Pilgrim's Pride Corporation PPC delivered a strong first-quarter 2025 performance with an adjusted EBITDA margin of 12%, up 350 basis points from the prior year. This marks a substantial improvement, driven primarily by strength in the U.S. business, where adjusted EBITDA margin surged to 14.3% compared with 9.4% a year ago. Prepared Foods and Case Ready led the way, while Big Bird benefited from elevated market pricing and optimized throughput.

But is this margin surge sustainable? The company faced only moderate grain input costs and gained from seasonal pricing strength. Additionally, distribution gains in value-added and branded products supported the mix. However, challenges such as live production volatility, hatchability concerns and foodservice softness still linger. Quick service restaurant volumes were strong, but foodservice traffic is under pressure industrywide.

Margin contributions from Europe and Mexico further complicate the picture. Mexico's business faced $8.5 million in foreign exchange headwinds and continues to see quarterly volatility tied to the live market. Meanwhile, Europe achieved a milestone with an 8.1% margin, implying progress from its ongoing structural reorganization. Key initiatives, such as the integration of support functions, manufacturing optimization and a sharpened focus on strategic customer partnerships, have helped enhance performance, supported by continued innovation in product offerings.

The increased adjusted EBITDA margin highlights what Pilgrim’s Pride can achieve when disciplined execution aligns with favorable market conditions. Sustaining this level, however, will depend on consistent demand across retail and foodservice, stable commodity costs and tight control over operational variables. While the result is a significant achievement, maintaining it will require continued focus on execution and a supportive macroeconomic environment.

Pilgrim's Pride’s Zacks Rank & Share Price Performance

Shares of this Zacks Rank #3 (Hold) company have lost 6.3% in the past three months compared with the industry’s 4.7% decline. PPC underperformed the broader Consumer Staples sector’s decline of 0.4% and the S&P 500 index’s growth of 9.4%, during the same period.

PPC Stock's Past 3-Month Performance

Image Source: Zacks Investment Research

Is PPC a Value Play Stock?

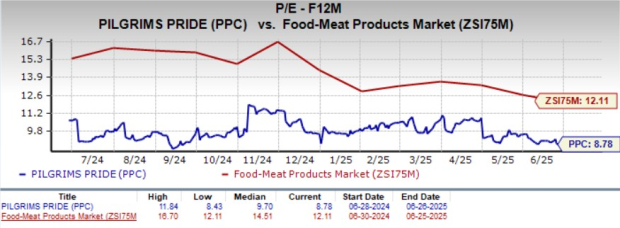

Pilgrim’s Pride currently trades at a forward 12-month P/E ratio of 8.78, which is slightly down from the industry average of 12.11 and notably below the sector average of 17.31. This valuation positions the stock at a modest discount relative to both its direct peers and the broader consumer staples sector.

PPC P/E Ratio (Forward 12 Months)

Image Source: Zacks Investment Research

Some Solid Bets

BRF S.A. BRFS raises, produces and slaughters poultry and pork for the processing, production and sale of fresh meat, processed products, pasta, margarine, pet food and other products. It currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for BRF S.A.'s current fiscal-year sales and earnings implies growth of 11.1% and 8.3%, respectively, from the prior-year levels. BRFS delivered a trailing four-quarter earnings surprise of 5.4%, on average.

Mondelez International MDLZ manufactures, markets and sells snack food and beverage products. It presently has a Zacks Rank of 2. MDLZ delivered a trailing four-quarter earnings surprise of 9.8%, on average.

The consensus estimate for Mondelez’s current fiscal-year sales implies growth of 5.3% from the year-ago figures.

Oatly Group AB OTLY, an oatmilk company, provides a range of plant-based dairy products made from oats. It presently has a Zacks Rank of 2. OTLY delivered a trailing four-quarter earnings surprise of 25.1%, on average.

The consensus estimate for Oatly Group’s current fiscal-year sales and earnings implies growth of 2.3% and 63.8%, respectively, from the year-ago figures.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpBRF S.A. (BRFS) : Free Stock Analysis Report

Pilgrim's Pride Corporation (PPC) : Free Stock Analysis Report

Mondelez International, Inc. (MDLZ) : Free Stock Analysis Report

Oatly Group AB Sponsored ADR (OTLY) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.