked earnings will be higher this year.

Additionally, Energy Transfer should benefit from higher volumes across its liquids pipelines and marine export terminals due to the war-fueled boost in U.S. energy exports. Energy Transfer's Nederland terminal is a key hub supporting oil releases from the U.S. Strategic Petroleum Reserve. Additionally, NGL exports from Nederland and other marine terminals will surge this year to offset Middle Eastern supply disruptions. The company will earn higher fee-based income from these higher volumes. Higher earnings from higher oil prices should continue to drive Energy Transfer's unit price higher this year.

Lake Charles LNG optionality

Energy Transfer announced the suspension of its Lake Charles LNG development last year. The company opted to halt work on the proposed liquefied natural gas (LNG) export terminal to focus on other higher-return, lower-risk natural gas infrastructure projects. However, while Energy Transfer ceased development, it remains open to discussions with third parties interested in developing the project.

The Strait of Hormuz closure has likely piqued interest in restarting this development. It has disrupted 20% of global LNG supplies, driving prices up by one-third this year. The prolonged closure of that crucial energy waterway is likely prompting many countries to diversify their LNG supply. That could enable Energy Transfer to find a development partner willing to take over the project, adding a meaningful long-term value driver for its gas pipeline business. Signing a deal to restart Lake Charles could give its unit price a nice boost.

Multiple expansion potential

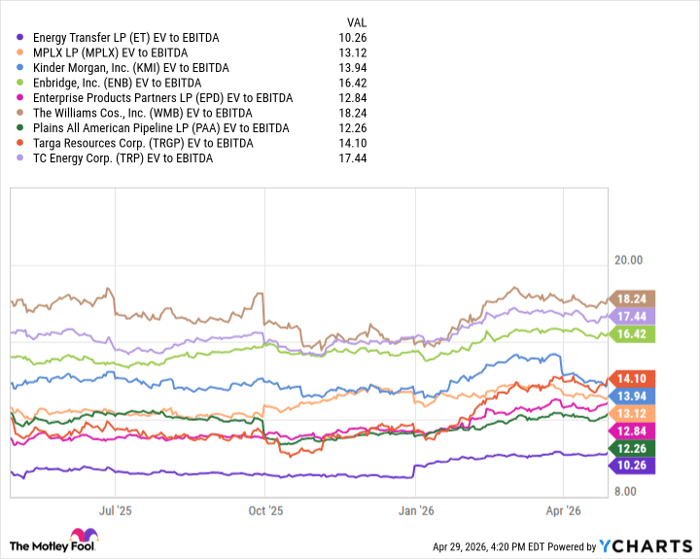

While Energy Transfer's unit price has surged this year, it still trades at the lowest valuation among large-scale energy midstream companies:

ET EV to EBITDA data by YCharts

There's no discernible reason for the discounted valuation. Energy Transfer is in its strongest financial position in history. While the company's earnings growth rate slowed last year due to lower commodity prices and fewer growth catalysts, it will accelerate in 2026. Energy Transfer currently expects its earnings to grow by 9% to 11.5% this year. It could grow even faster if oil prices remain elevated. Energy Transfer should continue growing at a healthy clip in the coming years as more expansion projects enter commercial service, primarily gas pipelines to support higher power demand from AI data centers and other catalysts.

I predict that this will finally be the year the market recognizes Energy Transfer's improved financial profile and growth prospects, driving valuation multiple expansion closer to the peer group average.

Multiple upside catalysts

Energy Transfer hasn't traded above $25 in more than a decade. I think that will change this year as multiple upside catalysts fuel a further rally in its unit price. Add in the MLP's 6.8%-yielding distribution, and it should continue to generate high-octane total returns this year.

Should you buy stock in Energy Transfer right now?

Before you buy stock in Energy Transfer, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Energy Transfer wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $496,797!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,282,815!*

Now, it’s worth noting Stock Advisor’s total average return is 979% — a market-crushing outperformance compared to 200% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of May 1, 2026.

Matt DiLallo has positions in Enbridge, Energy Transfer, Enterprise Products Partners, and Kinder Morgan. The Motley Fool has positions in and recommends Enbridge and Kinder Morgan. The Motley Fool recommends Enterprise Products Partners and Tc Energy. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.