When thinking of Consumer Staples titans, PepsiCo PEP undoubtedly jumps to the forefront of many minds. The company has established itself nicely over decades of successful operations, also rewarding shareholders nicely along the way.

These defensive-natured stocks are great for balancing a risk profile, as they possess the advantageous ability to generate consistent sales in the face of many economic situations. And they also carry a track record of increasing quarterly dividend payouts, another major perk.

Notably, PEP is on the reporting docket this week, with its results expected to come this Thursday before the market’s open. Let’s take a closer look at what to expect.

PepsiCo Earnings

PEP posted solid results concerning headline figures in its latest release, exceeding both of our consensus EPS and sales estimates. Sales grew by a modest 1% year-over-year, whereas adjusted EPS fell 7%. International momentum followed through nicely, with initiatives aimed at increasing growth and profitability also discussed in post-earnings commentary.

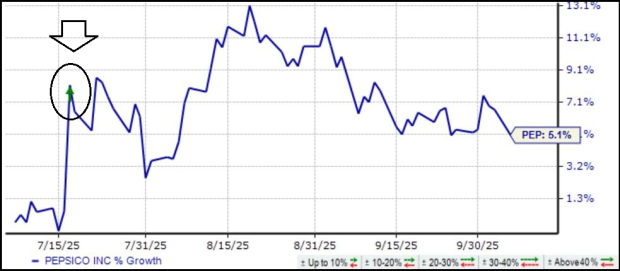

Notably, the company maintained its current year financial guidance, a key hurdle to clear amid the profitability-crunched environment PEP has seen within its North America results. Shares saw nice post-earnings strength following the release, reflective of a temporary turnaround in sentiment.

Image Source: Zacks Investment Research

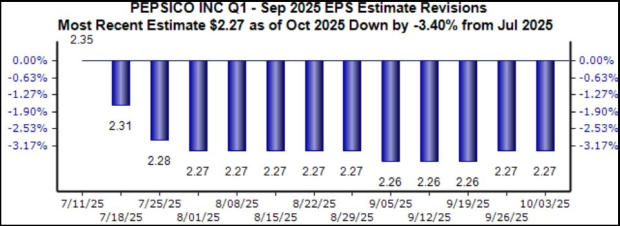

Analysts have shown some bearishness for the upcoming print, with the current $2.27 Zacks Consensus EPS estimate down roughly 3% over the last several months. But while the revisions have been negative, the recent stability and tick higher across August and September are a better takeaway to focus on.

Image Source: Zacks Investment Research

Revenue revisions have trickled higher over the same timeframe, with PEP forecasted to post 2.4% year-over-year sales growth on 1.7% lower earnings.

Notably, shares are currently trading at a historically low forward 12-month earnings multiple, with the current 17.0X value nearly reflecting a five-year low. Shares currently trade at a 28% discount relative to the S&P 500, again among the lowest we’ve seen over the last five years.

Image Source: Zacks Investment Research

Overall, commentary surrounding its North America results will again be key, with International momentum also likely to take the spotlight. Its reaffirmation of current year guidance in its latest release, stable EPS revisions over the past month, and positive sales revisions provide the company with a favorable backdrop heading into the print.

Keep in mind that the company recently strengthened its long-term strategic partnership with Celsius CELH near the beginning of September, which bolstered its energy drink portfolio nicely. The company has enjoyed favorable tailwinds from its partnership with Celsius, which are expected to continue as Celsius continues to gain momentum.

Putting Everything Together

Consumer staples titan PepsiCo PEP is on the reporting docket for this week, with results expected to come before the market’s open on Thursday. Analysts have largely kept their EPS revisions stable over the past month, whereas sales revisions have modestly moved higher.

Shares are also trading at historically cheap valuation levels, another key factor to keep in mind concerning the post-earnings move. Commentary and greater visibility about upcoming periods will dictate the post-earnings move, but it’s critical to note that the stock has been in a longer-term downtrend for some time now (down 7% over two years), with even a little bit of positivity likely to keep shares stable.

5 Stocks Set to Double

Each was handpicked by a Zacks expert as the #1 favorite stock to gain +100% or more in the coming year. While not all picks can be winners, previous recommendations have soared +112%, +171%, +209% and +232%.

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor.

Today, See These 5 Potential Home Runs >>PepsiCo, Inc. (PEP) : Free Stock Analysis Report

Celsius Holdings Inc. (CELH) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.