Pinterest, Inc.’s PINS shares have declined 14.7% in a year against the Internet - Software’s growth of 4.5%.The stock has also underperformed the Zacks Computer & Technology sector and the S&P 500’s growth during this time frame.

Image Source: Zacks Investment Research

Shares of PINS have outperformed peers like Snap Inc. SNAP but underperformed Meta Platforms, Inc. META over this period. Snap’s shares have plunged 35.3%, while shares of META have risen 7.8% in the same time frame.

PINS Plagued by Rising Operating Expenses, Growing Competition

The company heavily relies on advertising as its primary source of revenues. Moreover, it is highly dependent on the retail sector and shopping ads. The company faces stiff competition from other social media platforms such as META, Reddit and SNAP. META’s Instagram has emerged as one of the primary competitors for Pinterest. Instagram has strong e-commerce integration, enabling users to shop directly from posts. The company also faces competition from smaller companies, including Allrecipes, Houzz and Tastemade that offer users engaging content and commerce opportunities through similar technology, products and features or services.

Owing to this growing competition, Pinterest is spending heavily to develop its AI native product suite, focusing on improving engagement in the platform. This effort to retain users and expand into new markets is driving up the operating expenses.

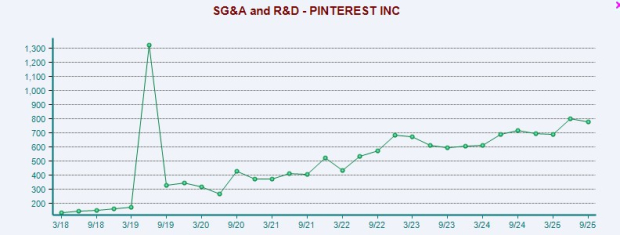

In the third quarter, the company’s total costs and expenses were $990.6 million, up from $904.3 million in the year-ago quarter. On a GAAP basis, research and development expenses rose to $371.3 million from $326.7 million. The increase in opex is due to growing infrastructure spend and investment in headcount to support AI and various other product initiatives. These may deliver long-term growth, but can create pressure on the bottom line in the short term. In the third quarter, the bottom line fell short of the Zacks Consensus Estimate by 2 cents.

Image Source: Zacks Investment Research

Macroeconomic Challenges and Lower Monetization Are Headwinds

Pinterest is exposed to macroeconomic challenges, tariff-related uncertainties and consumer spending cycles. Several large U.S. retailers are facing tariff-related margin pressure. This has led to moderating ad spending, directly impacting PINS’ net sales growth in this region. The company’s year-over-year growth rate is declining in the United States and Canada.

Despite growth in ad impression, the company’s ad pricing declined 24% year over year. Lower monetization in previously unmonetized international markets is dragging down the ad price.

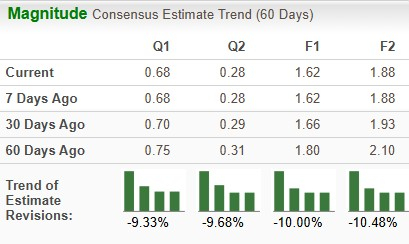

Estimate Revision Trend of PINS

Pinterest is currently witnessing a downtrend in estimate revisions. Earnings estimates for PINS for 2025 have moved down 10% to $1.62 over the past 60 days, while the same for 2026 has decreased 10.48% to $1.88.

Image Source: Zacks Investment Research

Key Valuation Metric of PINS

From a valuation standpoint, Pinterest appears to be relatively cheaper compared with the industry and below its mean. Going by the price/sales ratio, the company’s shares currently trade at 3.83 forward sales, lower than 4.94 for the industry and the stock’s mean of 5.04.

Image Source: Zacks Investment Research

End Note

High reliance on retail and shopping ads coupled with growing competition from other industry leaders such as META, Reddit and Snap are concerns. Tariff-related uncertainties and several other macroeconomic challenges continue to impact ad spend. Downtrend in estimate revision highlights dwindling investors’ confidence in the stock’s growth potential. With a Zacks Rank #4 (Sell), investors should avoid investing in PINS stock at present.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power.

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Snap Inc. (SNAP) : Free Stock Analysis Report

Pinterest, Inc. (PINS) : Free Stock Analysis Report

Meta Platforms, Inc. (META) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.