Parker-Hannifin Corporation PH is benefiting from strong momentum in the Aerospace Systems segment, driven by strength in the commercial and military end markets across both OEM and aftermarket channels. The segment’s organic revenues jumped 14% year over year in the second quarter of fiscal 2025 (ended December 2024). In the quarters ahead, the Aerospace Systems segment is likely to gain from strong demand for its products and aftermarket support services in the general aviation market, driven by growth in air transport activities. Strength in its defense end market, owing to stable U.S. and international defense spending volumes, is also likely to be beneficial. Parker-Hannifin expects the Aerospace Systems segment’s organic sales to increase 11% from the year-ago level in fiscal 2025 (ending June 2025).

Parker-Hannifin solidified its product portfolio and leveraged business opportunities through asset additions. In September 2022, the company completed the acquisition of Meggitt plc, a global leader in motion and control technologies. The acquisition expanded Parker-Hannifin’s presence in the United Kingdom, positioning it well to provide a broader suite of solutions for aircraft and aero-engine components and systems.

The company has doubled its portfolio of aerospace, filtration and engineered materials in the past eight years. Also, it is strategically shifting toward longer-cycle products (to attain stable and predictable revenue streams) supported by secular growth trends, which is improving its revenue mix. The growth drivers, i.e., the Win strategy, macro-CapEx reinvestment (a strategy of reinvesting capital expenditures into a company's operations, assets and growth initiatives), acquisitions and secular growth trends, are likely to help Parker-Hannifin achieve 4-6% revenue growth by fiscal 2029. The company also expects to increase its earnings by more than 10% per share (CAGR) and is set to achieve a 27% adjusted segment operating margin by fiscal 2029. It is worth noting that Parker-Hannifin reported an adjusted segment operating margin of 25.6% in the second quarter of fiscal 2025, up 110 bps from the year-ago number.

The company is committed to rewarding its shareholders through dividends. In April 2024, it hiked its dividend by 10% to $1.63 per share (annually: $6.52). In the first six months of fiscal 2025, Parker-Hannifin rewarded its shareholders with dividends of $420.1 million, up 10.2%.

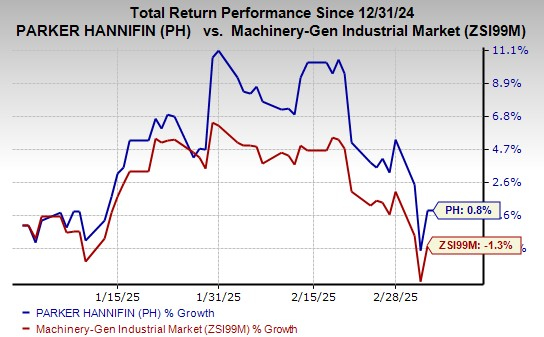

In the year-to-date period, this Zacks Rank #3 (Hold) company’s shares have gained 0.8% against the industry’s 1.3% decline.

Image Source: Zacks Investment Research

Downsides of PH

PH is plagued by weakness across the Diversified Industrial segment. Challenging conditions in the off-highway end market, due to softness in the construction and agricultural sectors, have been affecting both the North America and international businesses of the segment. Softness in the transportation end market, arising from lower demand for automotive cars, is ailing the North America business as well. Challenges in the energy end market owing to near-term delays in projects and continued destocking are concerning as well.

Parker-Hannifin intends to boost its revenues and profitability through overseas business expansion. However, this exposes the company's financial performance to various risks like political, environmental and foreign currency exchange rate fluctuations. In the second quarter of fiscal 2025, foreign currency translation lowered sales by approximately 0.9%. Foreign currency headwinds are expected to affect the company’s top line by 1.5% in fiscal 2025.

Stocks to Consider

Some better-ranked companies are discussed below.

RBC Bearings Incorporated RBC currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

RBC delivered a trailing four-quarter average earnings surprise of 4.9%. In the past 60 days, the Zacks Consensus Estimate for RBC’s fiscal 2025 earnings has increased 1.2%.

Enersys ENS presently sports a Zacks Rank of 1. The company delivered a trailing four-quarter average earnings surprise of 2.2%.

In the past 60 days, the consensus estimate for ENS’ fiscal 2025 earnings has increased 7.2%.

Applied Industrial Technologies AIT presently carries a Zacks Rank of 2. AIT delivered a trailing four-quarter average earnings surprise of 5.3%.

In the past 60 days, the consensus estimate for AIT’s fiscal 2025 earnings has inched up 1.4%.

Only $1 to See All Zacks' Buys and Sells

We're not kidding.

Several years ago, we shocked our members by offering them 30-day access to all our picks for the total sum of only $1. No obligation to spend another cent.

Thousands have taken advantage of this opportunity. Thousands did not - they thought there must be a catch. Yes, we do have a reason. We want you to get acquainted with our portfolio services like Surprise Trader, Stocks Under $10, Technology Innovators,and more, that closed 256 positions with double- and triple-digit gains in 2024 alone.

See Stocks Now >>Parker-Hannifin Corporation (PH) : Free Stock Analysis Report

RBC Bearings Incorporated (RBC) : Free Stock Analysis Report

Applied Industrial Technologies, Inc. (AIT) : Free Stock Analysis Report

Enersys (ENS) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.