Key Points

PayPal continues to struggle to keep up with competition from Apple, Google, and Buy Now, Pay Later companies.

Growth has stalled again, costing the CEO his job.

PayPal is cheap, but it's also risky. Investors may be wise to wait things out at this point.

- 10 stocks we like better than PayPal ›

Alex Chriss began his tenure as CEO of PayPal Holdings (NASDAQ: PYPL) in the fall of 2023. Chriss came over from Intuit, and investors hoped that he would breathe new life into one of the oldest fintech companies.

Despite unveiling some fresh ideas and pushing PayPal to rethink its user experience, PayPal apparently didn't see results quickly enough. In February, PayPal announced it had replaced Chriss with Enrique Lores, stating the company had been dissatisfied with progress over the past two years.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

Investors have endured years of miserable performance from PayPal stock, and shares have dropped to less than 10 times earnings today. Is it finally time to look for a turnaround, or is PayPal's low valuation a trap waiting to ensnare your capital?

Image source: The Motley Fool.

Failure to build around a strong, but stagnant, legacy business

PayPal is still one of the most prominent fintech brands, with approximately 439 million active users as of the fourth quarter of 2025. This is measured as anyone with at least one transaction over the past 12 months. The company offers various payment products and services, including branded and white-labeled payment processing (Braintree), and it owns Venmo, the popular peer-to-peer payment app.

But PayPal has arguably become a stale brand. Apple and Alphabet have become major competitors in the mobile payments space with Apple Pay and Google Pay. Buy Now, Pay Later companies, such as Affirm and Klarna, have become increasingly popular with young consumers. This has shown up in the numbers. Sure, 439 million active users is a lot, but PayPal had 435 million at the end of 2022, so there isn't much user growth happening.

PayPal leaned into advertising and a brand refresh under Alex Chriss, but PayPal's branded checkout growth slowed drastically in the fourth quarter of 2025. Branded online checkout growth slowed to 1% in the quarter, down from 6% in the fourth quarter of 2024. Branded experiences as a whole slowed to 4% growth from 8% in the same quarter of the prior year.

The momentum loss likely factored into PayPal's decision to move on from Alex Chriss.

Why investors may want to show restraint here

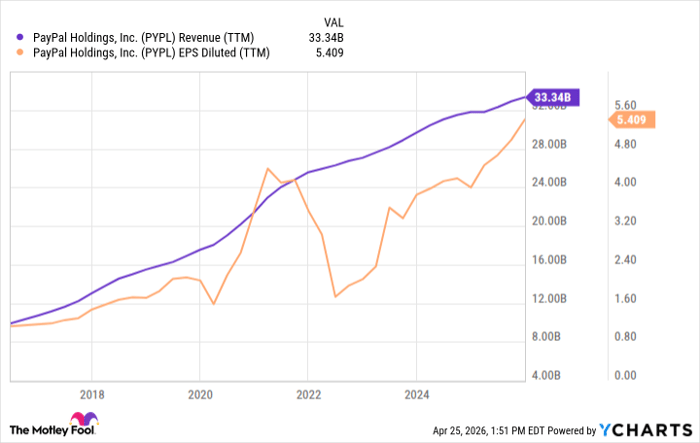

PayPal stock is a bit of a conundrum for investors. If you look backward, PayPal has continued to grow its top and bottom lines despite all the worries over competition.

Data by YCharts.

I'll admit that shares appear very cheap at under 10 times earnings. However, PayPal could face rougher waters ahead. The company guided its non-GAAP earnings to range between a low-single-digit decline and flat in 2026. Beyond that, PayPal has had three CEOs in roughly as many years. Different leaders have different opinions and ideas, and new CEO Enrique Lores is likely to push for more change, given that his predecessor lost his job because the current strategy isn't working well enough.

Potential investors may want to consider staying on the sidelines for now. PayPal now needs more time to implement new ideas and show in the numbers that they are working. There's investment upside if the new CEO finally rights this ship. That said, PayPal risks becoming a value trap, especially if its stagnant brand begins to weigh more on the company's financials than it has to this point.

Should you buy stock in PayPal right now?

Before you buy stock in PayPal, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and PayPal wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $492,752!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,327,935!*

Now, it’s worth noting Stock Advisor’s total average return is 991% — a market-crushing outperformance compared to 201% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of April 28, 2026.

Justin Pope has positions in Alphabet. The Motley Fool has positions in and recommends Alphabet, Apple, Intuit, Klarna Group, and PayPal. The Motley Fool recommends the following options: short June 2026 $50 calls on PayPal. The Motley Fool has a disclosure policy.

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.