Peloton Interactive, Inc. PTON surprised investors in first-quarter fiscal 2026 with a sharp rebound in free cash flow, posting $67 million compared with expectations for a slight outflow. On the surface, this marks a meaningful improvement after years of balance-sheet stress. The key question, however, is whether this surge signals a sustainable turnaround or reflects temporary timing benefits.

Management was transparent in noting that roughly $30 million of first-quarter fiscal 2026 free cash flow stemmed from timing-related factors, including vendor payment shifts and favorable tariff dynamics. Lower-than-expected tariff rates and delayed implementation also provided a near-term lift. These elements suggest that not all of the cash flow upside is structural and that some reversal is likely to happen in the coming quarters.

That said, dismissing the improvement as purely a timing boost would be shortsighted. Peloton is showing tangible progress on cost discipline. Operating expenses declined by double digits year over year, and the company reiterated confidence in achieving at least $100 million in run-rate cost savings by fiscal 2026. Importantly, adjusted EBITDA exceeded guidance even after absorbing recall-related inventory charges, highlighting improved underlying profitability.

The balance sheet trajectory also strengthens the bullish case. Net debt has fallen nearly 50% year over year, leverage ratios have compressed sharply and liquidity remains ample. This deleveraging gives Peloton more flexibility as it approaches upcoming convertible note maturities and evaluates refinancing options.

Ultimately, Peloton’s free cash flow surge appears to be a mix of both timing and transformation. Near-term benefits may normalize, but the combination of tighter cost controls, improving margins and a healthier capital structure suggests the company is laying the groundwork for more durable cash generation. The next few quarters will be critical in proving that first-quarter fiscal 2026 was the start of a trend, not just a fortunate quarter.

PTON’s Price Performance, Valuation and Estimates

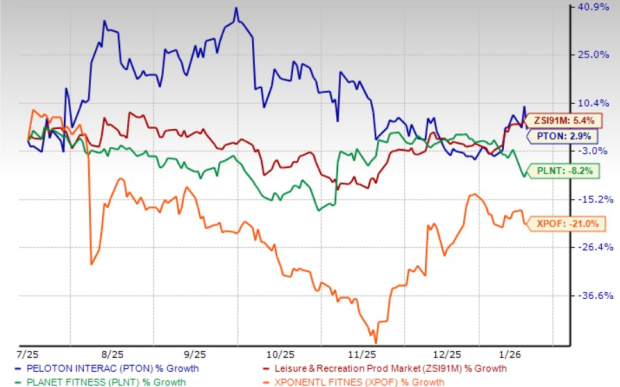

Peloton’s shares have risen 2.9% in the past six months compared with the industry’s growth of 5.4%. In the same time frame, stocks like Planet Fitness, Inc. PLNT and Xponential Fitness, Inc. XPOF have declined 8.2% and 21%, respectively.

Price Performance

Image Source: Zacks Investment Research

From a valuation standpoint, PTON trades at a forward price-to-sales ratio of 1.09X, down from the industry’s average. Planet Fitness and Xponential Fitness’ P/S stand at 5.73X and 1.32X, respectively.

P/S (F12M)

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for PTON’s 2025 and 2026 earnings implies a year-over-year uptick of 136.7% and 19.5%, respectively.

Image Source: Zacks Investment Research

PTON currently has a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks Names #1 Semiconductor Stock

This under-the-radar company specializes in semiconductor products that titans like NVIDIA don't build. It's uniquely positioned to take advantage of the next growth stage of this market. And it's just beginning to enter the spotlight, which is exactly where you want to be.

With strong earnings growth and an expanding customer base, it's positioned to feed the rampant demand for Artificial Intelligence, Machine Learning, and Internet of Things. Global semiconductor manufacturing is projected to explode from $452 billion in 2021 to $971 billion by 2028.

See This Stock Now for Free >>Planet Fitness, Inc. (PLNT) : Free Stock Analysis Report

Peloton Interactive, Inc. (PTON) : Free Stock Analysis Report

Xponential Fitness, Inc. (XPOF) : Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.